- When reporting a claim, your job is to state observable facts, not to diagnose the root cause of the damage.

- Avoid guessing how long a problem has existed; using words like “probably” or “must have been” can lead to inaccurate claim routing.

- If you do not know the exact cause or timeline, stating “I just discovered this today” is a completely valid and reliable approach.

The Danger of Guessing on Day One

The moment you discover property damage, the instinct is to try and make sense of it. You look at a collapsed ceiling or a flooded utility room, and your brain immediately starts trying to solve the mystery. By the time you pick up the phone to report the claim to your insurance company, you might have already formulated a complete theory about how the pipe slowly rusted over the last ten years until it finally gave way.

In my time working in claims operations, I can tell you that this natural human instinct to be helpful is exactly where the wear and tear vs sudden damage insurance confusion begins. When you call the intake department, the representative on the other end of the line is typing down exactly what you say. They are filling out a First Notice of Loss document, often selecting options from rigid drop-down menus.

If you nervously guess that a leak “has probably been dripping for months,” that guess becomes part of your official claim record. It can immediately route your file into a complex review process, even if a plumber later proves the pipe burst cleanly just twenty minutes before you found it.

I want to guide you through how to describe your loss at intake using only observable facts. We are going to separate what you actually know from what you assume, ensuring your claim is categorized accurately based on reality, rather than a panicked guess.

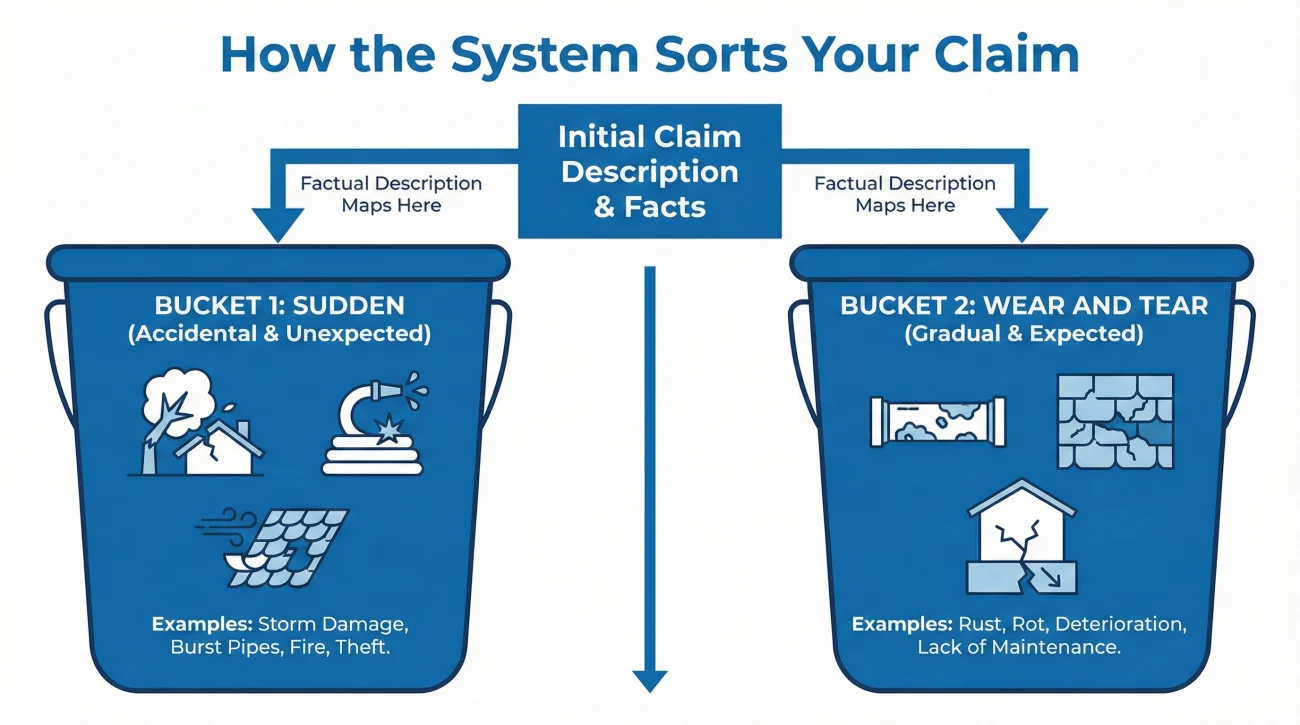

Understanding the Two Intake Buckets

While specific policy language and claim handling procedures vary by carrier and state, from an operational standpoint, the system is always trying to sort the event into one of several primary buckets. The two most common distinctions for internal routing at intake are sudden events and gradual deterioration.

You do not need to be an insurance expert or quote your policy to understand these buckets. You simply need to understand how the words you choose map to these categories.

| The “Sudden Event” Bucket | The “Wear and Tear” Bucket |

|---|---|

| Damage that happened clearly at a specific point in time. | Damage that occurred gradually over an extended period. |

| Examples: A tree falls on the roof, a washing machine hose bursts, wind rips off shingles. | Examples: A pipe slowly rusting, old shingles crumbling from age, chronic foundation settling. |

| Described using immediate facts: “I woke up and there was water,” or “I heard a loud crash.” | Often described using assumptions: “It looks like it’s been rotting,” or “It finally gave out.” |

The person answering your initial phone call or processing your web form is not an adjuster. They are not investigating the claim; they are simply recording your report. If your language blends the two columns above, you create immediate confusion in the system.

Principle 1: Stick to Observable Facts

The most reliable approach to reporting a claim is to pretend you are a neutral witness to a traffic accident. You only report what you saw, heard, felt, or smelled. You do not report what you think the internal mechanics of the situation might be.

Key Point: You are reporting the resulting damage you discovered, not diagnosing the mechanical failure that caused it.

Discovery Time vs. Failure Time

A crucial distinction in claims operations is the difference between when a component failed and when you discovered the resulting damage. You, as the property owner, only know the discovery time. The failure time (whether a pipe burst suddenly an hour ago or has been weeping for a week) is something a field adjuster or a specialized contractor will investigate later. Stick strictly to your discovery timeline at intake.

When preparing to file your claim, take a moment to write down only the raw data. What room are you in? What exactly is damaged? Is it wet, broken, or missing? When did you physically walk into the room and notice the change?

Field Note: The Danger of “Over-Explaining”

I commonly see homeowners get into trouble by trying to do the adjuster’s job before the adjuster even arrives. A typical pattern involves a homeowner finding a puddle under their kitchen sink. Instead of saying, “I found water pooling under my sink today,” they say, “My old sink plumbing finally rotted through because the seal has been bad for a while.” They just turned a simple factual discovery into a declaration of long-term maintenance failure, based on zero plumbing expertise. This is a common pattern in claims intake centers.

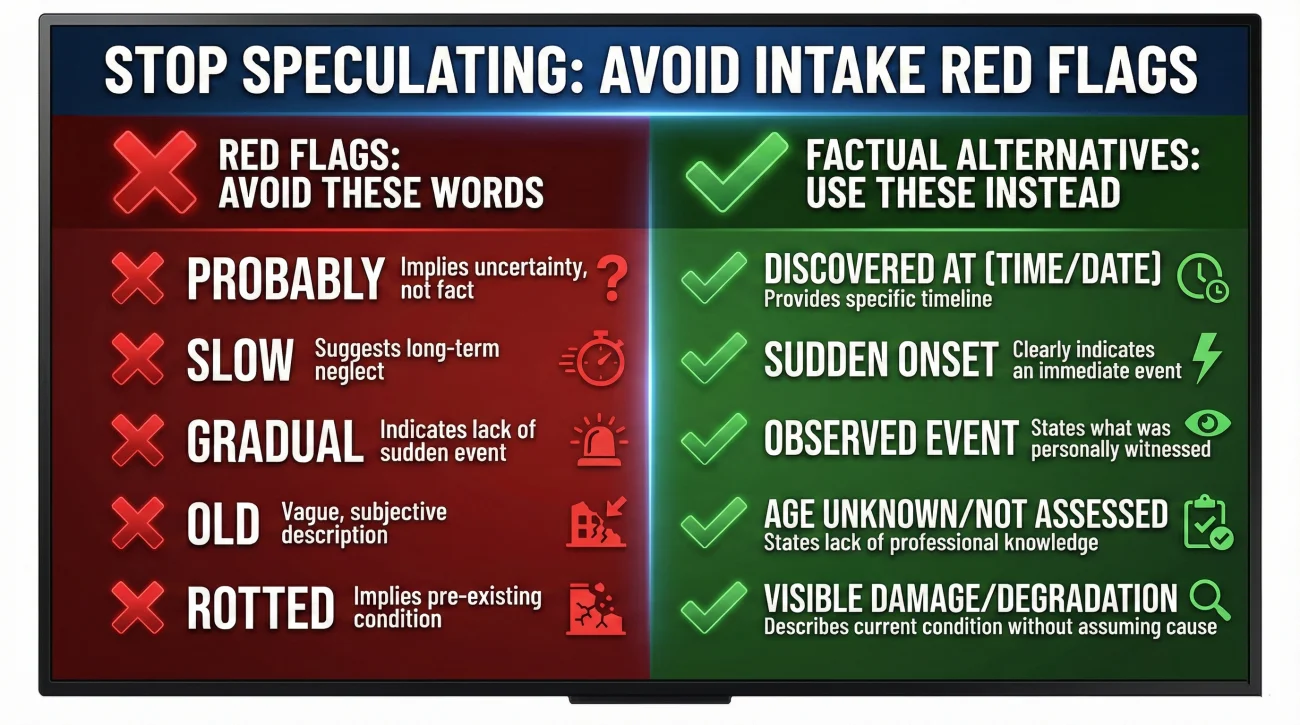

Red Flag Words to Avoid

Because intake systems rely heavily on keyword triggers, certain words can inadvertently signal that the damage is purely a maintenance issue. While you should never lie or hide facts, you should avoid using speculative words that paint an inaccurate picture of long-term neglect.

- ❌ “Probably” or “I guess”: These words mean you are speculating. (e.g., “It probably started leaking last week.”)

- ❌ “Slow” or “Gradual”: Unless you have been actively watching a leak for days, do not assume the speed of the failure. (e.g., “It looks like a slow leak.”)

- ❌ “Old” or “Rotted”: Age does not automatically mean wear and tear caused the specific failure, but saying “my old roof” shifts the focus away from the recent storm. If a contractor later confirms deterioration, you can update the record with their official report.

- ❌ “Always”: (e.g., “That window has always been a little drafty, but now it’s broken.”) Keep the focus on the current, distinct event.

By removing these speculative words, your report becomes clean, factual, and easy for the system to process correctly on day one.

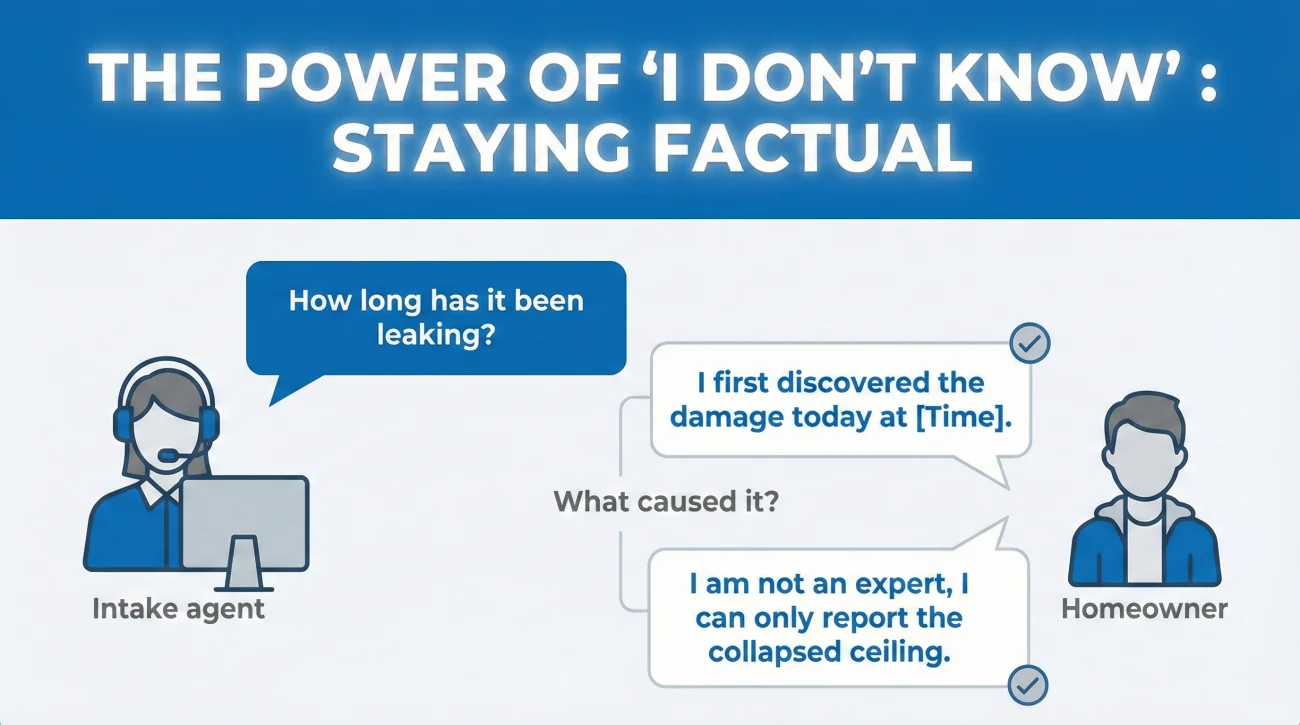

Principle 2: The “I Don’t Know” Script

When you call to report a loss, the representative will often ask direct questions to fill their forms. They might ask, “How long has this been leaking?” or “What caused the pipe to break?”

Many people feel pressured to provide an answer, fearing that saying “I do not know” will make their claim look suspicious. In reality, acknowledging that you do not know the technical cause is often the most honest and safest answer you can give.

If you genuinely just discovered the damage, you can use these simple, safe phrasing structures when speaking to intake or filling out an online form:

“I cannot say for sure when the component failed, but I first discovered the water/damage today at [Time].”When asked what caused the damage:

“I am not a contractor, so I do not know the exact cause of the failure. I can only report that the ceiling has collapsed and water is coming through.”

This phrasing does two important things. First, it anchors the timeline to your actual discovery of the event, which is sudden to you. Second, it politely declines to diagnose a mechanical issue, leaving that determination to the trained professionals who will eventually inspect the property.

Real-World Scenarios: Facts-Only Phrasing

To see how this works in practice, let us look at three common situations and how a slight wording change keeps your claim anchored in reality rather than speculation.

Scenario 1: The Dishwasher Leak.

Instead of guessing, “The hose behind the dishwasher finally wore out,” use facts-only phrasing: “I walked into the kitchen at 8 AM and found water pooling under the dishwasher. I have turned off the main valve.”

Scenario 2: Roof Leak After a Storm.

Instead of guessing, “The wind blew off my old, brittle shingles,” use facts-only phrasing: “Following last night’s storm, I noticed water dripping from the ceiling in the master bedroom.”

Scenario 3: Ceiling Stain After Vacation.

Instead of guessing, “The AC must have been leaking in the attic all week,” use facts-only phrasing: “I returned from a trip today at 4 PM and discovered a new, wet brown stain on the living room ceiling.”

In all three examples, you report the sudden event (finding the damage) and leave the analysis of the component’s structural integrity to the field inspector.

How to Correct the Record If You Misspoke

If you have already reported your claim and realize you used speculative language or guessed at the cause, do not panic. You can clarify your statement. Send a brief, written message to your assigned adjuster to correct the record and anchor your claim back to observable facts.

Subject: Clarification on Claim #[Your Claim Number]

Hello [Name],

I want to quickly clarify my initial intake statement. When I originally reported the claim, I speculated about the cause of the water damage. To be accurate, I am not a contractor and do not know the technical cause of the failure. I simply want the record to reflect that I first discovered the damage on [Date] at [Time]. I will provide the contractor’s diagnostic report once it is completed.

Thank you,

[Your Name]

Connecting Intake to Your Evidence

How you describe the damage on day one should align perfectly with the evidence you are gathering. If you state that you discovered a sudden influx of water, your day-one photos should show the immediate aftermath before cleanup begins.

💡 Pro Tip: If you are unsure how to organize the notes from your intake call alongside your photos, I highly recommend reviewing the proof of loss playbook. It helps you keep your documented facts and your visual evidence in a single, organized structure.

Keep a physical notepad next to you when making the initial claim report. Write down the exact phrases you use to describe the damage. This creates a baseline. If an adjuster calls you a week later, you can refer to your notes to ensure your story remains consistent. Consistency is a core component of a smooth claims process. If your intake report says one thing, and your conversation with the field adjuster implies something entirely different, you introduce unnecessary friction.

[Write down what you saw] + [Note the time of discovery] + [Read only those facts to intake]

Final

Navigating the wear and tear vs sudden damage insurance terminology does not require a law degree; it requires communication discipline. The intake phase of a property claim is about establishing the basic facts of the loss so the company can assign the right personnel and generate a claim number.

By focusing on facts versus assumptions, and describing the resulting damage rather than explaining the root cause, you protect the integrity of your claim. You ensure that the review process starts on a foundation of reality. Remember to write down your factual observations before you make the call, state clearly when you discovered the issue, and never be afraid to say that you do not know the technical cause of the failure. Let the professionals handle the diagnosis while you handle the factual reporting.

❓ FAQ

🤔 What is the difference between sudden damage and wear and tear?

Sudden damage refers to an unexpected, distinct event occurring at a specific point in time (like a burst pipe). Wear and tear refers to the gradual deterioration of an item over a long period (like slow rusting).

🏚️ Does homeowners insurance cover normal wear and tear?

In many standard policies, gradual deterioration and routine maintenance issues are not covered. This is why accurately reporting a sudden event without adding unnecessary guesses about age is vital.

🚰 How do I explain that water damage just happened?

State exactly when you found it. Instead of guessing how long a pipe has been dripping, say, “I walked into the room at 5 PM today and discovered water pooling on the floor.”

📅 Why did the adjuster ask how old my appliance is?

They are gathering data to determine the item’s lifecycle and potential depreciation. Answer factually if you know the age, but do not assume the age caused the specific failure.

🤷 What if I don’t know exactly when the damage started?

It is perfectly acceptable to state that you do not know the exact start time. Simply report the exact date and time you first discovered the damage.

💧 Is a slow plumbing leak considered sudden damage?

This often depends on the specifics of the investigation. However, at the intake stage, you should simply report finding the water rather than labeling the leak as “slow” yourself.

🛑 Can I guess the cause of the damage when filing a claim?

You should actively avoid guessing. Guessing the cause can inadvertently frame a sudden event as a long-term maintenance failure in the permanent claim record.

🗣️ What words should I avoid when describing the damage?

Avoid speculative words like “probably,” “must have been,” “slow,” “gradual,” or describing items as “rotted” unless you are quoting a professional report.

📸 How can I prove the damage is recent?

Take clear photos and videos immediately upon discovering the damage, before any cleanup begins. These timestamped files serve as your baseline visual evidence.

📝 What do I say if I am unsure if it is wear and tear or sudden?

State the facts of your discovery. Say, “I am not an expert, so I cannot diagnose the cause. I am calling to report that I just found this damage in my home today.”

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.