- A recorded statement is a routine system requirement for the adjuster, but it creates a permanent record of your claim details that you cannot easily change later.

- You do not have to give the statement the exact second the adjuster calls; you have the right to schedule it for a time when you have your notes in front of you.

- Stick exclusively to observable facts, never guess about timelines or causes of damage, and always request a copy of the transcript for your intake file.

The Reality of the “Quick Chat”

Usually, within a day or two of filing a property claim, your phone will ring. It is the adjuster assigned to your file. They will introduce themselves, confirm a few basic details, and then casually drop a phrase that immediately makes most homeowners freeze: “I just need to take a quick recorded statement to get the facts down.”

In my years working in claims operations, I have seen this exact moment trigger incredible anxiety. People worry they are going to say the wrong thing, accidentally trap themselves, or give the insurance company an excuse to complicate the file. The pressure of being recorded makes people nervous, and nervous people tend to over-explain, guess, or ramble.

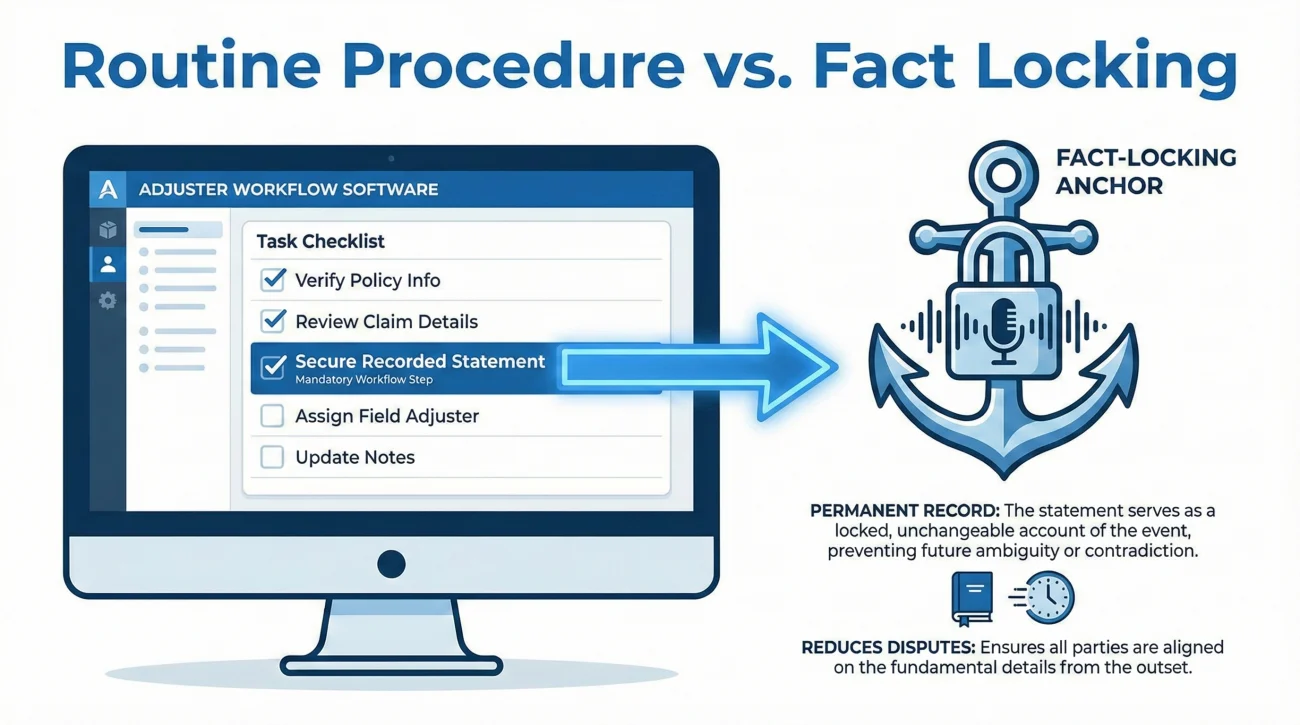

I want to bring some operational calm to this situation. A recorded statement is a standard part of the intake process. When a new claim hits an adjuster’s desk, their software system generates a checklist of tasks they must complete before moving the file forward. Securing a recorded statement is typically one of those mandatory checkboxes.

However, understanding that it is a routine process for them does not mean you should treat it casually. What you say on that recording becomes the foundational narrative of your file. If your recorded timeline contradicts the date you gave during your initial notice of loss, or if you guess about how a pipe broke instead of just stating that you found water, you create a discrepancy. In the claims world, discrepancies equal delays.

Is It a Trap or Just a Routine Procedure?

I am frequently asked if the recorded statement is a deliberate trap designed to trick policyholders. The operational truth is less dramatic, but just as important to understand. It is not a trap in the malicious sense, but it functions as a permanent anchor for your facts.

The goal of the recorded statement is fact-locking. The adjuster needs to clearly establish the timeline of events, the scope of the immediate damage, and what actions you took to secure the property. They record it so there is no ambiguity later about what was reported on day one.

Key Point: The danger is not that the adjuster is trying to trick you. The danger is that human memory is flawed, especially during a crisis. If you rely solely on your memory while a recorder is running, you risk introducing errors into your own file.

Let me share a very common field note from the operations side. A homeowner suffers a roof leak during a storm. The adjuster calls for a recorded statement while the homeowner is at work, distracted, and stressed. The adjuster asks, “When did you first notice the water on the ceiling?” The homeowner, trying to be helpful, guesses: “Uh, I think it was Tuesday night around 8 PM.”

Later, the homeowner checks their phone records and realizes they actually texted their spouse about the leak on Monday afternoon. But the recorded statement now says Tuesday. When the adjuster pulls the weather reports to verify the storm data, Monday shows high winds, but Tuesday shows clear skies. Because the homeowner guessed under pressure, the file is now flagged for an inconsistency regarding the date of loss. This preventable error can stall a claim for weeks while the timeline is investigated and corrected.

The Clarification Checklist: Before You Hit Record

The single biggest mistake you can make is agreeing to give a recorded statement the exact moment the adjuster calls, especially if you are driving, at work, or standing in the middle of a damaged room. You have the right to be prepared.

When the adjuster asks to take your statement, your first practical step is to pause the momentum. You need to clarify the parameters of the call and schedule it for a time when you are sitting down in a quiet space with your initial claim notes in front of you.

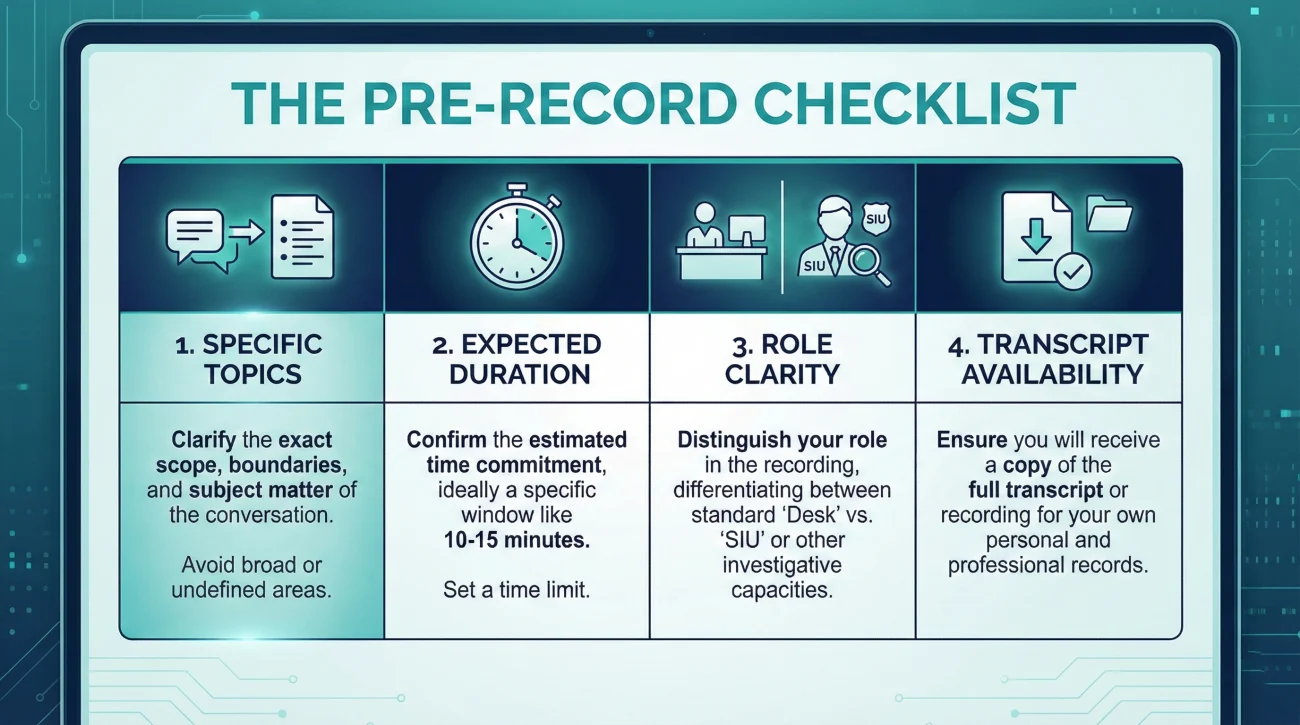

Here is a checklist of what you should clarify before agreeing to proceed with the recording.

| What to Clarify | Why It Matters |

|---|---|

| The Specific Topics | Are we only discussing the initial cause of loss, or do you expect a full inventory of damaged items today? Confirm whether this is initial intake only, so you know exactly what files to have ready. |

| The Expected Duration | A standard intake statement takes 10 to 15 minutes. If they block out an hour, you are facing a much more complex interview and need to prepare accordingly. |

| Role Clarity | Confirm if this is just for the desk adjuster’s file, or if it is being routed to a specialized department (like liability or SIU). If routed, ask what department and why. |

| Transcript Availability | Always ask upfront if they will provide you with a written transcript or an audio copy of the recording for your own records. |

Boundary Rules: How to Stick to the Facts

Once you are set up with your log and ready, the recording will begin. The adjuster will state the date, time, and your name, and ask for your permission to record. Before answering the first substantive question, you can use this 60-second opener script to set clear boundaries:

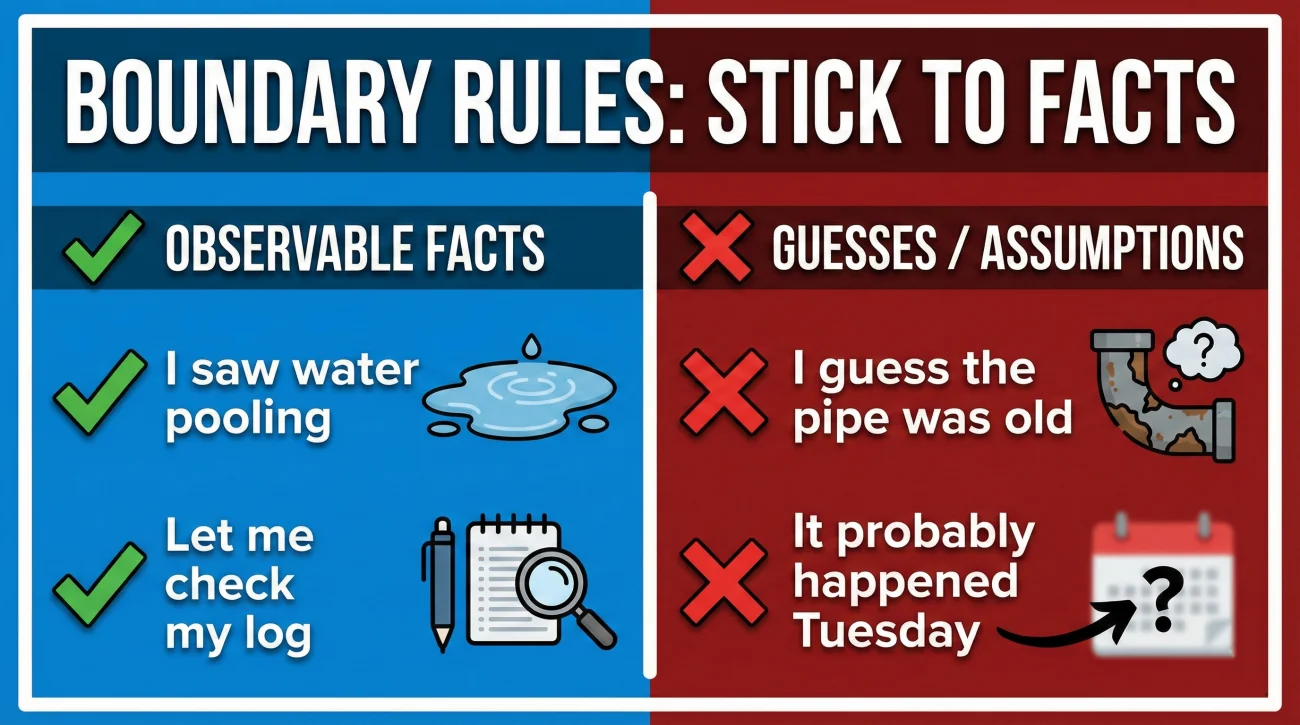

From that moment on, your safest lane is to operate within the boundaries of observable facts. I always advise people to visualize a strict line between what they actually saw with their own eyes and what they assume happened. You are there to report the former, never the latter.

- ✅ Do state exactly what you observed. “I walked into the kitchen at 7:15 AM and saw water pooling near the refrigerator.”

- ✅ Do reference your notes. It is perfectly acceptable to say, “Let me check my log. Yes, the plumber arrived at 10:30 AM.”

- ✅ Do keep answers short. Answer the specific question asked and then stop talking. Silence on the line is fine; wait for their next question.

- ❌ Do not guess about the technical cause. You are not a forensic engineer. Do not say, “The water pressure must have built up and blown the valve.” Say, “I saw water coming from behind the wall.”

- ❌ Do not estimate ages or conditions. If asked how old the roof is, and you do not have the paperwork in front of you, do not guess “maybe ten years.” Say, “I will need to check my closing documents and get back to you with the exact year.”

⚠️ Warning: Beware of conversational fillers. Words like “probably,” “maybe,” “I think,” and “I guess” are dangerous in a recorded file. If an adjuster hears “I think the leak started yesterday,” their notes will reflect uncertainty. If you do not know an answer with 100 percent certainty, the only correct answer is, “I do not know, I will need to check my records.”

The “Notes First” Principle

You should never go into a recorded statement relying on your memory. In my daily claim reviews, the cleanest, fastest-moving files are always the ones where the policyholder operates from a written baseline. This is why having your intake folder set up is so critical.

Before the call, you should have a single sheet of paper in front of you containing the absolute foundational facts of your claim. This includes the date of the loss, the time you discovered it, the immediate steps you took to stop further damage (like shutting off the water or calling a mitigation crew), and the names of anyone who has already inspected the property.

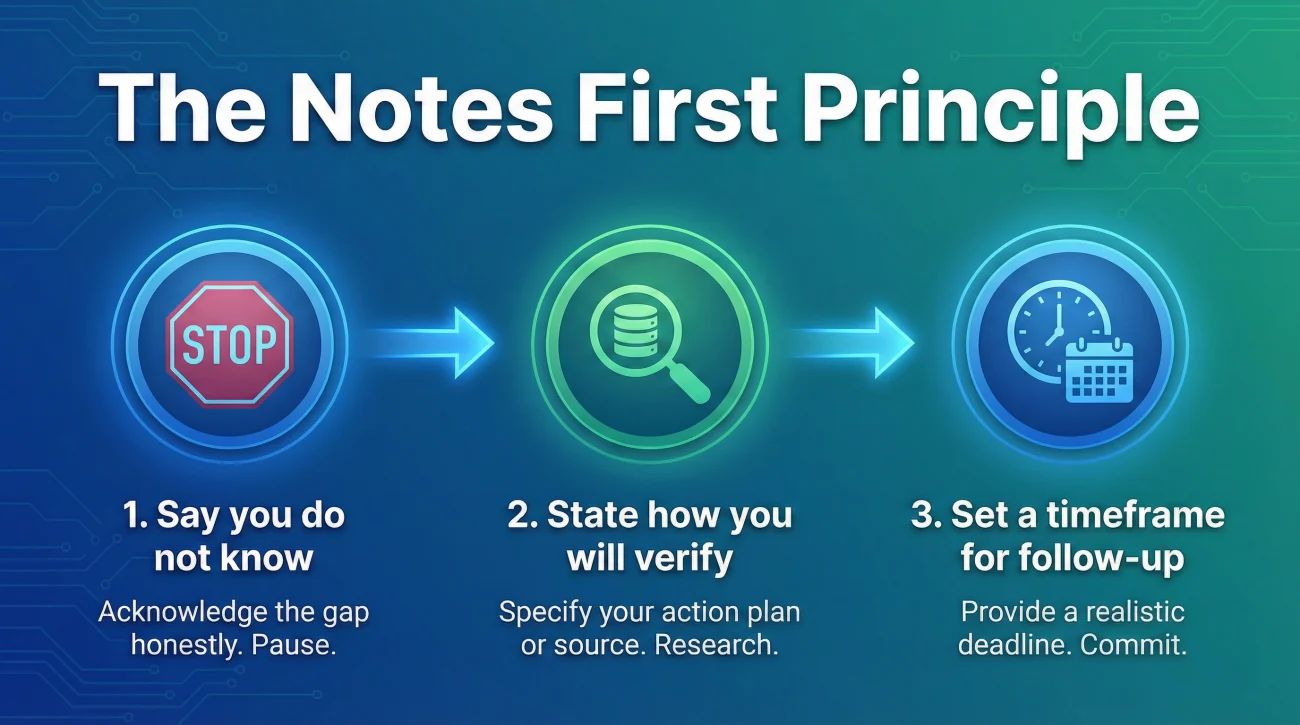

If the adjuster asks a question and the answer is not on your paper, follow this simple three-step playbook:

- 1️⃣ Say you do not know: Refuse the urge to guess.

- 2️⃣ State how you will verify: “I will need to check the plumber’s invoice.”

- 3️⃣ Set a timeframe: “I will follow up in writing by tomorrow morning.”

If you have not yet established a system for organizing these facts, you need to build that foundation immediately. I highly recommend reviewing our complete proof of loss playbook, which walks through exactly how to structure your documentation so you never have to guess when an adjuster asks for proof.

Navigating Questions and Summaries

Adjusters are trained to ask questions in specific ways to categorize the damage accurately. Sometimes, these questions can feel leading or confusing. Let us look at how applying the boundary rules changes the dynamic of the conversation.

A very common scenario involves questions about how long a problem has existed. Insurance covers sudden and accidental damage, not long-term maintenance issues. Therefore, the adjuster must ask questions to establish the timeline of the damage.

Adjuster: “Did you notice any soft spots on that ceiling last week?”

Homeowner: “I don’t think so, I mean, maybe? We don’t really look up there much, so it could have been there a while.”

Adjuster: “Did you notice any soft spots on that ceiling last week?”

Homeowner: “The first time I observed any damage to the ceiling was yesterday evening at 6:00 PM.”

Notice the difference? The “Before” response introduces massive ambiguity into the file. The homeowner was just trying to be honest about their habits, but they inadvertently gave the adjuster a reason to investigate if this was a long-term, uncovered leak. The “After” response is purely factual, precise, and removes most ambiguity.

You may also face questions where the adjuster attempts to summarize your words. They might say, “So, what you are saying is the wind blew the shingles off, which caused the leak?” If you did not actually see the wind blow the shingles off, do not agree to that summary.

A calm, factual correction sounds like this: “To be accurate, I did not see the roof during the storm. I can only confirm that after the storm passed, I found water in the living room and shingles in the yard.” You are maintaining control of your narrative by refusing to adopt assumptions.

Here are two more examples of how to deflect a leading summary:

“So you’re saying the pipe is old and finally gave out?”

“I cannot confirm the age or condition of the pipe. I can only confirm I found water pooling under the sink at 8:00 AM.”

“It sounds like the contractor thinks the roof was installed poorly.”

“I cannot confirm the installation quality. I can only confirm what the contractor wrote in their initial damage report.”

What to Do After the Call Concludes

The work does not stop when the adjuster turns off the recording. In claims operations, a conversation only matters if it is documented and accessible later.

Immediately after hanging up, open your intake file and create a new entry in your timeline log. Note the date, the time the statement started and ended, the name of the adjuster who took the statement, and a brief bulleted list of the main topics covered.

💡 Pro Tip: Within 24 hours of the call, it is a very smart process-friendly habit to send a brief, polite email to the adjuster confirming the statement took place. You can simply state, “Thank you for taking my recorded statement today regarding the date of loss and initial damage. As discussed, please provide a copy of the audio file or the written transcript for my records.”

Do not be surprised if getting the transcript takes time, or if they require a formal written request to release it. The point is not necessarily to get it the next day; the point is to establish a clear paper trail showing that you actively manage your file and expect transparency in return.

If you realize later that evening that you misspoke during the recording (for example, you gave the wrong date for when the mitigation company arrived), do not panic. Do not wait for them to figure it out. Send a written message immediately stating, “During our recorded statement today, I stated the crew arrived on Tuesday. Upon checking my invoices, I need to correct the record: they arrived on Wednesday morning.” Correcting the record proactively shows you are organized and focused on accuracy.

Final Thoughts: Controlling the Pace

Handling a recorded statement successfully comes down to controlling the pace of the interaction. The insurance company operates at their speed; you must operate at yours. They want to check their intake box quickly, but you have to live with the words you put on that recording for the entire lifespan of the claim.

By refusing to do the interview on the fly, by preparing your notes in advance, and by strictly limiting your answers to observable facts rather than guesses, you remove the biggest risks associated with this process. You provide the adjuster exactly what they need—a clear, factual baseline—without accidentally creating the kind of contradictions that lead to endless delays.

Stay calm, stay organized, and remember that “I need to check my records” is often the most powerful and protective sentence you can use during the early days of a claim.

❓ FAQ

🛑 Do I legally have to give a recorded statement to my insurance company?

Policy language varies, but in most cases, yes. Standard property policies include a “duties after loss” section that usually requires your cooperation, which often includes providing a recorded statement. However, you do not have to do it without preparation.

⏳ When is the best time to give a recorded statement?

The best time is only after you have stabilized your property, gathered your basic timeline facts, and are sitting in a prepared environment with your timeline log. Never do it while driving or distracted.

🗣️ What should I absolutely not say in an insurance recorded statement?

Do not use phrases like “I guess,” “I assume,” or “It probably happened when…” Never guess about the technical cause of the damage or estimate the age of items if you do not know the exact facts.

📝 Can I use my notes during a recorded insurance call?

Absolutely. It is highly encouraged. Relying on written notes ensures your timeline is accurate and prevents you from making nervous mistakes or contradicting your initial claim report.

🔄 What if I realize I made a mistake during the recorded statement?

If you realize it during the call, correct it immediately on the recording. If you realize it after the call ends, send a written message to the adjuster immediately to formally correct the record in your file.

📱 Can I record the insurance adjuster back during the statement?

This depends entirely on the recording laws in your specific jurisdiction (one-party vs. two-party consent). Operationally, the simpler path is to request a copy of their audio file or transcript.

🤷♂️ What if I just don’t know the answer to a question they ask?

The safest and most accurate answer is simply, “I do not know.” If it is something you can find out later, say, “I do not have that information right now, I will check my records and get back to you.”

📄 Will the insurance company automatically give me a copy of the recording?

Usually, no. They will keep it in their internal file. You must proactively ask for a copy of the audio file or the written transcript for your own records.

⏱️ How long does a recorded statement for a property claim typically take?

A standard initial intake statement usually takes between 10 to 20 minutes. If the claim is highly complex, or if it is a liability issue, it may take longer, which is why you should ask about duration beforehand.

🕵️♂️ Can they use my recorded statement to deny my claim entirely?

Inconsistencies or admitting to things that fall outside your coverage (like stating a leak has been happening for months) can certainly be used to justify a denial or cause massive delays in the investigation process.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.