- Avoid using the word “flood” casually when reporting a claim; in insurance operations, a flood means rising outdoor water, not a burst pipe.

- Describe the observable source of the water (e.g., a broken supply line) rather than the catastrophic result, to ensure your claim gets the correct routing label.

- Prepare your facts before you make the initial intake call, and strictly record what the representative tells you regarding your claim classification.

The Danger of Casual Vocabulary on Day One

When you walk into your home and find two inches of water covering your living room floor, your natural instinct is to panic. If you are like most people, you pick up the phone, call your insurance company, and frantically say, “My house is completely flooded, I need help right away!” In everyday conversation, that sentence makes perfect sense. But in the world of claims operations, using that specific “F-word” can instantly trigger a massive administrative nightmare.

In my daily work managing claims operations and file hygiene, the single most common reason I see valid claims get incorrectly flagged or delayed on day one comes down to vocabulary. When we talk about water damage vs flood insurance, we are not just debating definitions. We are talking about two entirely different claim categories, handled by different departments, and often requiring completely different policies.

While exact classification and coverage always vary by policy and carrier, the operational reality is that the person answering your first phone call is usually an intake representative, not a seasoned adjuster. Their job is to listen to your words and select options from a dropdown menu in their system. If you say the word “flood,” they select the flood category. If you do not have a separate, specific flood policy, the system will automatically generate a denial path for that file. By the time a real adjuster looks at the notes and realizes it was actually a burst kitchen pipe, you have lost weeks trying to correct the paperwork.

This guide is about protecting your claim at the very first step. I will walk you through exactly how the system maps these terms, what words you should use to describe observable facts, and how to survive the initial intake call without accidentally miscategorizing your own disaster.

The Operational Difference: Where Did the Water Start?

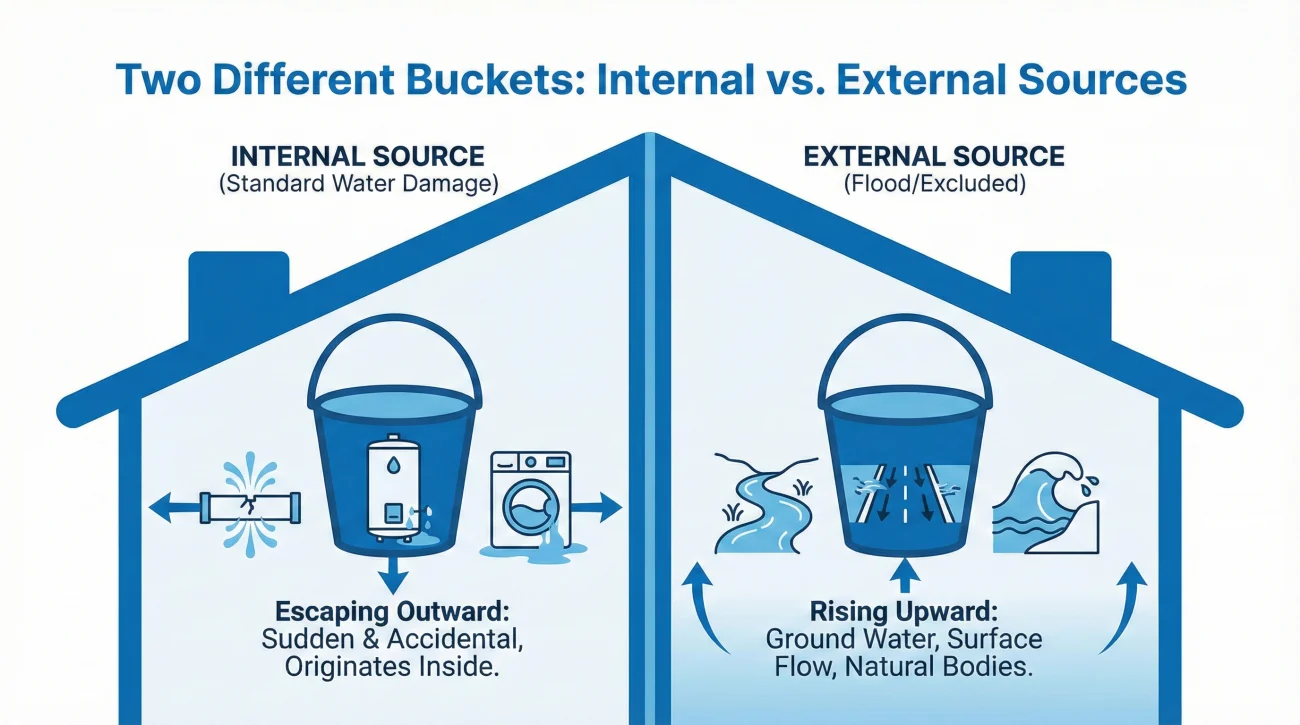

To navigate the intake process safely, you have to understand how the insurance industry categorizes water events. They do not care how much water is on your floor. They only care about how the water entered the space.

We train operations teams to look at the source. If the source is internal and sudden, it goes into one bucket. If the source is external and natural, it goes into another. Blurring these lines during your initial report is a critical mistake.

The “Water Damage” Bucket

Standard property water damage generally refers to water that escapes from an internal, artificial source in a sudden and accidental manner. This is the category most standard homeowners policies are built to address.

- ✅ A pressurized supply line under your sink ruptures.

- ✅ Your water heater tank suddenly bursts and releases its contents.

- ✅ A washing machine hose snaps mid-cycle.

In all of these cases, the water was supposed to be inside a pipe or an appliance, and an unexpected mechanical failure allowed it to escape into your home.

The “Flood” Bucket

In claims processing, a flood is a weather event or a natural disaster. The operational definition is often operationally treated as a general and temporary condition of partial or complete inundation of normally dry land. It is rising surface water.

- 🌊 A nearby river overflows its banks and enters your doors.

- 🌊 Heavy, sustained rainfall pools in your yard and rises above your foundation.

- 🌊 A coastal storm surge pushes seawater into your neighborhood.

Notice the stark difference. If water falls from the sky, hits the dirt, pools up, and enters your house, it is almost universally classified as a flood event. Standard policies typically exclude this, requiring a specialized external policy to handle the loss (though you should always check your specific declarations and endorsements to be sure).

| Factor | Standard Water Damage | Flood Event |

|---|---|---|

| The Source | Internal (Plumbing, Appliances, HVAC) | External (Rivers, Lakes, Surface Runoff) |

| The Movement | Escaping outward from a defined system | Rising upward from the ground |

| The Scope | Usually isolated to your specific property | Usually affects multiple properties in an area |

Gray Areas: When It Is Not Just a Pipe or a River

In reality, not every claim is black and white. There are several common “gray areas” that do not perfectly fit the simple burst pipe versus overflowing river analogy.

- 🔍 Sewer Backup: Water reversing course and coming up through your drains.

- 🔍 Sump Pump Failure: Groundwater filling a pit faster than the pump can eject it.

- 🔍 Foundation Seepage: Hydrostatic pressure pushing groundwater through microscopic cracks in your basement walls.

These scenarios often have entirely separate endorsements (add-on coverage) or specific exclusions. Even in these confusing scenarios, the operational rule remains the same: state the observable source and path (e.g., “water is actively backing up through the basement floor drain”). Do not self-label it. Let the desk adjuster determine the proper system tag.

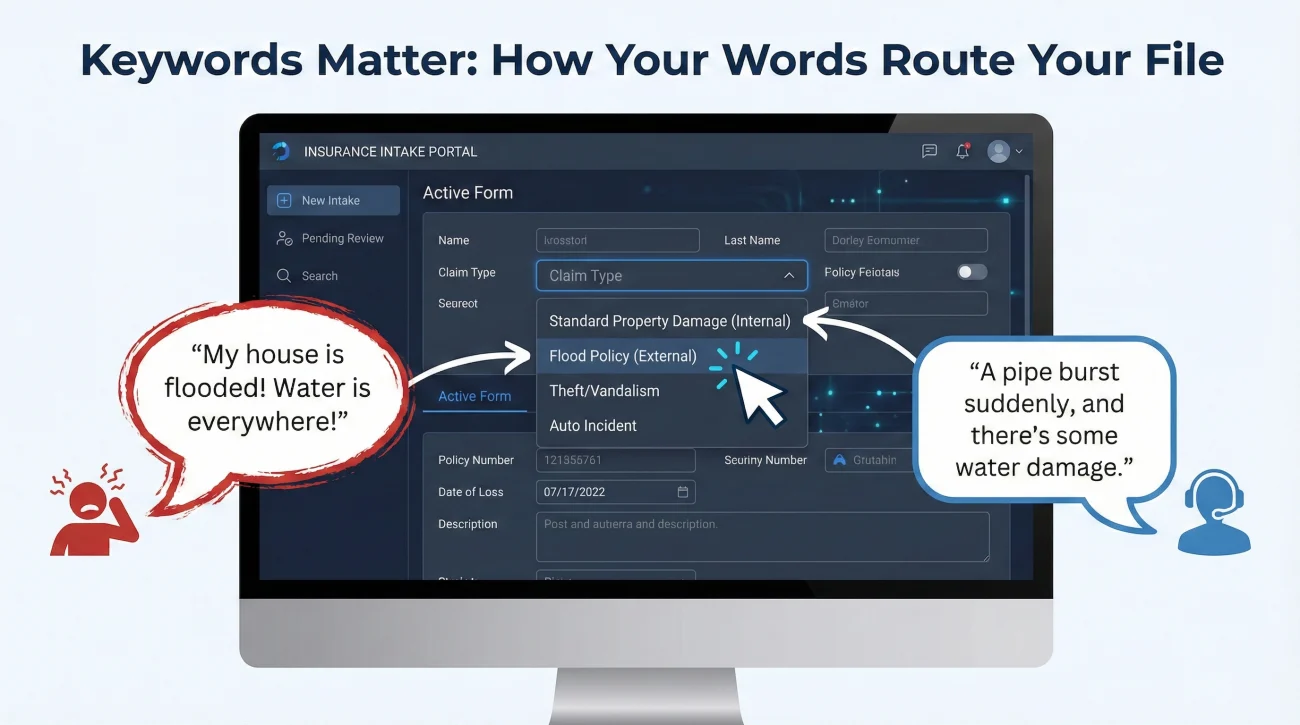

The Intake Call: How Representatives Route Your Claim

Understanding the difference is only half the battle. The real test happens during the First Notice of Loss (FNOL) call. This is the moment you formally notify the company that an event occurred. It is crucial to understand the psychology and the software on the other side of the phone.

The FNOL representative is typing exactly what you say into a text box, and then categorizing your claim based on those notes. They are trained to listen for keywords. If you are emotional and hyperbolize the damage, you feed them the wrong keywords.

Field Note: I frequently review intake logs where a perfectly covered plumbing failure gets tangled in red tape because the initial call notes read: “Insured called in panic, stated the entire downstairs is completely flooded.” The system reads “flooded,” assigns a catastrophic weather routing label, and triggers a coverage investigation. It can take weeks of administrative corrections, supervisor escalations, and repeated adjuster visits to pull the file out of the denial queue and get it back on the standard track.

To avoid this, you must stick strictly to observable facts. Do not diagnose the problem if you are not a plumber, and do not use catastrophic metaphors.

Real-World Scenarios: Words That Change Outcomes

Let us look at how the exact same physical event can be reported in two different ways, leading to completely different administrative outcomes.

Case 1: The Burst Kitchen Pipe

You come home from work to find water flowing out from under your kitchen cabinets and covering the hardwood floor in the living room.

“I need to file a claim! My house is completely flooded. There is water everywhere, the floors are ruined, it is a total disaster. I do not know what to do, it looks like a swimming pool in here.”

“I am reporting sudden water damage. A pipe under my kitchen sink burst suddenly this afternoon. The source is shut off now, but the escaped water has covered the kitchen and living room floors.”

In the “After” approach, you gave the intake rep exactly what they need for a clean system setup: the event type (sudden water damage), the observable source (pipe under sink), the timeline (this afternoon), and the current status (source is shut off).

Case 2: The Roof Leak

A severe storm blows through, damaging your shingles. The next day, you notice a large water stain on your bedroom ceiling and water dripping onto the carpet.

“The storm flooded my bedroom. Water is just pouring in from the ceiling and destroying the carpet.”

“I am reporting storm damage to my roof that has resulted in interior water damage. The wind damaged the shingles, and rainwater is now actively leaking through the ceiling into the bedroom.”

By framing it as storm damage resulting in an interior leak, you keep the claim out of the “ground water” category and accurately tie the internal water to the external covered peril (wind).

Case 3: Rainwater vs. Surface Runoff

A heavy storm hits. Rainwater hits your patio, pools up, and seeps under your back sliding door.

“The heavy rain flooded my living room. The water is coming right in from the storm outside.”

“Heavy rain accumulated on the back patio and entered the house under the sliding glass door.”

Why does this matter? Because “rain entering a house” sounds like a standard claim, but “rain pooling on the ground and entering” is the exact operational definition of surface water runoff (a flood). By stating the facts clearly, you allow the adjuster to apply the correct policy language, rather than arguing later over what your panicked “flooded” comment actually meant.

“Avoid using the word ‘flood’ unless a nearby river literally flowed through your front door. If it came from a pipe, an appliance, or a hole in the roof, it is a water damage event.”

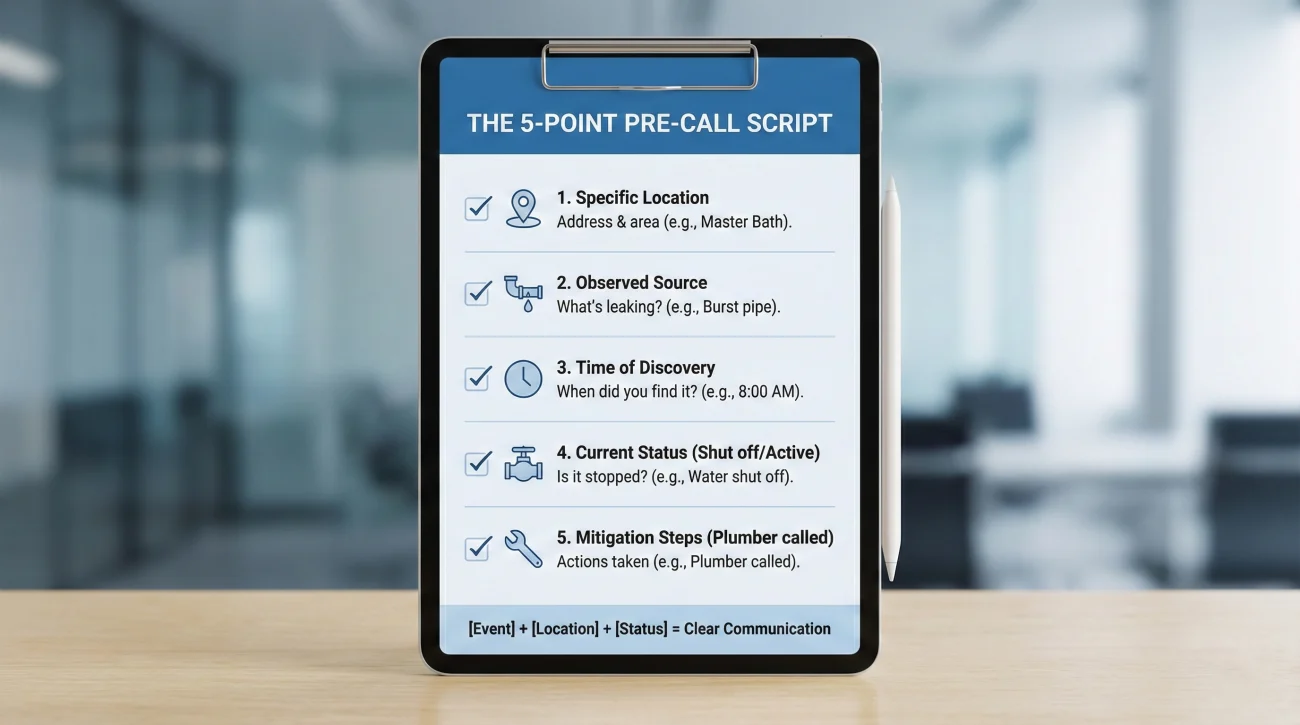

Safe Phrasing: Facts to Write Before You Dial

If you are preparing to make your intake call, write down your statement before you dial the number. Having a script keeps you focused and prevents nervous rambling. Keep your sentences short and strip out all emotion.

Before picking up the phone, jot down these five facts:

- ✅ Location: Which specific rooms are affected?

- ✅ Source Observed: Where exactly did you see the water coming from?

- ✅ Time Discovered: When did you first notice the issue?

- ✅ Current Status: Is the water shut off, or is it still actively flowing?

- ✅ Mitigation: Have you already called a plumber or a dry-out crew?

Using those facts, use this basic formula to construct your opening statement:

[Observable Event] + [Specific Location] + [Status of the Source]

Here are examples of clean, process-friendly phrasing you can adapt:

- 📄 “A pressurized water line to the refrigerator broke, releasing water into the kitchen.”

- 📄 “The washing machine malfunctioned and overflowed during a cycle.”

- 📄 “A pipe in the upstairs bathroom burst, and water has leaked down through the living room ceiling.”

⚠️ Warning: Avoid phrases like “it has been leaking for a while,” “slow drip,” or “gradual seepage.” Standard policies often distinguish between sudden events and long-term maintenance issues. Stick to what you discovered and when you discovered it, without guessing how long it was happening behind a wall.

Intake Questions You Must Ask Them

The intake call is not a one-way street. While the representative is gathering facts to open the file, you need to gather facts to set up your own tracking system. Do not hang up the phone without getting clear answers to the following operational questions.

Day-1 Clarification Script:

1. “Can you please provide the official claim number for this file?”

2. “Based on the notes you just took, how is this claim currently categorized in your system?”

3. “Am I cleared to contact a mitigation company to extract the standing water and dry the floors to prevent further damage?”

4. “By what exact date should I expect the assigned desk adjuster to make initial contact with me?”

Question 2 is your safety net. If the representative answers, “It is categorized as a flood,” you must immediately correct the record on the recorded line. You say, “Please correct that in the notes. This is not a surface water flood. This is internal water damage from a broken pipe.”

Intake Note Hygiene: What to Record

Just as the insurance company is recording your call, you must meticulously record the details of the conversation. Memory fades quickly during a crisis, and if a dispute arises later about how the claim was initially reported, your handwritten or typed log is your best defense.

Set up a simple intake log in your files. You only need a few specific data points for this first interaction:

- 📄 Date and Time of Call: The exact minute you connected.

- 📄 Representative Name: Ask for their first name and last initial or operator ID.

- 📄 Claim Number: This becomes the master key for every future document.

- 📄 Categorization Confirmed: Note what they told you about how the file is labeled.

- 📄 Mitigation Instructions: Did they say you could hire a dry-out crew? Write it down.

Once the file is categorized correctly, your next job is evidence packaging. I highly suggest reviewing our guide on organizing your proof of loss so you understand exactly how to label the photos and documents you are about to capture before the cleanup crews arrive.

❌ Note: Never rely on the insurance portal to act as your only record of the intake details. Portals can update, rewrite status descriptions, or experience glitches. Maintain your own independent communication log from minute one.

What If You Already Said the Wrong Word?

If you are reading this after you already made the initial phone call, and you realize you frantically told the intake rep your house was “flooded” due to a burst toilet, do not panic. It is a common mistake, but it requires immediate administrative correction to fix the file path.

You cannot un-say it, but you can formally clarify it in writing. Call back, but more importantly, send an email or a portal message to the assigned adjuster as soon as they are assigned. Use a reference-first response to clean up the record.

“Hello. I am writing to clarify the preliminary intake notes regarding my claim. During the initial emergency reporting, the word ‘flood’ may have been used colloquially to describe the amount of water on the floor. To be operationally clear, no external surface water entered the home. This loss is strictly the result of a sudden internal plumbing failure at the upstairs toilet supply line. Please ensure the file is categorized correctly as internal water damage.”

After sending this message, always request the updated category in writing, and ask for confirmation that the file was successfully re-routed to the standard property team. This puts a permanent, time-stamped correction into the file, forcing the adjuster to evaluate the claim based on the actual physical source rather than the panicked initial vocabulary.

Final Thoughts on Intake Discipline

The line between water damage vs flood insurance is strictly defined by the source of the water. When you make your First Notice of Loss call, you are not just asking for help; you are participating in a highly structured data-entry process. The vocabulary you choose in those first five minutes dictates the trajectory of your entire claim.

By removing emotion, avoiding catastrophic metaphors, and sticking strictly to observable facts about where the water came from, you ensure your file drops into the correct system tag. Treat the intake call like a business transaction. Prepare your script, ask clarifying questions, correct any misinterpretations immediately, and log every detail. A clean start prevents weeks of administrative friction later.

❓ FAQ

💧 Does standard home insurance cover water damage?

In most cases, standard policies cover sudden and accidental internal water damage, such as a burst pipe or a failing water heater. They generally do not cover gradual maintenance leaks or external ground water.

🌊 Is a burst pipe considered water damage or a flood?

A burst pipe is classified operationally as internal water damage. A flood specifically refers to rising external surface water or natural disasters affecting normally dry land.

🌧️ What happens if rain gets in my house, is that a flood?

If wind rips off your shingles and rain falls in, it is typically categorized as storm/wind damage resulting in interior water damage. If the rain hits the ground, pools up, and enters your home from the bottom, it is considered a flood.

🚽 My toilet overflowed, what kind of claim is that?

This is usually classified as accidental discharge or overflow of a plumbing system. Report it strictly as an internal plumbing failure, avoiding the word “flood.”

🗣️ What should I say when I call insurance for a leak?

Stick to observable facts. State what failed (the source), what room is affected, and whether the water is currently shut off. Keep emotion out of the report.

❌ Will my claim get denied if I accidentally say the word flood?

It can trigger an initial automated denial or route your file to the wrong department, causing severe delays. If you made this mistake, formally clarify the internal source of the water in writing immediately.

☔ Do I need separate insurance for ground water?

Yes. Damage from rising surface water, rivers overflowing, or storm surge almost universally requires a distinct, separate flood insurance policy to be covered.

🏠 How do adjusters know if it was a flood or just a leak?

Adjusters inspect the physical evidence. Flood water leaves a distinct, uniform mud or debris line across the lower areas of the property, whereas a plumbing leak creates localized damage originating from a specific internal source.

📞 Who do I call first when I find water in my house?

First, turn off the main water shut-off valve to stop the source. Once the active leak is stopped, call your insurance company to report the claim using fact-based language.

📝 What facts do I need to write down during my water damage claim call?

Record the location, observed source, time discovered, the representative’s name, your official claim number, and how the representative confirmed the claim is categorized.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.