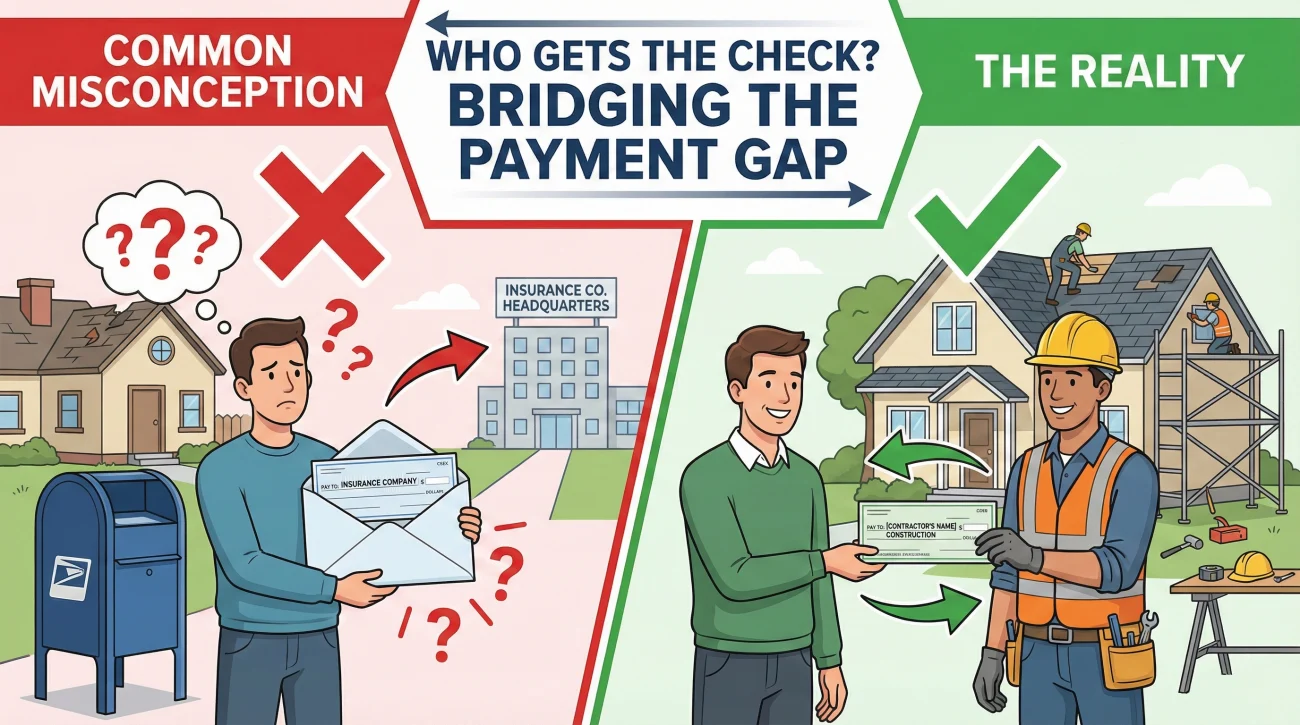

- The most common misunderstanding in property claims is who you pay your deductible to. You do not mail a check to your insurance company; instead, the deductible amount is subtracted from your payout before the check is printed.

- In many claims, your contractor’s final bill will closely align with the insurance estimate total, but your insurance checks will fall short of that total by the exact amount of your deductible. That gap is what you pay directly to the contractor.

- The deductible is typically taken out entirely from your very first payment. This operational rule is why the initial Actual Cash Value (ACV) check often feels surprisingly low.

The Reality of the “Missing” Deductible Check

If I had to pinpoint the single most common billing question that floods into claims departments every day, it is this: “Where do I send my deductible payment?” In my time working in claims operations, I have seen homeowners delay their repairs for weeks, waiting for the insurance company to send them an invoice for their deductible so they can “pay it and get started.”

The confusion is entirely understandable. When you go to the doctor, you hand your copay directly to the receptionist. When you get into a car accident, you often pay your deductible to the auto body shop before they hand over your keys. But property insurance claims operate on a completely different accounting mechanism. The system is designed around subtraction, not collection.

As a property owner, it helps immensely to understand how the claims software actually processes your deductible. They generally do not bill you directly; instead, they net it out in the settlement. They fulfill your deductible obligation by withholding that exact dollar amount from your settlement check. My goal here is to walk you through exactly where that number shows up in the payment flow, how it affects your interaction with your contractor, and how to read your estimate summary so you are never caught off guard by the math.

The Concept Map: How the Payment Flow Actually Works

To understand the deductible, you have to look at the very last page of your insurance estimate. The claims software calculates the cost of every single line item needed to fix your house: the drywall, the paint, the roof shingles, and the nails. It adds all of these up into a grand total. We call this the Replacement Cost Value (RCV) or the gross estimate.

Once the system has that gross number, it begins to subtract. The deductible is the most significant operational subtraction. It is applied globally to the entire claim, not individually to the roof or the kitchen. While carrier and policy setups can vary, the math follows a standardized flow across most platforms.

| The Estimate Summary Concept | What It Means in Practice |

|---|---|

| 1. Gross Estimate Total | The total cost to repair everything (e.g., $20,000). |

| 2. Less Depreciation | The amount held back temporarily for the age/condition of your items. |

| 3. Less Deductible | Your portion of the risk, subtracted permanently from the total payout (e.g., -$2,000). |

| 4. Net Claim / First Check | The actual money printed on the check mailed to you. |

Because the deductible is removed from the total payout, the insurance company considers your obligation “met” the moment they issue that net check. They have paid their portion, and you are now responsible for funding the remaining balance when it is time to pay the contractor.

Why Your Contractor Collects the Deductible

This subtraction method creates a very specific operational gap between what the insurance company pays you and what the contractor will eventually bill you. I often spend time untangling disputes where homeowners feel their contractor is “overcharging” them simply because the contractor is asking for the deductible amount.

Let us look at a practical scenario. Suppose the insurance estimate says your roof replacement costs $15,000, and your deductible is $2,000. Your contractor agrees to do the work based on the insurance estimate price. Many people assume the insurance check will cover the entire contractor bill.

However, the insurance company will only pay you a total of $13,000 over the life of the claim ($15,000 total cost minus your $2,000 deductible). When the contractor finishes the job, they hand you a final invoice for $15,000. You hand over the $13,000 you collected from the insurer, and you reach into your own bank account to pay the remaining $2,000. That $2,000 gap is your deductible.

Your contractor is not charging you an extra fee. They are simply collecting the portion of the repair bill that your policy explicitly stated the insurance company would not cover. Keep in mind that while pricing and scope can differ depending on your specific contractor, the underlying deductible logic stays the same.

The First Check: Why It Often Feels So Low

A frequent pattern I notice in claims operations is the panic that sets in when the first check arrives in the mail. Homeowners often look at the check amount, compare it to the total estimate, and assume a terrible mistake has been made. The culprit is commonly how the claims software applies the deductible to the first payment.

In standard property claims, the deductible is not spread out over multiple payments. The system is programmed to subtract the entire deductible amount from the very first check issued. This is combined with the subtraction for depreciation, which can make the initial Actual Cash Value (ACV) check look surprisingly small.

Key Point: The claims software applies your entire deductible against the first payment. If your initial payout seems lower than you expected, check the summary page of the estimate. You will usually see both depreciation and the full deductible subtracted from that first line item.

For example, if you have a $20,000 total claim, with $5,000 in withheld depreciation and a $2,000 deductible, your first check will be exactly $13,000. The entire $2,000 deductible obligation has now been met. When the work is completed and you recover your depreciation, that final $5,000 check will not have the deductible subtracted from it again. It only happens once.

Percentage Deductibles and the Paperwork Shock

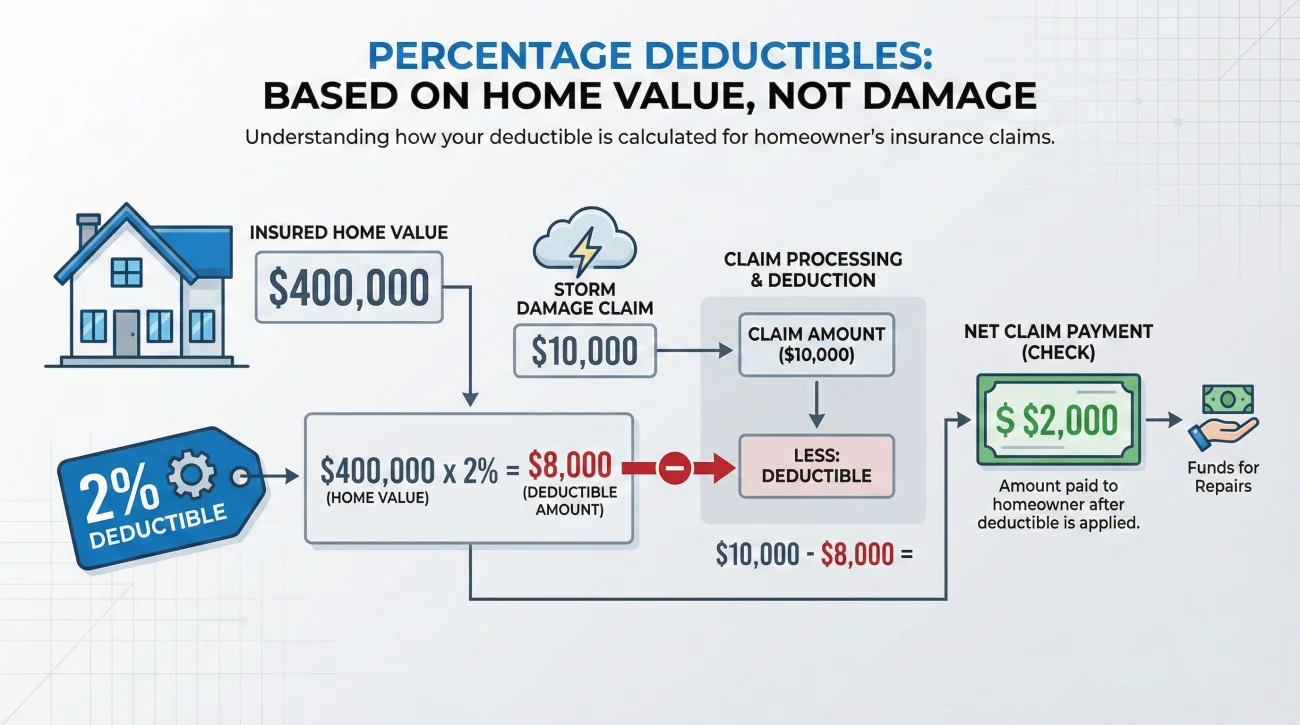

While many people are familiar with flat-rate deductibles (like $1,000 or $2,500), percentage deductibles operate differently on the paperwork and often cause significant confusion. In regions prone to windstorms, hail, or hurricanes, policies frequently carry a 1% or 2% deductible specifically for those weather events.

The operational trap here is that the percentage is not based on the size of the claim; it is based on the total insured value of your home (often referred to as Coverage A). If your home is insured for $400,000, a 2% wind/hail deductible equals $8,000.

When the adjuster writes the estimate, the software automatically pulls that $8,000 figure from your policy data and subtracts it from the gross estimate. If your storm damage totals $10,000, and your percentage deductible calculates to $8,000, your net claim check will only be $2,000. This is a purely mathematical operation within the system, but it is often a harsh reality for property owners to discover by reading the final line of their estimate summary.

⚠️ Note: If you see a strangely high, uneven number listed as the deductible on your estimate summary (e.g., $4,250), it is highly likely you have a percentage deductible tied to your dwelling coverage limit. You can verify this by looking at your declarations page.

When the Deductible Shows Up Twice

There are a few specific scenarios where you might see multiple deductibles applied, which can be highly confusing. The first is when you have multiple occurrences. If a windstorm damages your roof in May, and a separate hail storm breaks your windows in August, these are two distinct events. You will commonly be responsible for two separate deductibles.

The second scenario involves different peril deductibles. You might have a $1,000 “All Other Perils” deductible, but a separate 2% deductible specifically for wind and hail. If the claims software applies the wrong peril code, your subtraction could be drastically higher than expected. Always check your declarations page against the summary line to ensure the correct peril deductible was used.

The Operational Issue with “Waived” Deductibles

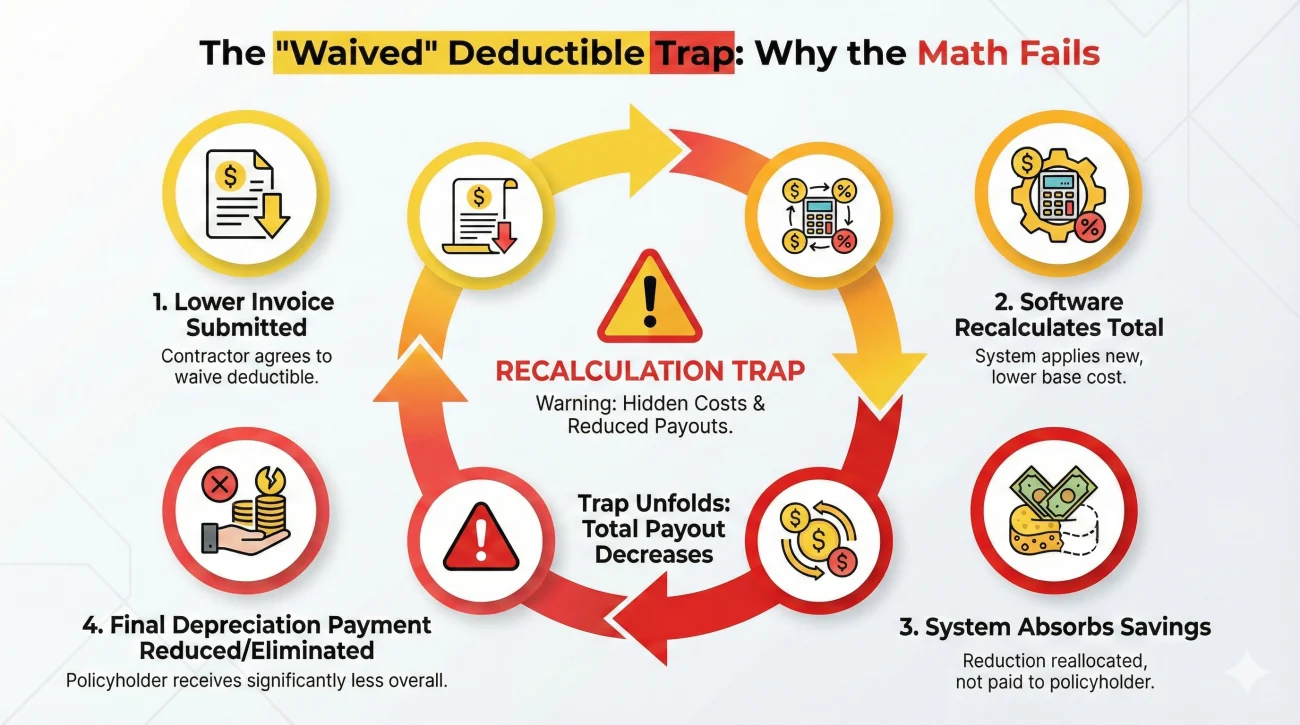

You may encounter contractors who offer to “waive” or “absorb” your deductible. They might say, “We will do the job for what the insurance pays, and you will not have to come out of pocket for the deductible.” Leaving aside any legal or ethical discussions, and keeping in mind that rules vary by state and carrier policies, I want to explain why this practice creates massive administrative headaches within the claims system.

The insurance software is designed to release withheld depreciation only when you prove that you actually incurred the full cost of the repairs. Suppose the gross estimate is $15,000, the deductible is $2,000, and the depreciation is $3,000. The carrier pays you $10,000 upfront. To get the final $3,000, you must submit a final invoice showing the contractor billed you the full $15,000.

If the contractor “waives” the deductible, they typically submit a final invoice to the insurance company for only $13,000. When the claims processor receives an invoice for $13,000, they enter that new, lower number into the software. The system then automatically recalculates the entire claim based on a $13,000 total cost. Because the repair was cheaper than estimated, the system absorbs that savings, applies your $2,000 deductible to the new total, and drastically reduces or eliminates your final depreciation payment.

Operationally, you cannot hide the deductible from the software. If the final invoice is lower than the gross estimate, the system simply adjusts the math, which often results in the homeowner getting significantly less money on the back end.

How Supplements Interact with Your Deductible

A common operational fear is that if the claim value increases, the deductible will be charged again. This is not how the system works. Your deductible is a fixed subtraction applied to the specific event, not a recurring fee for every check.

Let us look at a short case: you use a documentation system to spot low estimates and request a supplement. The desk adjuster approves it and adds $3,000 of new line items to the estimate. The gross total increases. However, the system recognizes that the deductible has already been met on the first check.

Your supplemental check will represent the pure, net cost of the new items ($3,000). You should still see the deductible line item listed on the new paperwork as “applied” or “previously subtracted” to confirm you are not being charged twice.

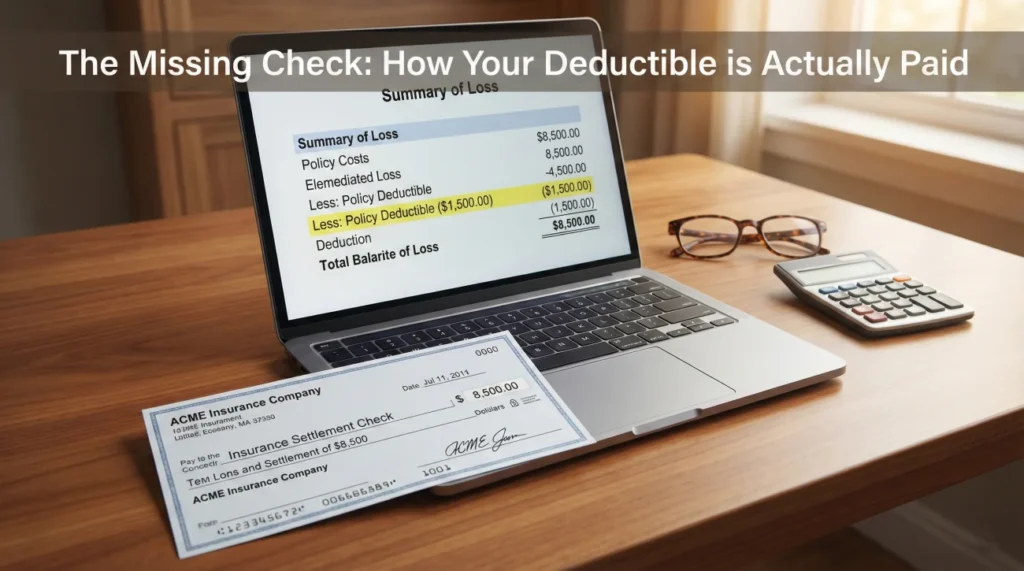

Verifying the Math: Reading the Summary Page

To keep control of your claim finances, you should develop the habit of reading the final summary page of your estimate before you agree to any contractor numbers. This page is the financial blueprint of your claim, and it clearly shows exactly where the deductible was applied.

Look for a section usually titled “Summary of Loss” or “Recap by Category.” It will read like a simple accounting ledger.

Reading the Settlement Summary:

Replacement Cost Value (RCV): $22,500.00 (The total approved cost)

Less Depreciation: -$4,500.00 (Funds held back until work is done)

Actual Cash Value (ACV): $18,000.00 (The current value of the damage)

Less Deductible: -$1,500.00 (Your permanent policy subtraction)

Net Claim Amount: $16,500.00 (The exact amount of your first check)

By reviewing this section, you can quickly confirm two things: first, that the correct deductible amount was applied, and second, exactly how much out-of-pocket money you need to have ready when the contractor finishes the job.

Your 4-Step Deductible Verification Checklist

Before you deposit any check or sign a final contractor invoice, run through this quick operational checklist to protect yourself:

- ✅ Verify the flat amount: Does the subtracted number match your policy documents?

- ✅ Verify the peril: Did they correctly apply the “wind/hail” versus “all other perils” rule?

- ✅ Confirm single subtraction: Was it only taken out of the first check?

- ✅ Save the proof: Take a screenshot or save the PDF of the Estimate Summary page for your records.

Final Thoughts on Managing the Subtraction

Navigating the financial side of a property claim becomes significantly less stressful once you understand that the deductible is a subtraction exercise. The insurance company’s software is designed to withhold that amount right at the beginning of the process.

Expect your first check to be reduced by the full deductible amount, plan to bridge the gap between the insurance payout and the contractor’s invoice with your own funds, and always review the summary page to ensure the math aligns with your policy. Keeping these accounting rules in focus helps prevent frustrating disputes as the claim progresses.

❓ FAQ

💸 Do I pay the deductible before work starts?

You do not pay the insurance company anything. You will pay the deductible amount directly to your contractor, usually as part of the final payment when the work is completed, though some contractors may request a portion of it in their initial deposit.

🏦 Who do I actually write the deductible check to?

You write the check to your chosen contractor or repair company. The deductible is simply the gap between what the insurance company pays you and the total cost of the repair bill.

✂️ Is the deductible taken out of every insurance check?

In most claims systems, no. The entire deductible amount is often subtracted once, entirely from the very first initial claim check. Subsequent checks for depreciation or supplements generally do not have the deductible subtracted again.

📉 What if the repair cost is less than my deductible?

If the gross estimate to fix the damage is lower than your deductible amount, the insurance company will not issue a payment. The system subtracts the deductible from the total, and if the result is zero or negative, the claim is closed without a payout.

📅 Does the deductible apply per year or per claim?

Unlike health insurance which is typically annual, property insurance deductibles commonly apply per claim (per occurrence), though carrier setups can vary. If you have two separate storm events in one year, you will typically be responsible for two separate deductibles.

🤝 Can my contractor just waive the deductible?

Operationally, if a contractor invoices the insurer for a lower amount to “hide” the deductible, the claims software recalculates the entire claim based on that lower invoice. This often results in the insurer reducing your final depreciation payment, leaving you short on funds.

📊 How does a percentage deductible work on the estimate?

The system calculates the percentage (e.g., 2%) based on the total insured value of your home, not the size of the damage. It then subtracts that large flat dollar amount from the repair estimate exactly like a standard deductible.

⛈️ What if I have multiple claims from one major storm?

If the damage (like a roof leak and a broken fence) happened during the exact same weather event and was reported as one occurrence, the system often applies the deductible once. Review the estimate summary to ensure it was not accidentally double-charged.

🛠️ Do I still pay the deductible if I do the work myself?

Yes. The deductible is a mandatory subtraction applied by the claims software before any check is printed, regardless of who actually performs the labor to fix the property.

🔍 Why is my first insurance check so small?

The first check is typically the Actual Cash Value (ACV). To get this number, the software takes the total repair cost, holds back money for depreciation, and then subtracts your full deductible. These two subtractions combined often make the initial check feel surprisingly low.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.