- Calling your agent to ask questions is often smart, but you must control the phrasing to avoid accidentally opening a formal claim before you are ready.

- Insurance systems track “inquiries” and “claims” differently. Once you state a specific date of loss and cause of damage, a claim record is usually triggered automatically.

- Always prepare a written list of hypothetical questions to confirm your deductible and coverage buckets before describing the actual damage to your property.

- Take detailed notes logging exactly what the agent says, but remember that the agent does not make the final coverage decision.

The Hesitation Before You Dial

You have damage to your property, and your first instinct is likely to pick up the phone and ask your agent for advice. It makes sense. You want to know if the damage is covered, how much your deductible is, and whether the repair costs will even exceed that deductible. But then the hesitation sets in: “If I call my agent, does that automatically start a claim?”

In my years working in claims operations, I have seen this exact scenario play out thousands of times. The reality is that the line between a policy-only discussion and an official First Notice of Loss (FNOL) is incredibly thin. A homeowner calls their agent just to explore options, uses a few specific phrases, and the next day, an adjuster is calling to schedule an inspection for a claim they never explicitly asked to file.

The goal of this guide is to help you navigate that very first conversation. I want to show you how to gather the facts you need to make an informed decision without losing control of the process. If you decide to call your agent before filing claim paperwork, you need a strategy.

Key Point: Your agent is there to service your policy, but they are also bound by the software systems they use. If you give them enough specific facts about a loss, their system may require them to generate a formal claim number, regardless of your intentions.

The Reality of the Information Gathering Chat

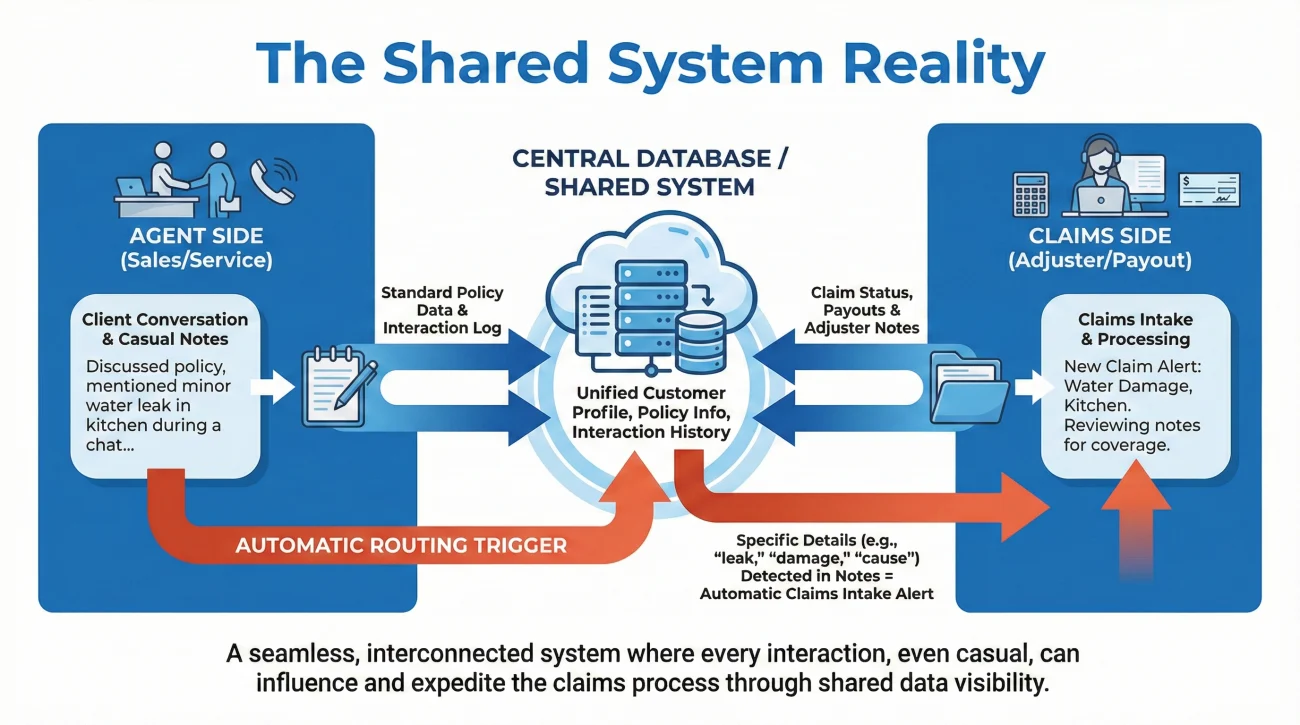

To communicate effectively, you first need to understand the structural difference between an agent and a claims adjuster. Many people assume the agent is the one who approves or denies the claim. In reality, the agent’s primary role is to sell policies, manage your account, and act as a bridge to the corporate carrier.

When you call the agency, you are speaking to the sales and service side of the business. The claims department is an entirely separate entity. However, these two sides share a computer system. This is where the danger of casual conversation lives.

I frequently review intake logs where the timeline of events clearly shows a breakdown in communication. A homeowner will call their agent on a Tuesday to ask if a sudden pipe burst is covered. The agent says, “Let me check your policy,” and enters notes into the system detailing the pipe burst and the date it happened. Because the facts of a loss were established, the system automatically routes those notes to the claims intake department. The homeowner thought they were just chatting; the system recorded it as a formal report.

Calling your agent in a panic, describing the exact damage, the date it happened, and asking, “Is this covered?”

Calling your agent calmly, asking hypothetical questions about your deductibles and limits, without establishing a formal date of loss.

Give yourself a 5-minute policy-only window before making any permanent decisions. You must keep the conversation strictly theoretical until you have made the firm decision to move forward.

The “Inquiry” vs. “Claim” Trap

In the insurance industry, there is a distinct difference between an “inquiry” and a “claim.” However, carriers define and track these differently, which is why you must tread carefully.

An inquiry is generally a question about policy terms, coverages, or deductibles. A claim is a formal request for compensation based on a specific event. The problem arises when an inquiry gets logged as a zero-dollar claim or an incident report.

To be clear, a simple policy question rarely impacts your rates. However, if your questions are specific enough that the agent logs an “incident” or a zero-dollar claim, that record could potentially be factored into future underwriting decisions depending on your carrier.

⚠️ Warning: Never assume that a conversation is completely off the record. Most modern agency phone systems log calls, and agents are trained to take notes on every interaction to protect themselves from liability.

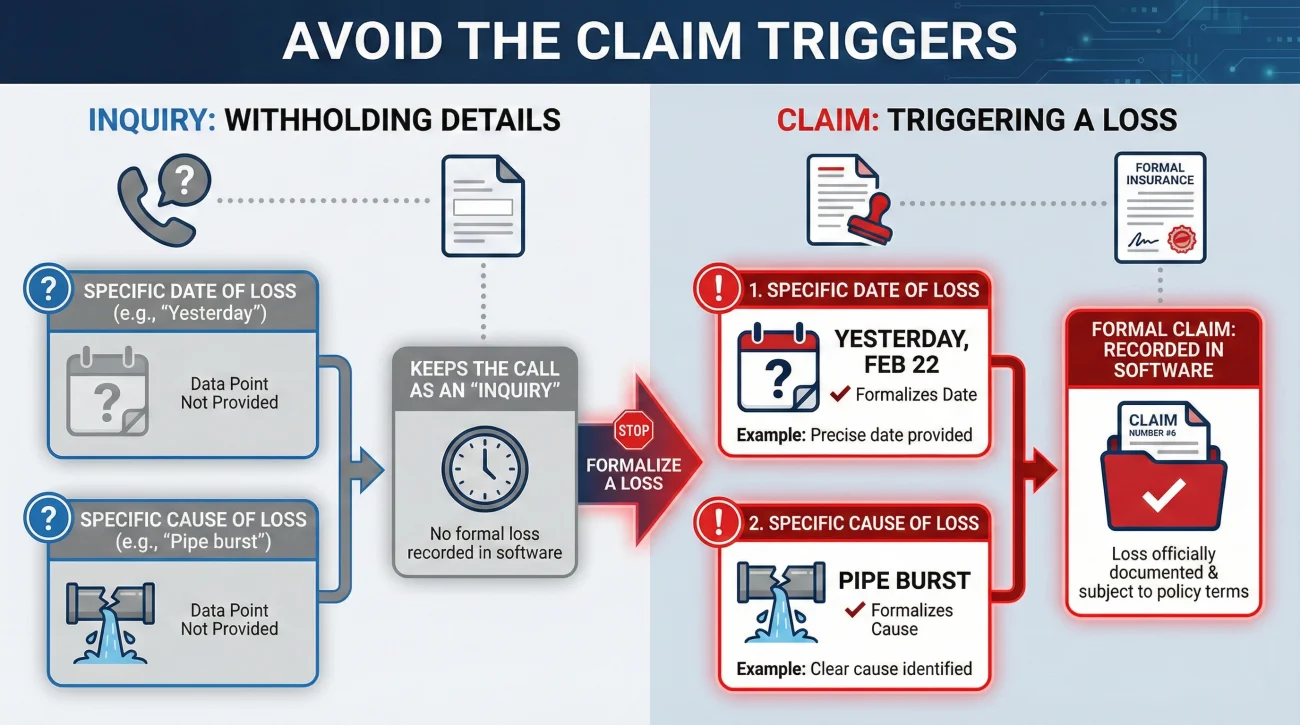

To avoid turning an inquiry into a claim, you have to withhold the two triggers that formalize a loss:

- ✅ Trigger 1: The specific Date of Loss (saying “yesterday” or giving a calendar date).

- ✅ Trigger 2: The specific Cause of Loss (saying “my kitchen caught fire” or “a tree fell on my roof”).

If you withhold those two specific details and speak in general terms, the agent often cannot complete the intake fields to generate a formal claim number.

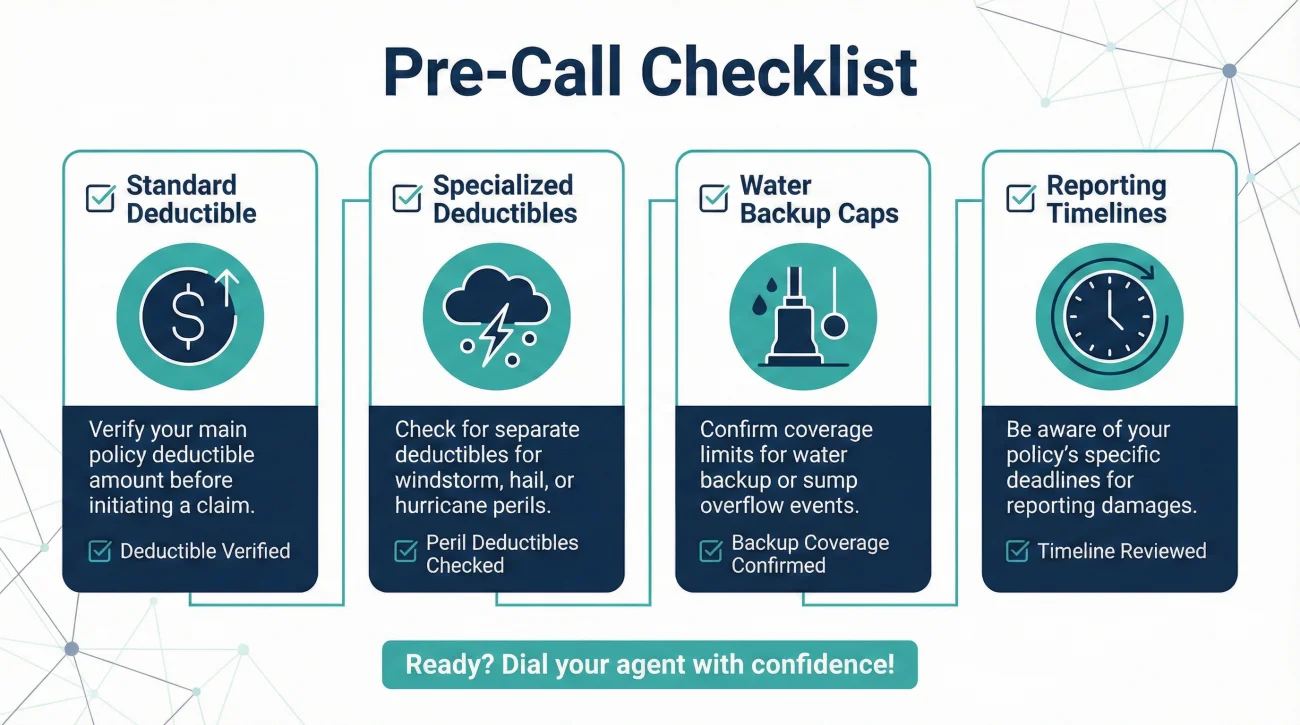

The Pre-Call Preparation Checklist

Before you pick up the phone, you need to know exactly what information you are trying to extract from the agent. Going into the call without a plan often leads to over-talking.

Equally important is knowing what you are not asking for. You are not asking for a coverage determination, and you are not asking them to estimate repair costs. You just need to verify your deductible, specific endorsements, caps, and reporting timelines so you can decide your next move.

Here are the facts you need to confirm:

| What to Ask About | Why You Need to Know |

|---|---|

| Your All-Peril Deductible | To know your out-of-pocket baseline for standard damage. |

| Specialized Deductibles | To check if wind, hail, or named storms have a higher percentage-based deductible. |

| Water Backup Endorsements | To see if you have specific caps on sump pump or drain backup issues. |

| Reporting Timelines | To understand if your policy requires you to report damage within a strict number of days. |

Scripts to Keep It in Contract Language

Knowing what to ask is only half the battle. You need to use language that clearly signals to the agent that you are requesting policy information, not reporting an event. Think of your opening sentence as a “gatekeeper” that frames the entire call: “I just have some policy questions today, no loss details to report.”

Here are practical scripts you can use to guide the conversation safely.

Script 1: The Deductible Verification

Use this script when you just need to know your financial baseline before getting contractor estimates.

Script 2: The Hypothetical Scenario

Use this script when you need to understand how a specific type of damage is treated under your policy.

Script 3: The Escape Line

Often, an agent will pause and ask you directly: “Did something happen at the house?” or “When did this occur?” You need a polite pivot to avoid answering.

Notice how these scripts avoid saying “I have damage.” They frame the questions as general financial planning. This gives the agent the freedom to explain the policy without feeling operationally pushed to document it as an active loss.

A Realistic Example: The Accidental Filing

Let’s look at how easily a casual conversation can slip out of your control. I once reviewed a file where the homeowner had a very small kitchen fire. It was mostly smoke damage, and they wanted to know if they should bother filing a claim.

The Mistake: The homeowner called the agent and said, “We had a small grease fire on the stove last night. We put it out quickly, but the cabinets are charred. My deductible is a thousand dollars, right? Do you think I should file this?”

By saying “last night” (Date of Loss) and “grease fire” (Cause of Loss), the homeowner provided the exact data points required to open a claim. The agent, following their corporate guidelines regarding fire risks, immediately logged it. Even though the homeowner decided the damage was only worth six hundred dollars and paid out of pocket, a zero-dollar claim for fire damage remained on their record.

The Better Approach: The homeowner should have used the deductible script. Once the agent confirmed the deductible was a thousand dollars, the homeowner could have thanked them, hung up, and gotten a contractor estimate privately.

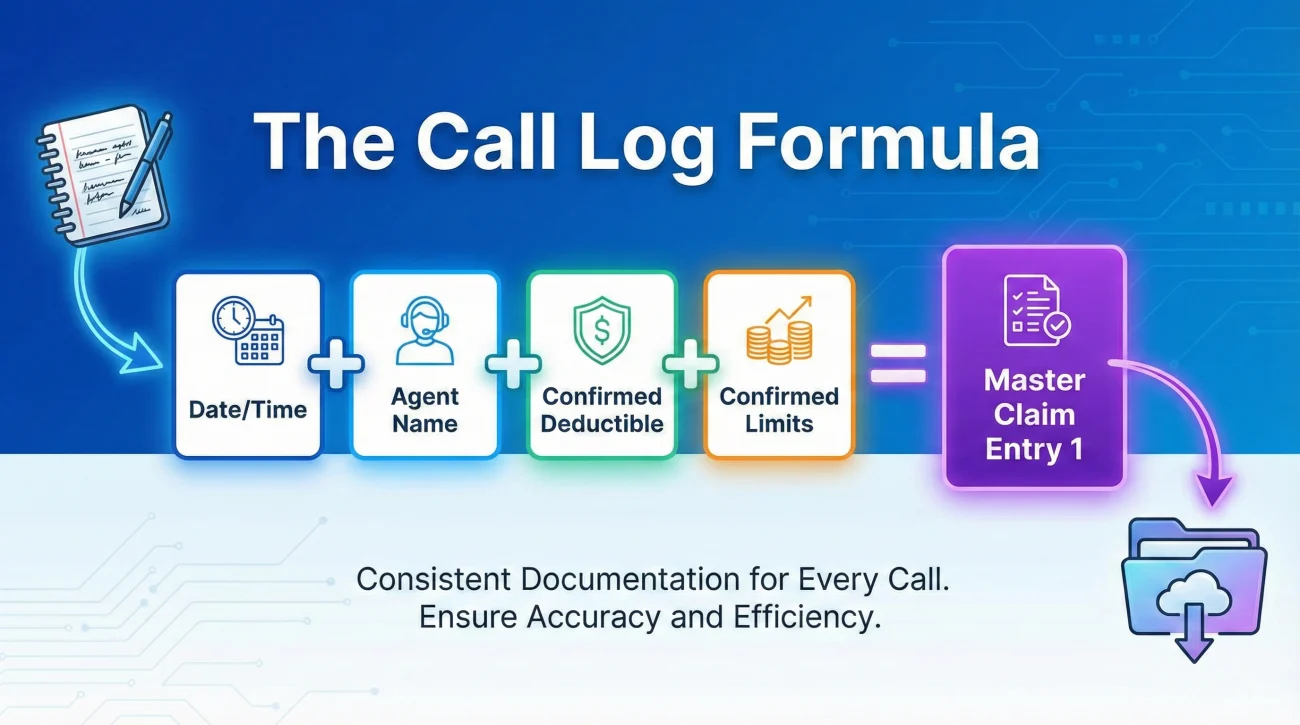

Documenting the Agent’s Advice

Even if you stay entirely theoretical, you must take meticulous notes. Whatever the agent tells you regarding your coverages, endorsements, or deductibles needs to be written down immediately.

Why? Because the agent’s verbal assurance does not override the written policy contract. If you later file a claim based on what the agent said, and the corporate adjuster denies it based on a policy exclusion, your notes will be your only reference point.

Create a simple log for this call. Note the date, the time, the exact name of the person you spoke with, and bullet points of what they confirmed.

[Date/Time] + [Agent Name] + [Confirmed Deductible Amount] + [Confirmed Coverage Limits]

If you evaluate your deductibles against contractor estimates and decide you must formally file, this call note becomes the very first entry in your master claim file. Staying strictly organized from day one is critical. I highly recommend setting up a structured system, which you can find in our Proof of Loss Playbook, to keep every conversation logged correctly.

Handling the “Just File It” Response

Often, when you ask an agent a hypothetical question about coverage, they will give you a non-answer. They might say, “Every situation is different, so it’s impossible to say for sure. You really just need to file a claim and let the adjuster come out and take a look.”

This is a common operational deflection. Agents are specifically trained not to make firm coverage determinations. They do not want to promise you coverage only to have the adjuster deny it later.

❌ Note: Do not let this deflection pressure you into filing prematurely. You have the right to secure independent contractor estimates before making a final decision.

If the agent pushes you to file, simply hold your ground with a polite but firm response:

What If an Incident Was Already Logged?

Sometimes, despite your best intentions, a conversation goes too far. If you realize you already gave specific loss details to your agent and suspect a claim might have been triggered, you need to verify it in writing to protect your history.

Send a short email to your agent asking: “Can you please confirm if a formal claim number was generated from our call yesterday?”

If they say yes, but you intend to pay out of pocket, reply immediately with: “Since I have not formally requested to file a claim and am handling repairs privately, please update the file notes to reflect this was an informational call and no claim is being pursued.”

While this does not guarantee the carrier will erase the internal record, it creates a clear paper trail showing your intent, which can be useful if questions arise during future underwriting reviews.

Final Thoughts Before You Make the Call

Calling your agent before filing a claim is a strategic move, provided you control the flow of information. You are in the driver’s seat right up until the moment you establish a formal date and cause of loss.

Take a deep breath, write your questions down, and stick to your scripts. Do not volunteer details that you are not ready to formalize on a permanent record. Gather your facts, get independent repair estimates if possible, and compare those numbers against the deductibles your agent confirms. Only then should you transition from a policy-only discussion to an official claim submission.

❓ FAQ

📞 Should I call my insurance agent before filing a claim?

Yes, doing so helps you verify deductibles and limits. Just ensure you withhold specific details about the event until you are ready to file.

🕵️♂️ Can my insurance agent see if I file a claim?

Yes. The agency and corporate claims departments share systems, so your local agent will typically see any formal record attached to your profile.

📈 Will calling my agent to ask a question raise my rates?

Simple policy questions rarely do. However, if enough details are shared to trigger an incident report or zero-dollar claim, some carriers may factor it into underwriting.

🛑 What happens if I call my agent but decide not to file?

If you only asked about policy terms, nothing happens. If you provided loss details and they logged it, it will likely show up as closed without payment.

📋 Does asking a hypothetical question count as an inquiry?

Yes, routine questions about deductibles or coverage explanations are standard policy service calls and do not trigger the formal intake process.

🗣️ How do I ask my agent about coverage without accidentally filing?

Frame the conversation around financial planning or an annual review, rather than discussing an active property issue.

⚖️ Can my agent tell me for sure if my damage is covered?

No. They can outline general policy terms, but the claims adjuster always makes the final coverage determination after an investigation.

📝 What should I write down when I call my agent?

Record the date, time, agent’s name, and any specific deductibles, limits, or exclusions they mention during the call.

⏱️ How long do I have to decide to file after speaking with my agent?

Most policies require prompt reporting once you decide to file. You should ask your agent about strict timeline requirements during your initial chat.

🔄 If I tell my agent about the damage, do I still have to call the main claims line?

Often the agent’s notes will automatically route to the main line, but you should always confirm in writing if they initiated the process on your behalf.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.