- Your date of loss documentation is the chronological anchor for your entire claim file. Inconsistent dates across different documents are a primary cause of process delays.

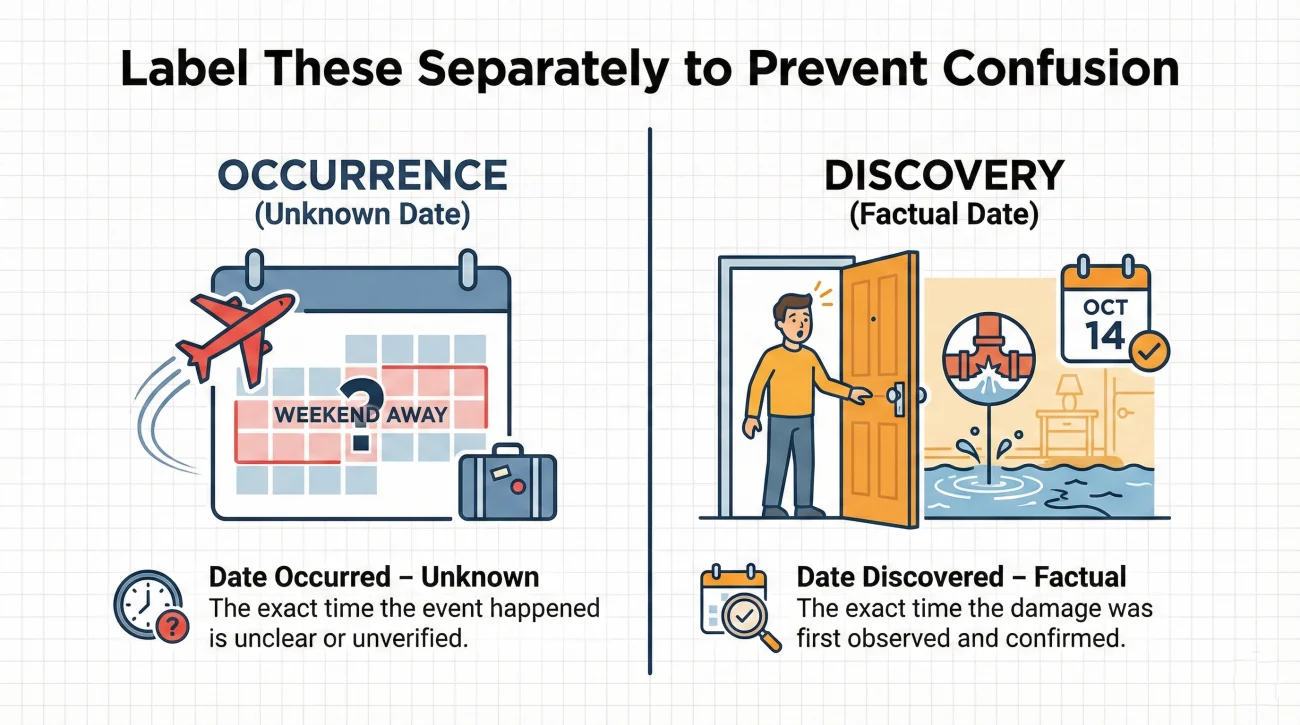

- Always distinguish between the date the damage “occurred” and the date it was “discovered.” Documenting this difference clearly prevents confusion.

- Review every third-party document (contractor estimates, mitigation invoices) to ensure their listed dates match your initial report exactly before submitting them.

- If a date error happens, use a clean correction protocol. Submit a written clarification rather than just quietly changing the date on your next form.

The Ripple Effect of a Single Mismatched Date

When you are dealing with property damage, your first instinct is simply to stop the leak, secure the roof, or clean up the mess. The exact time and date you found the problem usually feel like minor details compared to the stress of the actual damage. But in my experience reviewing claim files and operations, the timeline drives the entire routing and verification process. Establishing clear date of loss documentation is one of the most critical steps you can take to keep your file moving forward smoothly.

I often see otherwise straightforward claims hit a brick wall simply because the dates on the paperwork do not align. For example, a homeowner might report that a pipe burst on a Tuesday. A week later, they submit an invoice from their emergency plumber, but the plumber’s front office accidentally dated the invoice for the previous Sunday. To a desk adjuster reviewing hundreds of files, that discrepancy is an immediate red flag. The process stops, an email is sent out for “clarification,” and days or even weeks are lost while the confusion is untangled.

My goal here is to help you build a consistent, reliable timeline from day one. I want to walk you through the core elements of what you need to track, how to organize your timeline, and how to fix the inevitable minor mistakes without derailing your entire process. By treating your dates as a core part of your evidence, you eliminate the guesswork for the person processing your file.

Building Your Incident Timeline Record

When we talk about documenting the date of loss, we are not just talking about circling a day on the calendar. We are talking about building a timeline that makes logical sense and is backed up by your files. A good timeline leaves no room for questions.

Key Point: Your timeline needs to explain not just when the event happened, but when you found it, what you did immediately after, and who was involved in those first few critical hours.

Basic Date Vocabulary

Before building your log, it helps to understand the terminology your adjuster is looking for. People often confuse the day they paid a plumber with the day the damage actually happened.

- 📄 Loss Date: When the damage actually occurred.

- 📄 Discovery Date: When you first noticed the damage.

- 📄 Service Date: When a contractor or mitigation crew started work.

- 📄 Invoice Date: When the bill was generated (this is rarely the loss date).

I recommend keeping a simple, running log. You do not need complex software. A standard notebook or a digital document works perfectly. The objective is to have a single source of truth that you reference every time you fill out a form or speak to an adjuster. Here are the minimum fields you should be tracking in your timeline record.

| Timeline Field | What to Record | Why It Matters for Your File |

|---|---|---|

| Date and Time Discovered | Exact day, date, and approximate time you noticed the damage. | Sets the baseline for your initial report. This is the most critical data point. |

| Date and Time Occurred (If Known) | When the actual event happened (e.g., time of the severe storm). | Helps correlate the damage to known weather events or specific incidents. |

| First Action Taken | Turning off the water main, putting a tarp on the roof. | Shows you took immediate steps to prevent further damage. |

| First Vendor Contacted | Name of the emergency plumber or water mitigation crew, plus time called. | Provides a trail for the earliest third-party invoices you will receive. |

Before you send any of this information in your initial claim package, I always suggest reviewing your master property insurance claim documents checklist. You want to make sure that the timeline you have drafted matches the supporting files you are about to attach.

The “Discovered vs. Occurred” Trap

One of the most common mistakes I see happens when someone is not home when the damage actually takes place. This creates confusion between when the damage “occurred” and when it was “discovered.” If you are not careful with how you communicate this, it can look like you are changing your story.

💡 Two Dates You Must Label:

- ✅ Date Discovered: The factual day and time you found the damage.

- ✅ Date Occurred: The day the event happened (only if known, otherwise state “unknown”).

Let’s look at a realistic operational scenario. You leave for a weekend trip on Friday morning. On Saturday night, a pipe fails under your kitchen sink. You come home on Sunday afternoon and find standing water in the kitchen. When you call to report the claim, the representative asks, “When did this happen?”

If you say “Sunday,” but the mitigation crew later writes “estimated 48 hours of standing water” on their report, you suddenly have a conflict in your file. The adjuster sees your “Sunday” date and the crew’s “Friday/Saturday” estimate, and the file gets flagged for review.

⚠️ Warning: Avoid guessing the exact moment of failure if you were not there to witness it. Stick to the facts you can prove.

Here is how you handle this smoothly to keep your documentation clean:

“The pipe broke on Sunday afternoon. That is the date of loss.”

“I discovered the damage on Sunday at 4:00 PM when I returned from a trip. The exact time the pipe failed over the weekend is unknown, but I immediately shut off the water upon discovery.”

By splitting the difference between discovery and occurrence, you protect the integrity of your timeline. You are giving the adjuster the exact, factual truth, which matches what the water mitigation crew will likely put in their report.

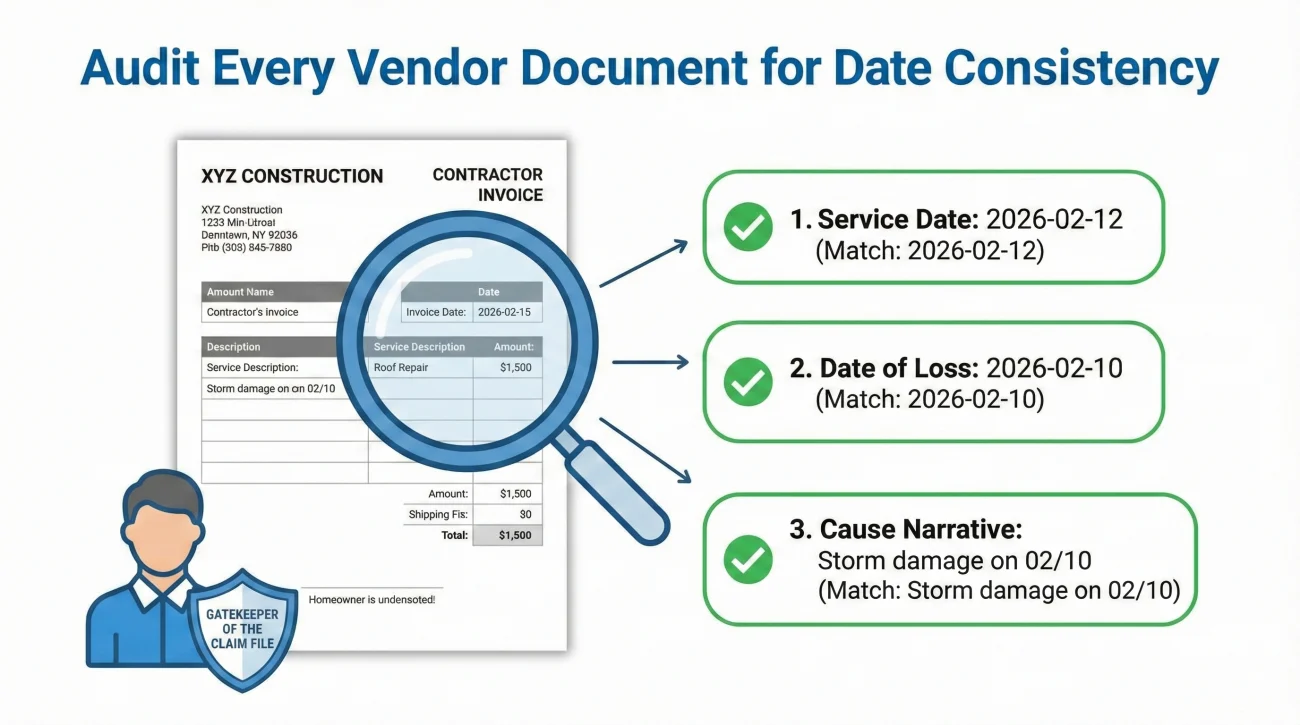

Policing Your Vendor Documents

This is a field note from the operations side that you absolutely must adopt: you cannot blindly trust the paperwork handed to you by contractors or emergency service vendors. These companies are moving fast, going from house to house, and administrative errors happen constantly.

I have seen countless files delayed because a homeowner forwarded a roofer’s estimate without reading it first. The homeowner reported the storm damage correctly for the 15th of the month. The roofer, filling out the form a week later, accidentally typed the 16th as the date of loss on their estimate cover sheet. When the insurer receives that document, their system notes a date discrepancy. They cannot process the roofer’s estimate because technically, it is referencing a different date than the claim on file.

You must become the gatekeeper of your claim file. Every single document that a third party hands you must be audited for date consistency before you pass it along to the adjuster.

- 📄 Check the Service Date: Does the date they claim they arrived match your log?

- ✅ Check the Date of Loss: If their form has a specific field for “Date of Loss,” does it perfectly match the date you gave the insurer?

- 📄 Check the Cause Narrative: Does their brief description of the event match your timeline (e.g., “wind damage” vs “tree impact”)?

When Vendors Use Their Own Terminology

Be aware that some contractors use their own form templates. A vendor might write “Incident Date” on their paperwork, but they actually mean the “Service Date” when their crew arrived at your house. If you see vague terminology on a vendor form, ask them to clarify or update it to match the standard terms above so the desk adjuster does not get confused.

How to Ask for a Vendor Correction

If you catch an error on a vendor’s document, do not cross it out with a pen and write the correct date. Altered documents are heavily scrutinized. Instead, you need to ask the vendor to issue a clean, revised copy. Keep your request polite but firm.

Subject: Request for invoice revision – Date correction needed

Hello [Vendor Name],

Thank you for sending over the invoice and estimate for the work completed at my home. Before I forward this to my adjuster, I noticed a small clerical error regarding the dates.

The invoice lists the date of loss as [Incorrect Date]. The correct date of loss on file for this claim is [Correct Date].

Could you please update the date of loss on your document to [Correct Date] and send me a revised PDF? I want to ensure the dates match my file exactly so there are no delays in processing.

Thank you for your help with this.

Correcting Your Own Date Mistakes

We are all human. Sometimes, in the panic of a flooded basement or a damaged roof, you might call the claims hotline and say the wrong day. Or perhaps you fill out an online form quickly and click the 12th on the calendar dropdown instead of the 11th. You realize the mistake a few days later when you are organizing your paperwork.

The worst thing you can do is just quietly start using the correct date on future forms without explaining the change. To the person reviewing your file, it looks like you cannot keep your story straight. The best approach is a transparent, written correction.

When I see a file where a homeowner proactively sends a short note correcting an administrative error, it actually builds credibility. It shows they are organized and paying attention to detail.

“A clean file isn’t one that never had a mistake; it is one where every mistake is clearly documented and corrected in writing.”

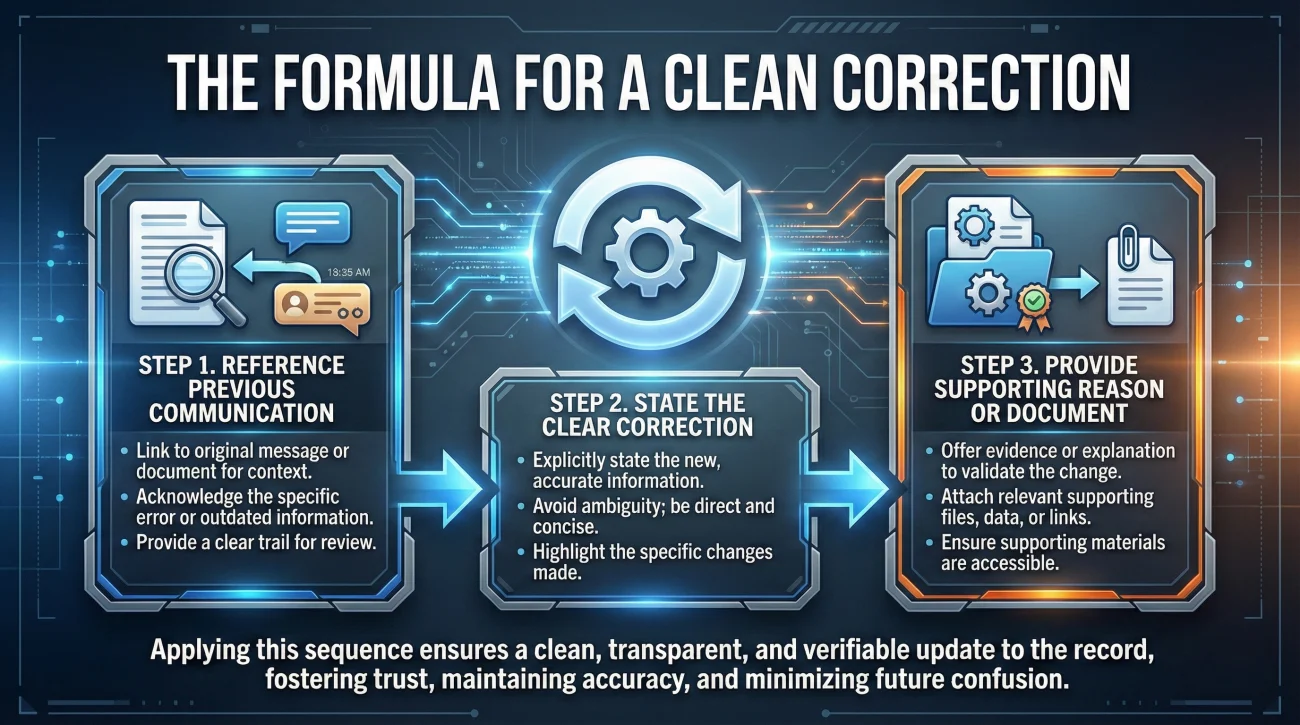

If you need to correct a date you previously provided, use this simple formula to update the record:

[Reference the previous communication] + [State the clear correction] + [Provide the supporting reason or document]

Here is an example of how that looks in practice:

Dear Adjuster,

I am writing to formally correct a date provided in my initial claim report. During my initial phone call on Tuesday, I accidentally stated that the leak was discovered on Sunday the 14th.

After reviewing my records and the initial emergency plumber’s dispatch log, the correct date of discovery was actually Saturday the 13th at approximately 8:00 PM. Please update my file to reflect Saturday the 13th as the correct timeline baseline moving forward.

I have attached the plumber’s dispatch receipt for your reference. Please confirm you have received this update.

💡 Pro Tip: Always ask for confirmation when you submit a correction. You want a written reply stating “Received and file updated” so you know the old, incorrect date is no longer being used against you.

Final Thoughts on Timeline Hygiene

Managing the date of loss documentation is ultimately about reducing friction. In the operational world of claims, speed comes from clarity. Every time someone has to stop and figure out why a receipt says Thursday but a form says Friday, your file moves to the bottom of the stack.

Take the extra ten minutes to build your incident timeline. Write down the facts, check every incoming document against your master log, and address any discrepancies head-on. By taking control of your timeline early, you project organization and competence, which goes a long way in keeping the entire process moving at a steady pace.

❓ FAQ

📅 What happens if I put the wrong date of loss on my claim?

A wrong date usually triggers a review process, causing delays. The adjuster may flag the file because the reported date does not align with weather reports or vendor invoices. It is best to correct the mistake in writing as soon as you notice it.

🕰️ Do I use the date the damage happened or the date I found it?

If you know exactly when it happened (like a specific storm), use that date. If the damage happened while you were away, clearly state the exact date and time you discovered it, and note that the time of occurrence is unknown.

🌧️ How do I prove the date of loss for storm damage?

Storm dates are usually verified using public weather reports. You can document it by retaining any contemporaneous weather alerts, local news reports, or photos of the immediate aftermath.

🔧 What if my plumber’s invoice has the wrong date?

Do not alter the document yourself. Contact the plumber’s office immediately, point out the discrepancy compared to your records, and ask them to issue a clean, revised invoice with the correct date before you send it to the insurer.

📝 Can I change the date of loss after I file the claim?

Yes, you can issue a correction, but it must be done carefully. Send a written message to your adjuster explaining the administrative error, stating the correct date clearly, and providing any proof (like a photo timestamp) that supports the change.

📸 Do photos count as date of loss documentation?

Yes. Digital photos often contain metadata (timestamp data) showing when they were taken. Taking photos immediately upon discovering damage is a strong way to establish a timeline, even if metadata is sometimes stripped when forwarding files.

🤷♂️ What if I was on vacation and don’t know the exact date?

Be honest and state that you were out of town. Provide the date you left and the exact date and time you returned to find the damage. Providing a date range is better than guessing a specific day that cannot be proven.

📂 Why does the adjuster keep asking about when the leak started?

They are trying to establish the timeline to understand how long water was sitting. Inconsistent answers can cause confusion, which is why having a written timeline log to reference during every call is so important.

✍️ How do I write an incident timeline for my insurance claim?

Keep a simple list noting the date and time discovered, the first actions you took to mitigate the damage, and a log of the first vendors you called. Keep this document updated and use it to double-check all other forms.

🛑 Will my claim be delayed if my dates don’t match exactly?

In many cases, yes. Discrepancies between your report, contractor invoices, and mitigation reports create confusion. The file usually pauses until the adjuster can get written clarification on which date is correct.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.