- Filing a claim without knowing your coverage buckets can lead to unnecessary denials based on how you describe the damage.

- Insurance generally covers “sudden and accidental” events, but usually excludes “wear and tear” or maintenance issues.

- Separate what you saw from what you think happened. Stick strictly to observable facts when speaking to your agent or intake rep.

- You can ask your agent hypothetical questions to understand your coverage, but always confirm if the conversation creates a claim record.

- To be clear: the goal is absolute honesty and clarity, not manipulating the system. You want to set up a clean file based on facts.

The Guessing Game Before You Hit “Submit”

If you are standing in your kitchen looking at a ruined hardwood floor, or staring at a tree branch resting on your roof, your first instinct is usually to pick up the phone. But right before you dial, the hesitation sets in. You find yourself asking: is this covered by homeowners insurance?

In my time working in claims operations, I have watched thousands of homeowners make the exact same mistake. They panic, they call the main intake line, and in their rush to get help, they start trying to play detective. Without realizing it, the words they use in that very first phone call can accidentally push their claim into a category that gets heavily scrutinized or denied.

I want to walk you through how the system actually categorizes damage. When an initial report comes in, it is not sorted by “good people” or “bad people.” It is sorted into buckets based on the facts provided. If you understand these buckets, you can communicate clearly, avoid self-sabotage, and set up your file correctly from day one.

💡 Pro Tip: The goal here is not to manipulate the system or hide damage. The goal is clarity. You must be honest, but you must also stick strictly to what you can observe, rather than guessing at the underlying cause.

How the System Views Damage: The Coverage Buckets

When you report a loss, the person on the other end of the line, or the portal you are typing into, is looking for specific triggers. They are essentially sorting your information into one of a few core buckets. Your goal is to provide accurate, factual information without accidentally volunteering theories that place you in the wrong bucket.

Bucket 1: The Sudden and Accidental Loss

This is the most straightforward bucket. In general, standard policies are designed to respond to events that happen suddenly, accidentally, and without warning. Think of a healthy tree blowing over in a storm and crushing your porch, or a washing machine hose bursting abruptly and flooding the laundry room.

From an operational standpoint, these are the cleanest files to set up because the timeline is clear. There is a distinct “before” and “after.”

Bucket 2: The Maintenance and Wear-and-Tear Trap

This bucket is where I see the most friction, confusion, and ultimate disappointment. Insurance is generally not a maintenance contract for your home. If a system fails because it is old, rusted, or poorly maintained, the resulting damage often falls into a grey area or is excluded entirely.

A common pattern I see is homeowners trying to be overly helpful by acting as amateur engineers. They will look at a leak and try to explain the mechanics behind it. My operational rule is simple: facts first, cause later. Leave the diagnosis to the professionals who will inspect the property.

Bucket 3: Exclusions and Limitations

Not every denial is based on wear and tear. Standard policies have specific boundaries. I find it helps to look at these in two distinct groups:

- ✅ Named Exclusions: Events the policy explicitly refuses to cover. The most common is outside flood water (rising water from a storm surge or river entering the home). Earth movement (earthquakes, sinkholes) is another standard exclusion.

- ✅ Limit-Based Items: Events that are covered, but capped. For example, mold resulting from a covered water loss might be covered, but limited to a strict dollar amount (like a $10,000 maximum). Additional Living Expenses (ALE) might also be capped by a timeline or dollar amount.

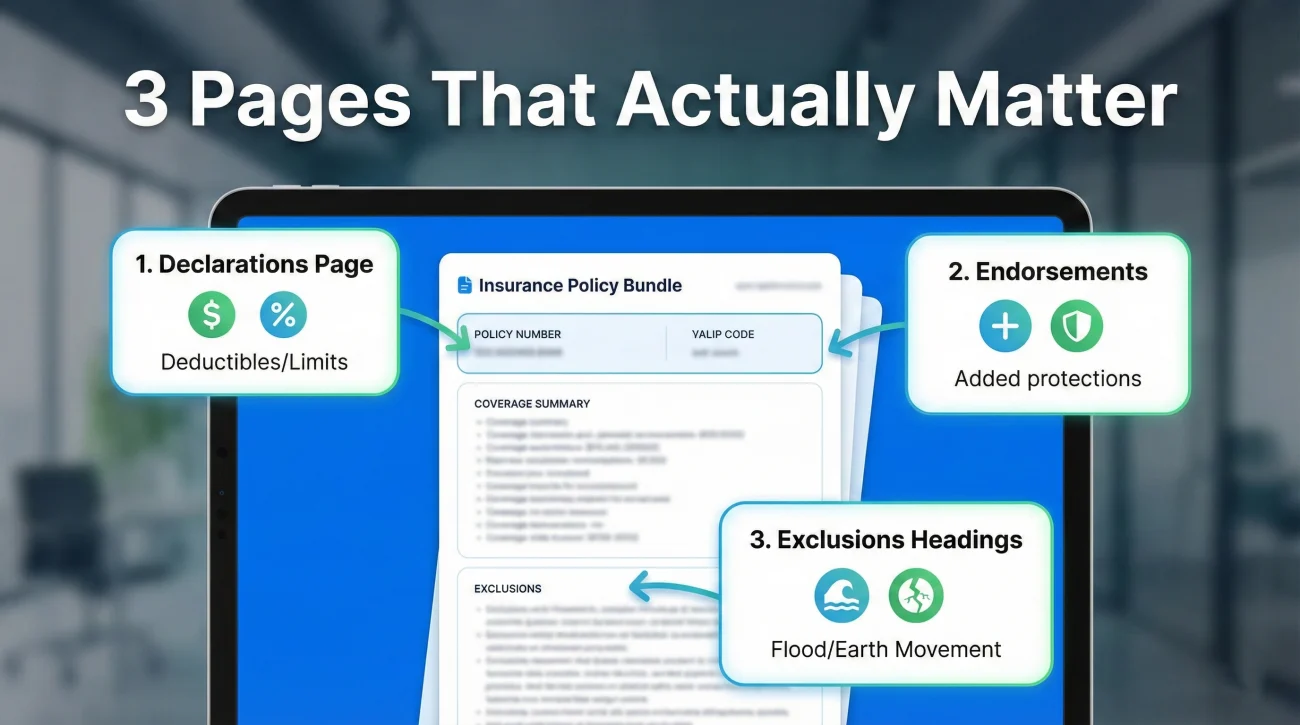

Where to Look in Your Policy (Without Reading 60 Pages)

You do not need a law degree to figure out your general coverage. Before you file, grab your policy document and look for these three specific areas to get your bearings:

- 📄 Declarations Page: Usually page one. It lists your core coverages (Dwelling, Personal Property) and, most importantly, your deductibles.

- 📄 Endorsements and Riders: Skim this section for added coverages you may have purchased, like water backup protection or scheduled valuables.

- 📄 Exclusions Headings: Look for bold headers in the main form. You will clearly see sections labeled “Earth Movement” or “Water Damage” (which usually outlines the flood exclusion rules).

The Questions to Ask Before You File

If you are unsure whether an issue is covered, you do not have to guess in the dark. Often, the smartest move is to have a conversation with your local insurance agent before you call the main 1-800 claims hotline.

Your local agent may be able to review your policy and explain your coverage buckets without necessarily opening a formal claim immediately. However, procedures vary by carrier. Before discussing specifics, you must protect your claim history.

Example Script: Asking for Policy Clarity Safely

This approach allows you to gather vital information about your coverage buckets calmly. You can confirm your deductible amount, which is critical. Filing a claim for a payout that barely covers your deductible does not just waste time; it adds a claim to your history, which can impact your future premiums or renewal eligibility.

Field Notes: When Over-Explaining Goes Wrong

To show you exactly how this plays out in real claims operations, here are two common scenarios where a single sentence at intake caused massive headaches for the homeowner.

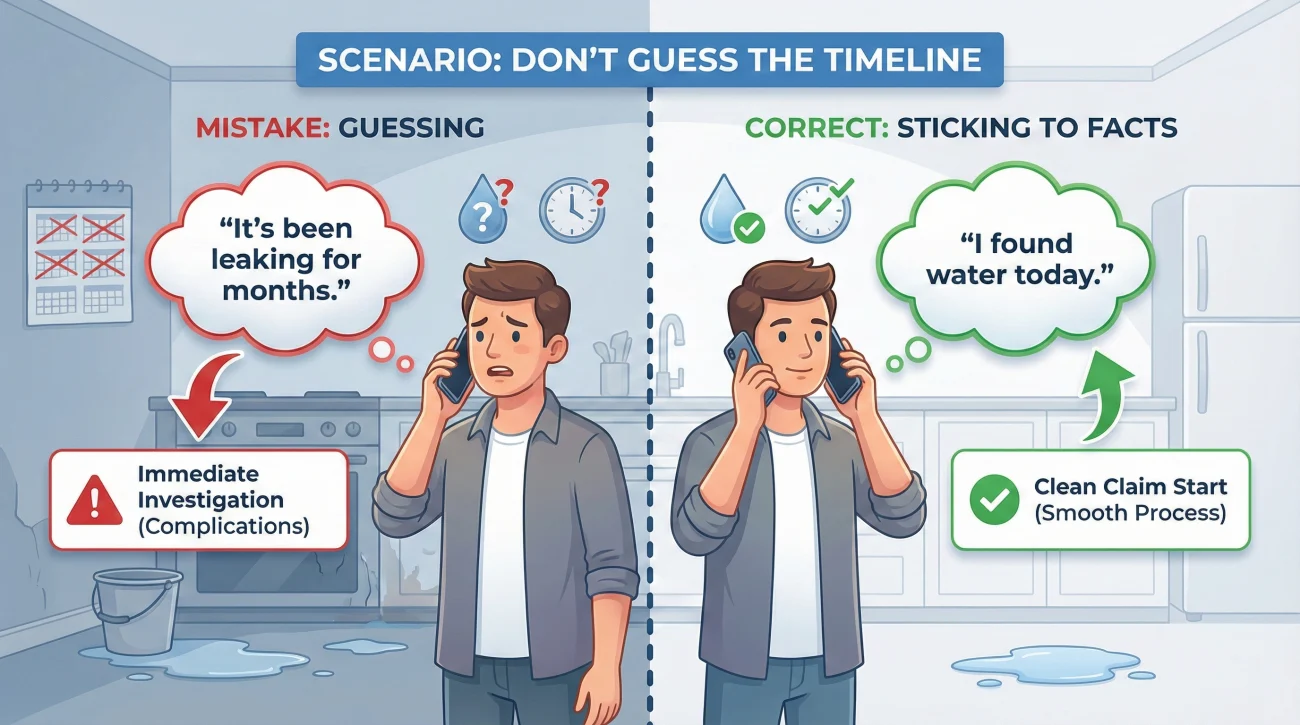

Scenario 1: The “Slow Leak” Admission

A homeowner discovered a pool of water near their refrigerator. Panicked, they called intake and said, “The ice maker has probably been leaking slowly behind the fridge for months, and the floor is finally ruined.”

Because they guessed the timeline (“for months”) instead of stating what they actually knew (“I found water today”), the claim was immediately flagged for a long-term wear-and-tear investigation. The adjuster demanded years of maintenance records. If the homeowner had just stated the facts, the investigation would have started on much cleaner ground.

Scenario 2: The Wind vs. Tree Confusion

A heavy storm blew through, and a tree branch scraped the side of a house. The homeowner told intake, “That old, rotting tree finally dropped a branch on my siding during the windstorm.”

By diagnosing the tree as “rotting,” the homeowner handed the insurer an easy reason to investigate failure to maintain the property. The fact was simply that a storm blew the branch down. The condition of the tree is for the adjuster to determine on-site, not for the homeowner to guess on the phone.

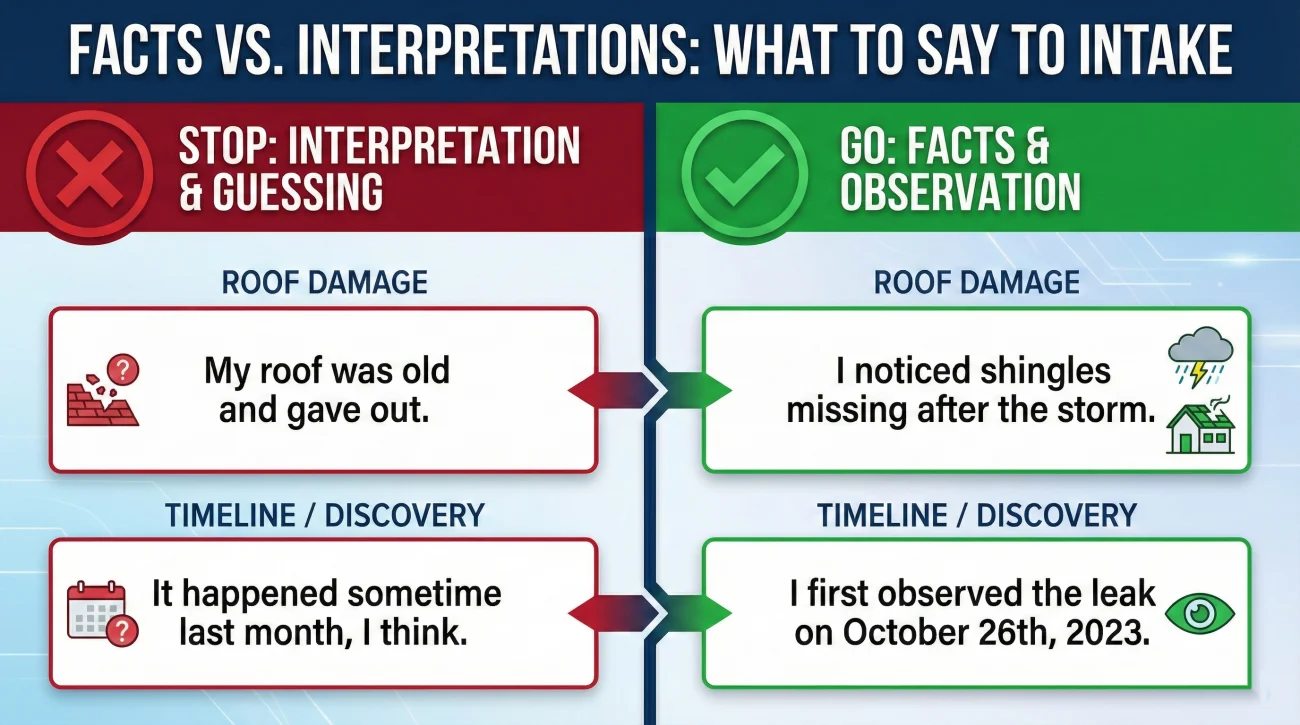

Organizing Proof: Facts vs. Interpretations

Once you understand the basic coverage buckets and have decided that you probably need to file, your next step is crucial. Do not just pick up the phone and start talking. You need to organize your facts.

In my experience, a scattered intake call leads to a messy file. When a file is messy from day one, it suffers from delays, miscommunications, and constant requests for clarification. You want to be the organized homeowner who provides a clean timeline.

Here is a cheat sheet on how to separate interpretations (which hurt your claim) from observable facts (which build your proof):

| ❌ Interpretation (What to Avoid) | ✅ Observable Fact (What to Say) |

|---|---|

| “My roof was old and finally gave out during the rain.” | “I noticed shingles missing in the yard after the storm on Tuesday.” |

| “The pipe under the sink failed due to age.” | “I opened the cabinet at 8:00 AM and found standing water.” |

| “The foundation shifted and cracked the drywall.” | “A crack appeared in the living room wall this week.” |

Documenting these intake facts is just the beginning of building a strong file. To see how these initial notes fit into the bigger picture of substantiating your loss, I highly recommend reviewing our complete proof of loss playbook. It outlines exactly how to transition from your day-one notes to a fully organized evidence package.

❌ Note: Never throw away damaged items or broken parts (like a ruptured hose or failed valve) until the adjuster has explicitly given you written permission to do so. Those items are the physical proof of what happened.

Final Thoughts on Navigating Coverage

Figuring out if a specific event is covered by your homeowners insurance is not about finding a magic loophole. It is about understanding the basic structure of your policy and communicating the observable facts clearly.

Remember, insurance policies vary by carrier and state. Nothing in this process is a guarantee of a payout. Stay calm, avoid self-diagnosing the damage, and keep your initial reports strictly factual. By approaching the situation methodically, you protect your file from unnecessary complications and set a clear path forward for the rest of your claim.

❓ FAQ

🔍 How do I find out what my home insurance covers without filing a claim?

You can read your policy declarations page, which lists your coverages and deductibles. Alternatively, you can call your local insurance agent and ask general, hypothetical questions about how your policy handles specific scenarios like storms or sudden leaks.

💧 Are sudden water leaks covered by homeowners insurance?

In many cases, standard policies cover water damage if it is sudden and accidental, such as a burst pipe or a failed washing machine hose. However, they typically do not cover water damage resulting from unresolved maintenance issues or slow, long-term leaks.

🏠 Does home insurance cover roof replacements?

A policy generally covers roof repairs or replacement if the damage was caused by a covered peril, like a sudden windstorm, hail, or a fallen tree. It rarely covers a roof replacement simply because the shingles are old and have reached the end of their lifespan.

🦠 Is mold covered by homeowners insurance?

Mold coverage is highly dependent on the source. If mold grows rapidly as a direct result of a covered, sudden water loss (like a burst pipe), it may be covered up to a certain limit. Mold caused by high humidity or a slow, ignored leak is usually excluded.

🔧 Does homeowners insurance cover plumbing issues?

Your policy may cover the damage caused by the plumbing failure (like ruined drywall or flooring), but it almost never pays to repair or replace the actual broken pipe or plumbing appliance itself. That is considered a maintenance expense.

🛑 What is generally not covered by standard home insurance?

Standard policies typically exclude damage from outside flooding, earthquakes, earth movement, pest infestations, and general wear and tear or lack of maintenance. You usually need separate policies or riders for floods and earthquakes.

🧱 Does homeowners insurance cover foundation repair?

Foundation repairs are usually excluded if the damage is caused by natural settling, earth movement, or poor construction. Coverage might only apply if the foundation was damaged by a very specific covered peril, like a massive plumbing failure, but this is rare and complex.

🌳 Does home insurance cover tree damage?

If a healthy tree falls due to a storm and damages a covered structure (like your house or fence), it is usually covered. If the tree falls just in your yard without hitting anything, or if it fell because it was dead and rotting, coverage may be limited or denied.

📋 How do I check my coverage limits before filing?

Review the Declarations Page of your insurance policy document. It outlines the maximum amounts the insurer will pay for dwelling structure, personal property, and liability, as well as listing your deductibles.

🚗 Does homeowners insurance cover theft from my car?

Yes, in many cases, the personal property coverage within your homeowners or renters policy extends to items stolen from your vehicle, even if the car was not parked at your home. Your auto insurance usually covers the car itself, while home insurance covers your stolen belongings.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.