- The words you use on day one decide which coverage bucket your claim lands in.

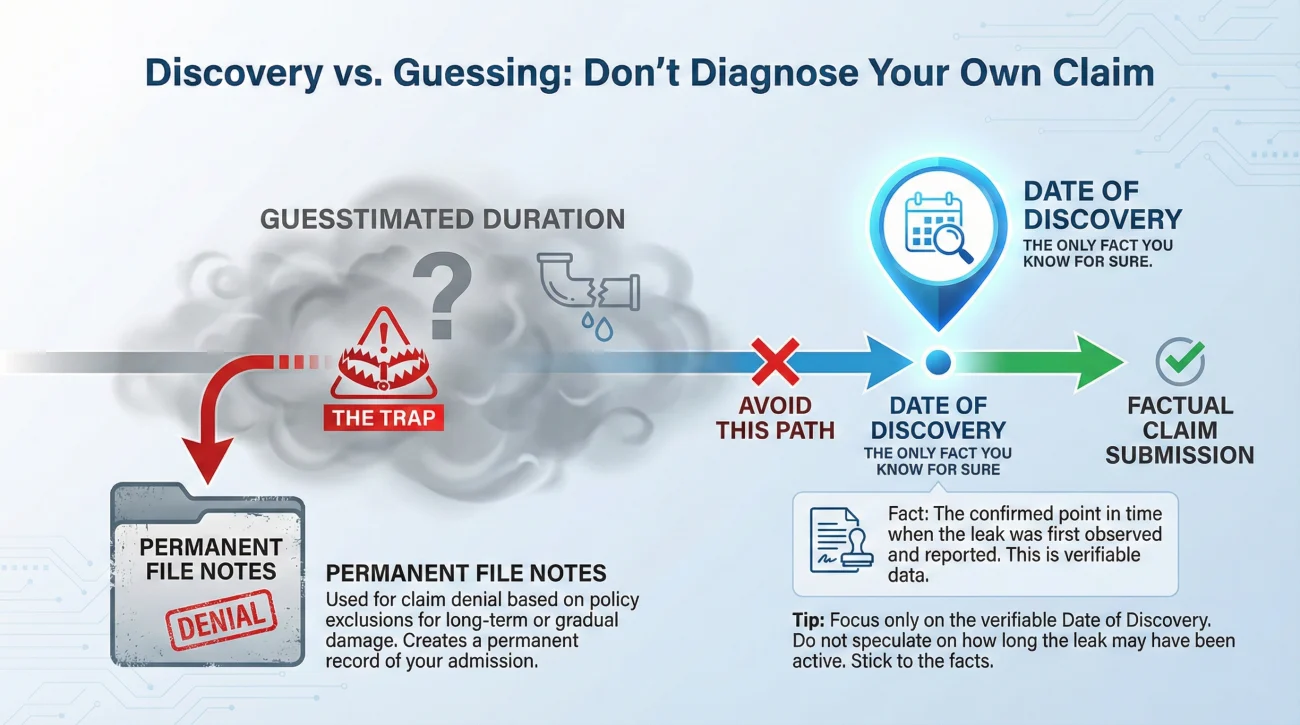

- Stick exclusively to observable facts when reporting a loss. Do not guess how long a leak has existed.

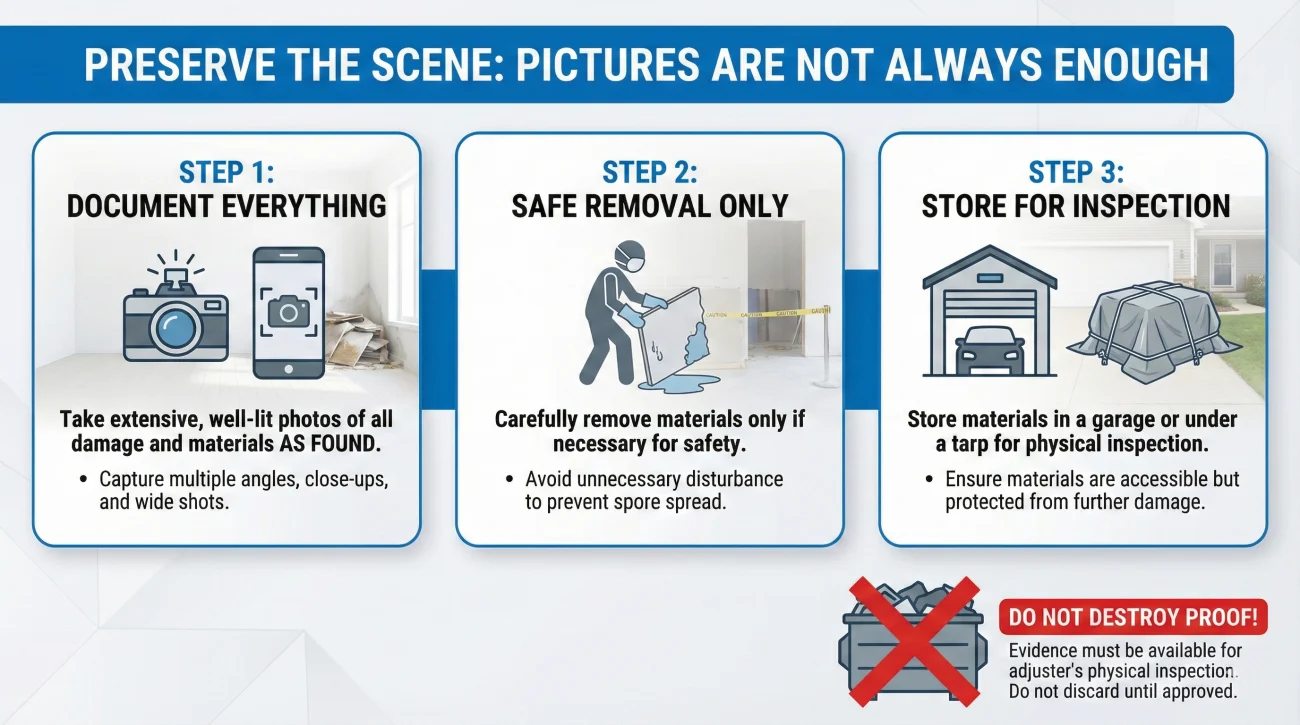

- Keep wet, damaged materials available for inspection; throwing them away too early can ruin your timeline proof.

The Reality of Reporting Mold Damage

In my time working in claims operations, I have watched hundreds of homeowners call in to report property damage. When it comes to discovering dark, fuzzy spots on drywall or under a sink, panic usually takes over. People call their insurance company immediately, but in their rush, they often say things that completely alter the trajectory of their claim.

The core issue is that whether mold covered by homeowners insurance is approved or denied frequently comes down to the very first conversation you have with a claims representative. That initial call is called the First Notice of Loss (FNOL). The person on the other end of the line is typing your words into a system, and those notes become the foundation of your file. While coverage specifics, limits, and mold endorsements vary wildly between insurance carriers, the core principles of intake hygiene stay exactly the same.

I always tell people: you are not an investigator, and you are not a plumber. You are an observer. Your job on day one is to report exactly what you see and what you know to be true at that exact moment. When homeowners try to be helpful by guessing the origin of the water or estimating how many weeks something has been leaking, they often walk themselves straight into a “wear and tear” denial. This guide is built to help you navigate that first phone call, organize your facts, and keep your claim strictly rooted in observable reality.

The Coverage Bucket Map: Where Your Claim Lands

Before you pick up the phone to report your damage, you need to understand how the person on the other end of the line is categorizing your situation. In claims operations, every detail you provide is used to drop your file into a specific “bucket.” Depending on the bucket you land in, the path forward will look very different.

For mold and water damage scenarios, there are generally two main buckets established during the intake phase.

| Bucket 1: Sudden and Accidental Event | Bucket 2: Long-Term Maintenance Issue |

|---|---|

| A pipe burst, a water heater failed suddenly, or a storm broke a window allowing rain in. | A slow drip under a sink, a roof that has been slowly leaking for months, or poor bathroom ventilation. |

| The timeline of the damage is clearly tied to a specific, recent event that you can point to. | The timeline is vague, and the damage appears to have been developing gradually over a long period. |

| Usually triggers a standard adjuster assignment and a clear path to inspection. | Often triggers immediate scrutiny, requests for historical maintenance records, and high risk of denial. |

The goal is not to trick the system. If you have a maintenance issue, it is what it is. However, a common pattern I see is a homeowner experiencing a genuine sudden event (like a pipe bursting behind a wall while they were out of town), but because they found mold a few days later, they over-explain and accidentally make it sound like a long-term neglect issue. You have to understand that mold can grow quickly. Just because it is present does not automatically mean a leak has been happening for six months.

The “Long-Term Leak” Trap (And How We Fall Into It)

When you call to report the claim, the intake representative will ask you when the damage occurred. This is where the trap is set, not out of malice, but out of procedural necessity. They need a “Date of Loss” to open the file.

I frequently review initial call transcripts where the homeowner, trying to be as honest as possible, starts speculating. They might say, “Well, I just found it today, but honestly, looking at it, it must have been leaking since the spring.”

I remember reviewing a file where a family returned from a two-week vacation to find their kitchen flooded and mold creeping up the cabinets. A supply line had failed while they were away. Because they were shocked by the mold, the homeowner told the intake rep, “This must have been spraying for weeks.” That single sentence derailed their claim for months as it was initially coded as a long-term maintenance issue. They only knew their Date of Discovery, which was the day they walked in the door. The exact duration of the leak was a matter for the adjuster to investigate.

Key Point: As soon as you guess that a leak has been happening for an extended period, the intake representative types that guess into the permanent file. The adjuster will read those notes before they even call you to schedule an inspection. You have effectively diagnosed the problem against your own interests before an expert has even looked at it.

As a best practice to keep your file clean, it helps to mentally separate the Date of Discovery from the Date of Loss. You only know for sure when you found the problem. Stick to that.

“I think my kitchen sink has been dripping for weeks because there is a lot of mold behind the trash can. I guess I just never noticed it until it started smelling.”

“I discovered water damage and mold under my kitchen sink today at 3:00 PM. I have turned off the water valve to stop any active flow.”

The second statement provides the intake system with exactly what it needs: the date and time of discovery, the location, the observable facts, and the immediate mitigation steps taken. It leaves the professional diagnosis of how long the pipe was compromised to the actual inspection process.

Intake Questions You Will Be Asked (And How to Prepare)

Knowing what questions are coming allows you to prepare your notes in advance. When the phone rings, or when you are filling out an online portal form, you will not have to think on your feet. Here are the common intake questions and how to handle them cleanly.

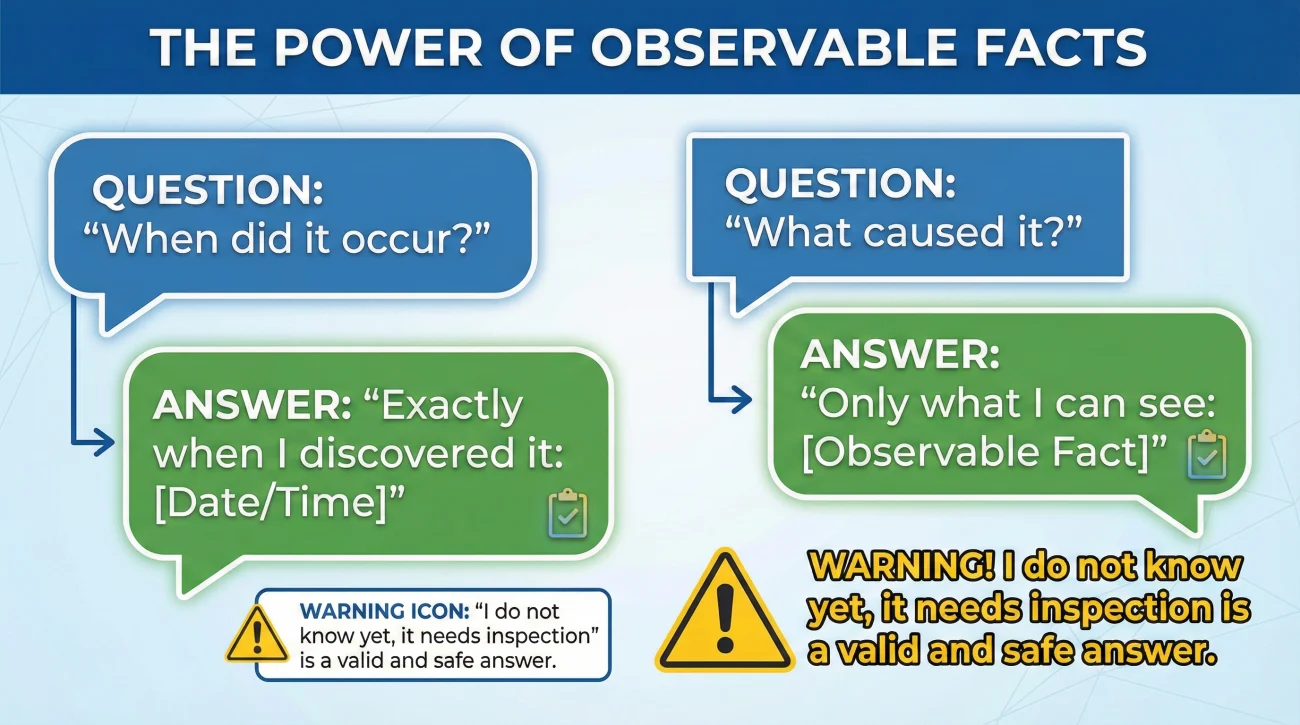

“When did the damage occur?”

Answer with the exact date and time you discovered the damage. If you were away on vacation, provide the date you left and the date you returned to find the damage. Do not provide a guessed timeline.

“Where is the damage located?”

Be specific about the rooms, but keep it factual. “The ceiling in the first-floor guest bathroom and the flooring directly below it.”

“What caused the damage?”

Only state what you can see. If you see a broken pipe, say “a broken pipe.” If you just see a wet ceiling and mold, say “water is coming through the ceiling.” Do not guess that the roof is failing if you have not been on the roof.

“Is the home livable?”

Answer based strictly on basic utilities (water, electricity, heat) and physical safety. Avoid giving medical opinions about air quality on day one.

⚠️ Warning: Intake representatives are trained to fill out required fields in their software. If you do not know the answer to a question, the safest answer is always, “I do not know yet, it will need to be inspected.” It is best to avoid letting a representative pressure you into guessing just so they can check a box on their screen.

Setting Up Your Intake Notes for a Mold Claim

In day-to-day claims operations, the files that move the smoothest are the ones where the homeowner treats the process like a business transaction from the very first minute. You need to write down your facts before you call, and you need to take notes during the call.

Grab a single notebook or open a dedicated digital document. This will become your master timeline. Before you dial the number, write down your observable facts. During the call, you will use a specific formula to ensure you capture the details of the interaction.

[Representative Name] + [Date/Time of Call] + [Claim Number] + [Next Expected Action]

Here is an example of what your notepad should look like after you hang up the phone on day one.

Location: Wall behind the washing machine.

Observable Facts: Drywall is wet to the touch. Baseboards are warped. Dark spots visible on the wall surface. Water line is turned off.Call Log:

October 12, 4:30 PM – Spoke with Sarah (Intake Dept).

Claim Number Assigned: CLM-987654321

Notes: Sarah confirmed FNOL is complete. She stated a field adjuster is estimated to call within 48 hours to schedule an inspection.

By keeping this rigid structure, you prevent your file from becoming scattered. If the adjuster does not call within the estimated timeframe, you have an exact record of who made the commitment and when it was made.

What to Confirm Before Cleaning or Tearing Out Walls

This is where I see the most heartbreaking mistakes. A homeowner finds water damage and mold, panics about the mess, and immediately starts tearing out drywall, ripping up carpet, and throwing the materials into a dumpster. A week later, the adjuster arrives, looks at a bare stud wall, and asks, “Where is the evidence?”

Safety is always your first priority. If materials present a severe health or safety hazard and must be removed, taking comprehensive photographs before touching anything is your best defense. However, whenever safely possible, you have a duty to preserve the scene for inspection. If you casually throw away the source of the leak or the damaged materials, you are destroying the exact proof you need to show that this was a sudden event and not a long-term maintenance failure.

If you need to remove materials to dry the area, it is best to ask a specific question during your intake call, and you need their answer recorded.

“To prevent further damage, I need to remove the wet baseboards and cut away some wet drywall. Do you require me to keep these materials on-site for the adjuster to inspect, or is photographic evidence sufficient?”

💡 Pro Tip: In many cases, the safest route is to take clear, well-lit photos of everything before you touch it, then carefully remove the wet materials and store them in a garage or on a patio under a tarp. Let the adjuster be the one to give you written approval to throw them away.

Communication Hygiene: Getting Requirements in Writing

Once you have reported the claim, your operational focus shifts entirely to communication hygiene. Phone calls are great for moving things forward quickly, but they leave zero paper trail. If a representative tells you on the phone that you are clear to throw away damaged materials, but later an adjuster denies the claim because they could not inspect those materials, you have a major problem.

Always follow up important phone calls with a brief, polite email to confirm what was discussed. This creates a timestamped record that becomes part of your file.

Subject: Claim # [Your Claim Number] – Confirmation of Today’s Call

Hello [Representative Name],

Thank you for taking my call today at [Time] to open my claim.

I am writing to confirm my understanding of our conversation. You advised that a field adjuster will contact me within an estimated 48 hours to schedule an inspection. You also noted that I should take photographs of the wet drywall before removing it to dry the area, and that I should retain the removed materials on my back patio for the adjuster to review.

If any of this is incorrect, or if there is a specific checklist of required documents I need to start gathering, please let me know in writing.

Thank you,

[Your Name]

This script is entirely neutral. It does not threaten anyone, and it does not make demands. It simply locks the verbal instructions into a written format, protecting your timeline and your actions.

The Gray Areas of Mold

Some scenarios are not as obvious as a burst pipe. Things like heavy window condensation, poor bathroom ventilation, a minor drip discovered late, or a pipe hidden deep inside a wall are classic gray areas. It is very tempting to self-diagnose these issues when reporting the claim because you want to sound helpful.

Even in these confusing scenarios, the rule remains exactly the same: report only the observable facts. You might see mold near a window, but unless you are a certified contractor, you do not know if it is from a failed window seal, a roof leak tracking down the wall, or simple humidity. Stick to reporting the date you found the damage and let the official inspection determine the origin.

How to Correct the Record If You Guessed

If you have already called in your claim and realize you accidentally guessed the timeline or offered an unverified theory about how long the leak existed, do not panic. You can still correct the record by sending a polite follow-up email to clarify your intake statement.

Subject: Claim # [Your Claim Number] – Clarification of Intake Statement

Hello,

I am writing to clarify a detail from my initial claim report filed on [Date].

To ensure my file is accurate, I want to confirm that my Date of Discovery for the damage was [Date you found it]. While I may have speculated on the phone about how long the water might have been present, I actually do not know the exact duration or origin of the issue.

I am relying on the adjuster’s professional inspection to determine the facts of the loss. Please add this clarification to my file.

Thank you,

[Your Name]

This simple message puts your correction in writing and officially walks back any accidental guesses, making it much harder for an adjuster to rely on your initial speculation as grounds for a denial.

Final Preparations Before You Dial

Reporting a claim involving mold requires a calm, systematic approach. The moment you discover the issue, take a breath. Grab your notebook, write down the factual time of discovery, turn off the water source, and take extensive photos before you move a single item.

When you make the call, remember that you are simply passing along objective data. Treat the intake representative with professional courtesy, get your claim number, and record the next steps.

If you need a broader view on how to organize the documents and photos you will eventually need to submit once the adjuster is assigned, I highly recommend reviewing our complete proof of loss playbook. Getting your story straight on day one is the most critical step you can take to keep your file moving smoothly and avoid the dreaded long-term leak denial.

❓ FAQ

💧 Is mold ever covered by homeowners insurance?

In many cases, it depends on the source of the water. If the mold is the direct result of a covered “sudden and accidental” event, like a burst pipe, it is often addressed as part of that claim. If it is from long-term neglected maintenance, it is commonly denied.

🛑 Does my policy cover mold from a slow leak?

Often, policies exclude damage resulting from slow, continuous leaks that have occurred over weeks or months. This falls into the maintenance category rather than sudden damage.

📸 Should I take pictures of the mold before cleaning it?

It is highly recommended. Taking clear photos of everything exactly as you found it provides the primary visual evidence of the scene before any mitigation or alteration takes place.

🧽 Can I clean the mold myself before the adjuster comes?

You have a duty to prevent further damage, but cleaning away evidence can harm your claim. Always ask the claims representative for written permission or guidance on what you can clean before the inspection.

📞 What do I say when I call the insurance company about mold?

State only the observable facts: the exact date and time you discovered the damage, the location of the damage, and the steps you took to stop active water flow. Do not guess how long it has been there.

🤔 Will my insurance pay for a mold inspection?

This depends entirely on the adjuster’s initial findings. If they accept the cause of loss as a covered event, they may cover specialized testing, but you should always confirm this in writing before hiring your own inspector.

🗑️ Can I throw away moldy items before they are inspected?

Avoid doing this unless you have explicit written guidance or it poses a severe safety hazard. Throwing away damaged materials destroys evidence. If you must remove items safely, store them on the property until the adjuster reviews them.

💨 Does insurance cover mold from a broken water heater?

If the water heater failed suddenly and accidentally, the resulting water damage and any rapid mold growth are often covered. However, the cost to replace the water heater itself is usually not covered.

🗓️ How long does it take for mold to grow after a leak?

Under the right conditions of moisture and temperature, mold can begin growing quickly, sometimes within a day or two depending on the environment and the materials affected.

📝 What proof do I need for a mold insurance claim?

You need a documented date of discovery, extensive photographs of the unchanged scene, saved damaged materials, and a clear, factual timeline log showing your communications with the insurance company.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.