- Filing a roof leak claim is fundamentally an exercise in categorizing facts: is this a sudden event or a maintenance issue? Your initial intake notes determine the path.

- Never guess the cause or the date on the first call. Insurance systems record your initial statements permanently, and contradictory timelines often trigger administrative delays.

- Before you pick up the phone or open the online portal, map out your “intake facts” including date of discovery, observable cause, and immediate actions taken to stop further water entry.

The Reality of Reporting a Roof Leak

In my years working in claims operations, I have watched countless files get tangled in administrative knots on day one simply because of how a roof leak was reported. When water is dripping into your living room or running down your drywall, your instinct is to pick up the phone, call the 1-800 number, and ask for help. But from an operational standpoint, the intake representative on the other end of that line is not there to diagnose your roof. They are there to input data points into a system.

That initial conversation is where the foundation of your entire claim is built. The system requires the representative to select specific codes from drop-down menus based on the words you use. If I look at a hundred delayed roof claims, the number one First Notice of Loss (FNOL) error I see is the caller accidentally mixing the date of a storm with the date they noticed the water stain. The system flags that timeline discrepancy immediately.

I always tell property owners that you do not need to be an expert in roofing materials or policy language. However, you do need to be highly disciplined about the facts you provide. The intake process is not a casual conversation; it is the formal creation of a permanent administrative record. My goal here is to share a clear framework so you can organize your intake facts before you make that call, ensuring your claim starts on a solid, consistent track.

The Two Core “Coverage Buckets” You Must Understand

When you report a loss, the intake software essentially attempts to sort your claim into one of two main administrative buckets in real-time. Understanding these buckets is critical because it dictates how you should prepare your intake notes. I cannot give you legal advice on what your specific policy covers, but I can show you how claims systems organize this data.

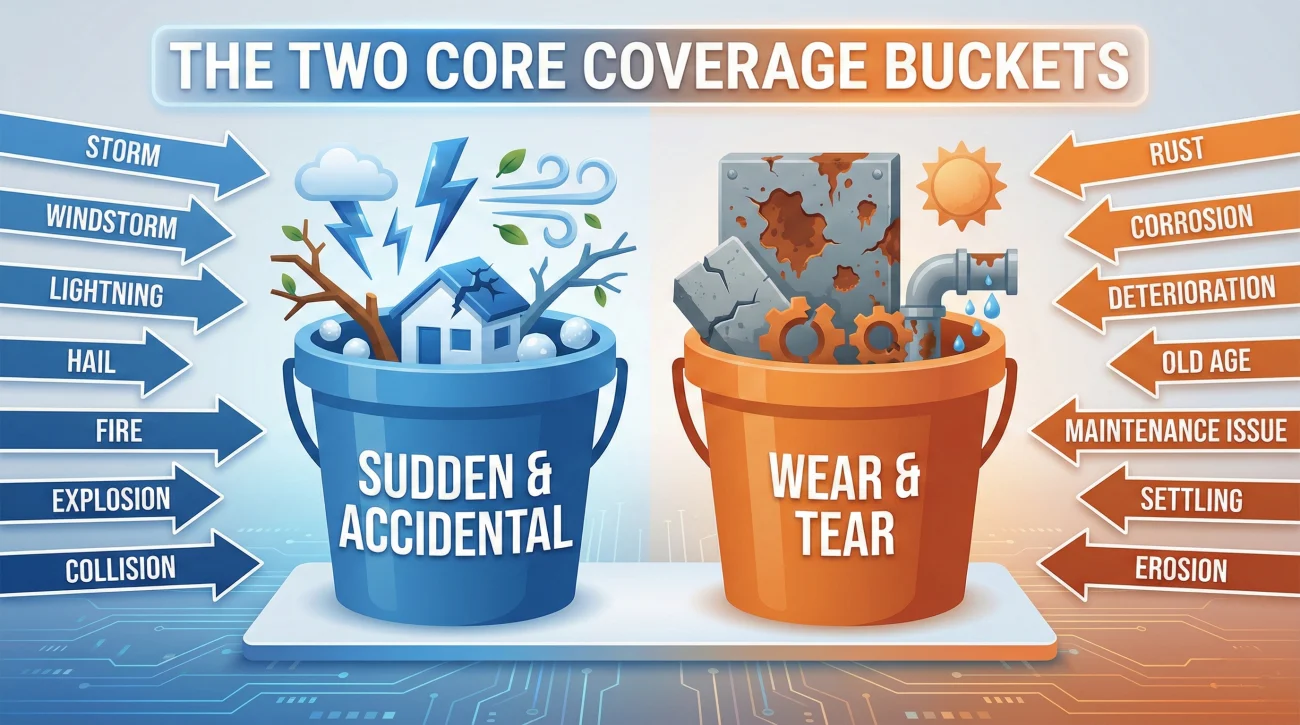

Bucket 1: The “Sudden and Accidental” Event

In claims operations, the smoothest files are usually those that clearly fit into the sudden and accidental bucket. This means there is a specific, identifiable event that occurred on a specific date, causing immediate and observable damage. For a roof, this often involves extreme weather.

From an intake perspective, the data points required to fill this bucket are highly specific. The system wants to know the exact date the storm hit, what kind of storm it was (wind, hail, heavy localized rain), and what immediate physical change occurred (e.g., shingles blew off, a branch punctured the decking). When you provide these facts clearly, the representative can select the appropriate peril code without ambiguity.

Bucket 2: The “Wear, Tear, and Maintenance” Framing

The second bucket is where claims stall. This is the maintenance, wear and tear, or long-term degradation bucket. No claims system likes ambiguity. When a property owner uses trigger phrases like “it has been happening for months,” “I patched it last year,” or “the roof is pretty old,” the system leans heavily toward maintenance.

Operationally, this does not just change a dropdown code. It triggers a completely different workflow. If your words frame the claim as a maintenance issue, it often prompts the adjuster to request your historical maintenance records, prior repair invoices, or a roofer’s history before they even schedule an inspection. You accidentally shift the burden of proof onto yourself right out of the gate.

“I just noticed water coming in. It rained hard yesterday, but honestly, the roof is pretty old and it might have been leaking slowly for a while without me noticing.”

“I am reporting water intrusion that occurred yesterday, October 12th, immediately following the severe windstorm. Prior to this event, there were no known leaks.”

Grey-Zone Scenarios: Handling Unclear Timelines

Not every roof leak happens while you are staring out the window. In reality, claims often fall into grey areas where timelines are not perfectly aligned. Here is how you navigate these common situations so the intake system does not misinterpret your claim.

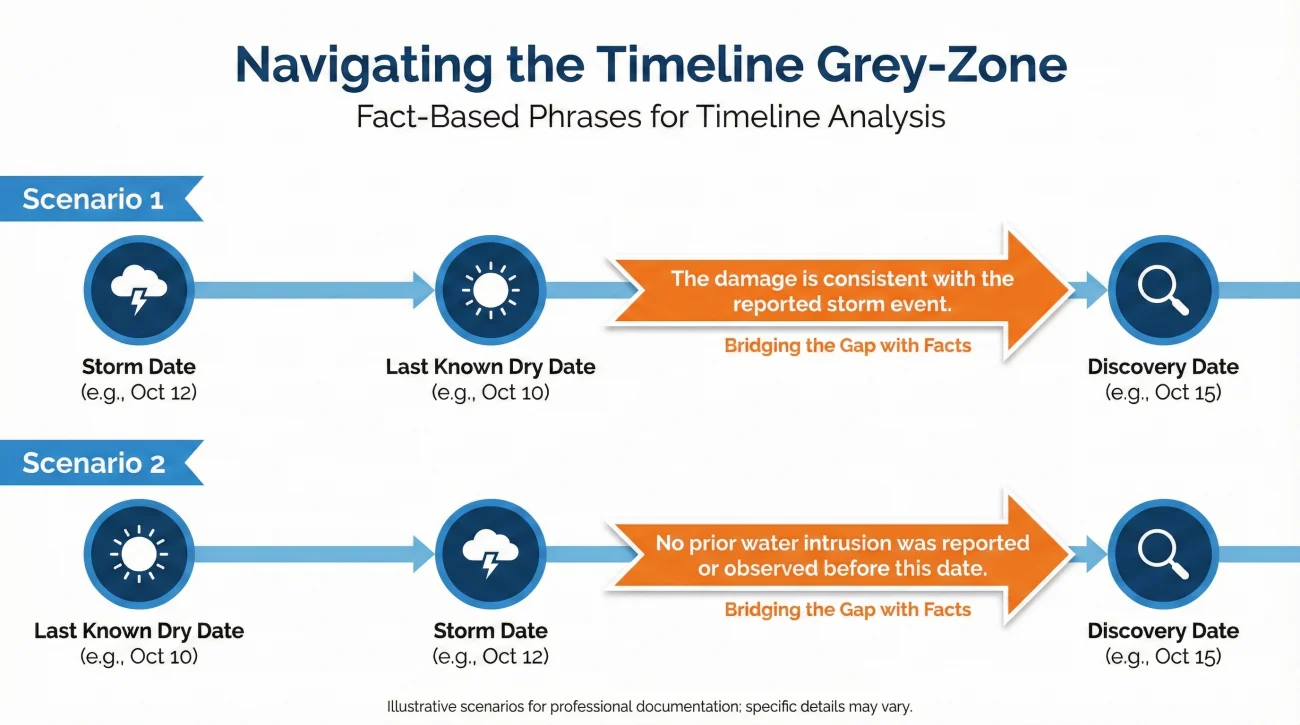

Scenario 1: The leak appears a few days after the storm

If you report that a storm hit on Tuesday but the leak started on Friday, the system immediately sees a timeline gap and questions the causation. To keep the record clean, you need to anchor the “last known dry time” and tie your discovery directly to the event. A safe way to frame this is: “I am reporting water intrusion discovered Friday. The last weather event was Tuesday’s severe windstorm, and there were no leaks prior to that.”

Scenario 2: You only know the “Date of Discovery”

Guessing a date is one of the fastest ways to get a file flagged, especially if weather reports show clear skies on the date you accidentally guessed. Instead of making an assumption, clearly separate your discovery from the actual event. Simply tell the representative: “I discovered the damage today upon returning home. The last known dry date was the 12th, and heavy storms occurred in my area on the 14th.”

Scenario 3: Multiple rainstorms hit back-to-back

Ambiguity about which specific storm caused the damage can trigger multiple deductibles or cause the rep to code the leak as an ongoing, long-term issue. In this case, focus tightly on when the internal damage actually appeared. A clean, factual report sounds like: “I observed new water intrusion today following this morning’s heavy rain. I cannot determine if prior storms weakened the exterior, but the interior leak began today.”

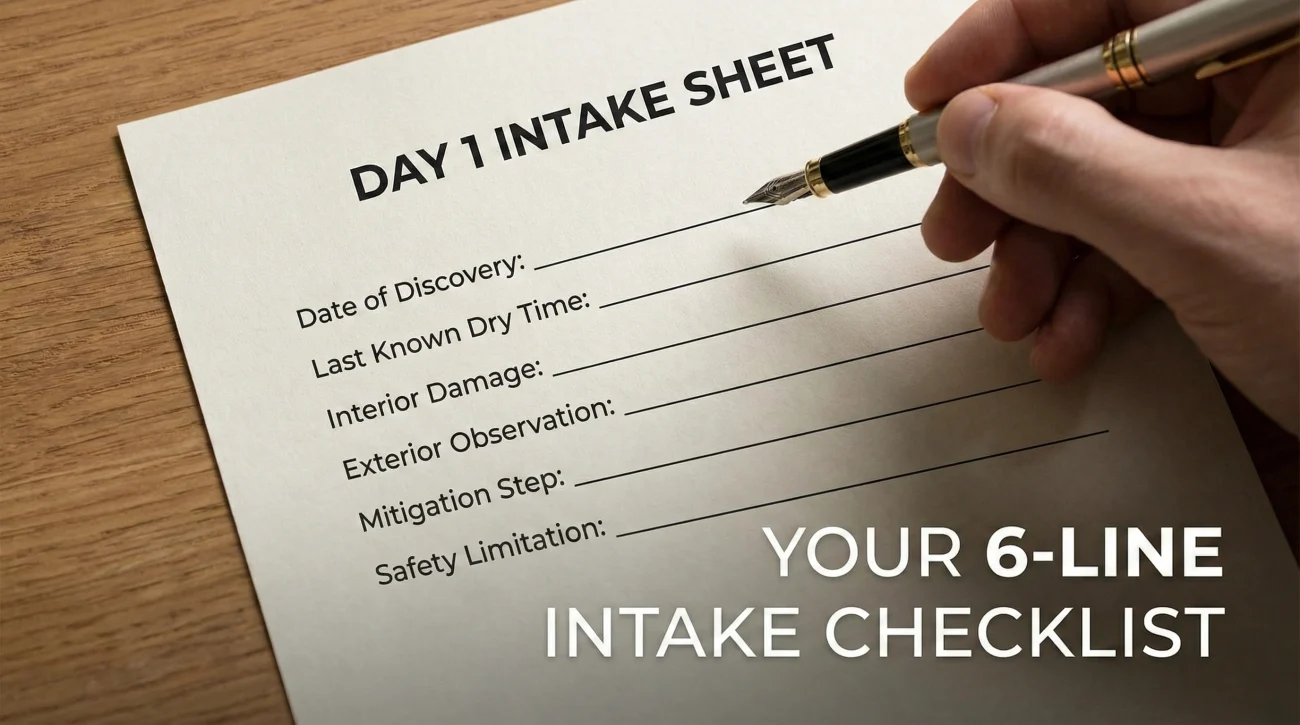

Setting Up Your 6-Line Intake Sheet Before You Call

In day-to-day claims ops, the fastest wins usually come from property owners who treat the process like a business transaction. I highly recommend setting up a dedicated file for your claim before you even make the first phone call. When you prepare your proof of loss playbook down the road, you will be thankful you established consistent facts on day one.

Grab a piece of paper. You need to create a “Day 1 Intake Sheet” with exactly six lines. This sheet will sit in front of you while you speak to the representative, and you will read directly from it. This prevents rambling.

My Day 1 Intake Fact Sheet:

Date of Discovery: [e.g., October 14, 2023 at 8:00 AM]

Last Known Dry Time: [e.g., October 12, 2023, before leaving for work]

Observable Interior Damage: [e.g., Active drip and new 2-foot water stain on living room ceiling]

Exterior Observation (From Ground): [e.g., Two shingle tabs visible in the front yard]

Mitigation Step: [e.g., Placed buckets, scheduled roofer for emergency tarping today]

Safety Limitation: [e.g., Cannot safely access roof to determine exact entry point]

By defining these exact fields beforehand, you strip the emotion out of the report. You are simply transferring data from your sheet into their system.

The “Offhand Comment” Mistake (What Not to Say)

I want to share a common pattern I see routinely in claims processing. A file comes across a desk, and the desk adjuster is reviewing the FNOL notes taken by the call center. The notes read: “Insured reports roof leaking. States roof is old and they knew it needed replacing soon, but the rain yesterday finally caused it to leak into the kitchen.”

That single sentence, often said as an offhand, honest comment by a stressed homeowner trying to be helpful, instantly changes the trajectory of the claim. The intake representative typed exactly what they heard. Now, the adjuster is forced to view the claim through the lens of delayed maintenance rather than a sudden weather event.

Key Point: Intake representatives are trained to type a narrative summary of your call. Every assumption, guess, or theory you offer about the age, condition, or history of your property becomes part of the permanent claim record. Stick strictly to the observable facts of the current event.

Tracking the Call: What to Log Immediately

Filing the claim is only the first half of the intake process; recording how the claim was filed is the second. In operations, we track everything, because verbal assurances mean nothing if a file gets lost or misrouted.

Before you hang up the phone, you must secure the primary tracking element: the claim number. This is more important than your policy number moving forward.

| What to Ask For | Why You Need It (The Operational Reason) |

|---|---|

| The Claim Number | This proves the system accepted the intake. Without it, the claim technically does not exist yet. |

| Name and ID of the Representative | Establishes a chain of custody for the First Notice of Loss. |

| The “Next Step” Timeline | Gives you a concrete deadline to follow up. (e.g., “An adjuster will contact you within 48 hours.”) |

If you used an online portal to file the claim, take a screenshot of the final submission page showing the generated claim number and the summary of facts you submitted, and save that image to your digital folder. This establishes your baseline proof of reporting.

How to Handle Questions You Cannot Answer

During the intake process, the system may prompt the representative to ask highly specific questions that you simply cannot answer from the ground. They might ask, “Are the underlayment membranes damaged?” or “What is the square footage of the affected roofing area?”

This is where many people panic and start guessing. From a process standpoint, guessing introduces bad data into the file, which later has to be corrected, causing confusion and delays.

Here is a safe, neutral way to handle technical questions during intake:

[Acknowledge the question] + [State your limitation] + [Suggest the next step]

“I understand you need the square footage of the damaged area, but I cannot safely access the roof to measure it. I am only reporting the visible missing shingles from the ground. We will need the field adjuster to determine the exact measurements during their inspection.”

This response is polite, sets a boundary, and keeps the intake record clean. It forces the representative to note “Pending Inspection” rather than inputting an inaccurate guess.

Final Thoughts: The “Decision Pressure” Trap

I see too many property owners walk into the intake process feeling like they have to prove their entire case on the very first phone call. You do not. Your job on day one is not to prove coverage, diagnose the roofing system, or argue about policy language. Your only job is to keep the administrative record clean so the field adjuster has a clear, factual baseline when they arrive to inspect.

Remove the pressure of being an expert. If you focus solely on establishing a tight timeline, reporting what you can safely observe from the ground, and documenting your mitigation efforts, you have done exactly what the system requires. Let the claims machinery do its initial sorting based on your organized facts. A claim that starts with disciplined neutrality is significantly harder to derail later in the process.

❓ FAQ

🌧️ Is a roof leak covered by insurance?

It depends entirely on the cause. Leaks caused by a sudden, accidental event like a windstorm or falling tree branch are typically categorized differently than leaks caused by long-term wear, age, or lack of maintenance. The initial facts you report help the system determine this categorization.

⏱️ How long do I have to report a roof leak?

You should report a loss as soon as you are safely able to discover and document the initial damage. Delaying the report can sometimes complicate the claim, as it becomes harder to differentiate between the initial event damage and subsequent secondary damage.

📝 Do I need to know the exact date the leak started?

Yes, providing a specific Date of Loss is a critical requirement for the intake system. If you were away, provide the date you discovered it and tie it to a known weather event that occurred during your absence, keeping your facts clear and consistent.

📸 What should I document before calling the insurance company?

Before calling, write down your intake facts: Date of loss, observable cause, interior damage, and mitigation steps. It is also wise to take basic, safe photos of the interior water damage and any visible exterior issues from the ground before things are cleaned up or tarped.

🛠️ Should I put a tarp on my roof before the adjuster comes?

Yes, taking reasonable steps to prevent further damage (mitigation) is generally expected. Placing a tarp to stop active water entry is a standard temporary repair. Just ensure you safely document the damage with photos before the tarp covers the evidence.

❌ What if I don’t know what caused the leak?

If you genuinely do not know, simply state the facts of what you see right now. “I discovered water dripping from the ceiling today. I do not know the external cause and will need an adjuster to inspect the roof.” Never guess or invent a cause just to fill in a blank.

🏚️ Will insurance cover a leak if my roof is old?

The age of the roof is a factor adjusters consider, but a sudden, severe weather event can damage roofs of any age. The key during intake is to focus your report on the specific sudden event that caused the current leak, rather than volunteering information about the roof’s lifespan.

📁 What happens to the notes the rep takes on the first call?

Those notes become the First Notice of Loss (FNOL) document. This is a permanent administrative record attached to your claim file. The desk adjuster and field adjuster will read these notes before they ever speak to you, which is why factual accuracy on day one is so important.

🗣️ If I already made a messy first call, can I correct the record?

Yes. Do not call back to argue. Send a brief, neutral written message through the portal or to your assigned adjuster clarifying the timeline: “To clarify my initial report, the date of discovery was X, and the severe weather event occurred on Y. Please update the file.” Keep it entirely fact-based.

💻 What if I used the wrong word on the online form?

If you accidentally selected a “wear and tear” option online, take a screenshot of your baseline submission. Then, use the portal’s messaging system immediately to issue a neutral correction: “I selected X in error; please note the cause of loss is observable wind damage from the [Date] storm.”

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.