- Do not panic if your first supplement is only partially approved; partial approvals are a completely normal part of the claims operation workflow.

- Stop looking at the bottom line total. You must compare the revised insurance estimate against your contractor’s bid line by line.

- Follow the 30-minute after-revision workflow to isolate a specific “Delta Scope List” of missing items.

- Apply the evidence mapping rule to every missing item: one close-up photo, one justification note, and a specific room location.

- Submit your second request as a one-page delta packet, completely removing any items they have already agreed to pay.

The Frustration of the Partial Win

You did everything right. You noticed that the initial insurance estimate was too low, you worked with your contractor to build a detailed supplement packet, and you submitted it for review. After weeks of waiting, you finally get the email stating your supplement was approved. You open the attached PDF, scroll straight to the bottom line, and your heart sinks. They added more money, but the total is still short of your contractor’s actual bid.

If you find yourself with an insurance supplement approved but still short, your first reaction might be anger. It feels like the insurance company is playing a game of attrition, hoping you will just accept the partial win and pay the remaining difference out of pocket. In my experience working on the operational side of claims, I can tell you that while attrition is a real factor, a partial approval is usually not a malicious denial. It is simply an operational filter.

Desk adjusters process supplements rapidly. They look for the easiest line items to approve first, the ones with obvious photo evidence. If a line item requires complex calculations, needs supervisor authority, or lacks a specific justification note, the adjuster will often just leave it out of the revised estimate to push the file off their immediate task list.

This means the remaining shortage is not necessarily a final rejection. It is often just a “not proven yet” status. My goal with this guide is to show you exactly how to isolate those unproven items, run a second gap check, and build a targeted response that helps close the remaining financial gap.

Key Point: A partial supplement approval is a stepping stone, not a dead end. Your job now is to stop arguing about the total dollar amount and start tracking down the specific missing line items.

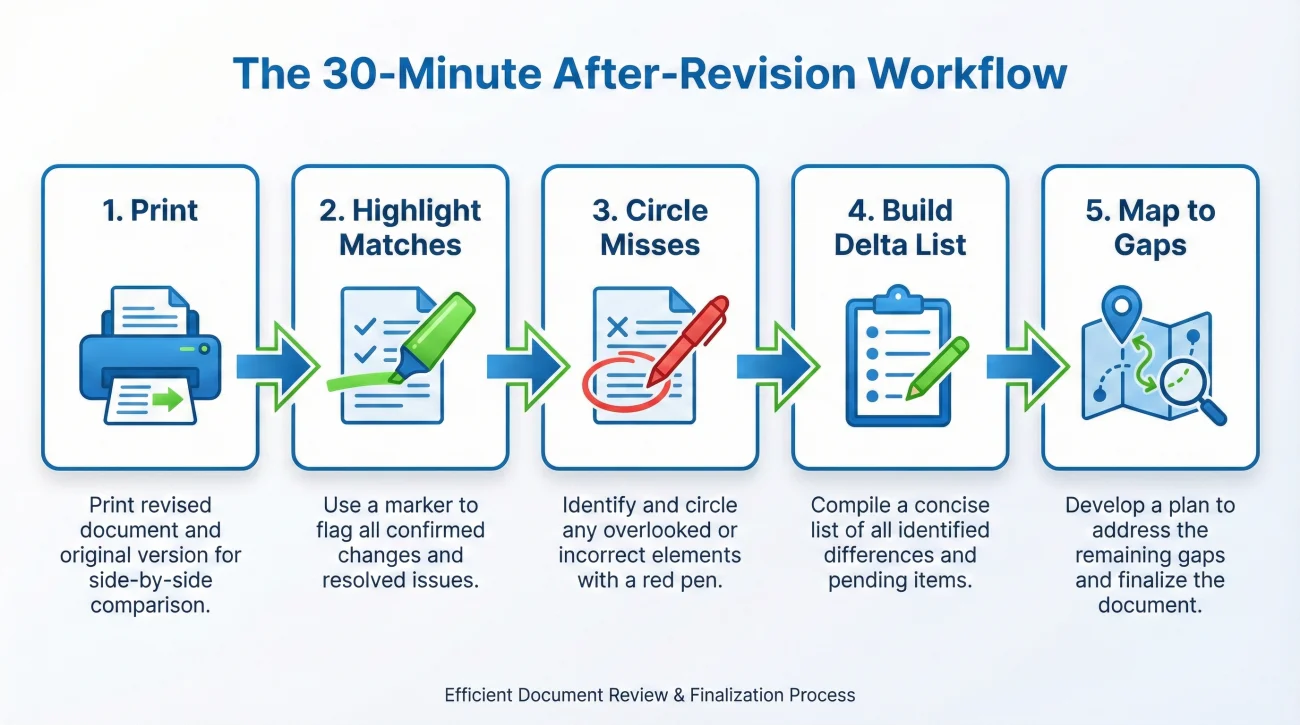

The 30-Minute After-Revision Workflow

When you get a revised estimate back, the biggest mistake you can make is just forwarding it to your contractor with a message that says they still did not pay enough. You have to take ownership of the numbers. I recommend executing a specific 30-minute workflow the moment you receive that PDF to filter out the noise and focus only on the actual points of disagreement.

Clear off your desk and follow these exact steps:

- 📄 Step 1: Print both documents. Print your contractor’s original supplement request and the brand new revised insurance estimate.

- ✅ Step 2: Highlight the matches. Go line by line. If the adjuster added an item with the exact same quantity your contractor requested, highlight it in green on both pages. That item is closed.

- ❌ Step 3: Circle the misses. When you find an item on your contractor’s bid that is missing or short on quantity, circle it in red. Do not try to solve it yet.

- 📝 Step 4: Build the delta list. Extract only the red circled items onto a fresh sheet of paper. This is your official Delta Scope List.

- 🔍 Step 5: Map to the gap buckets. Take each item on your delta list and figure out why it was likely missed using the gap checklist below.

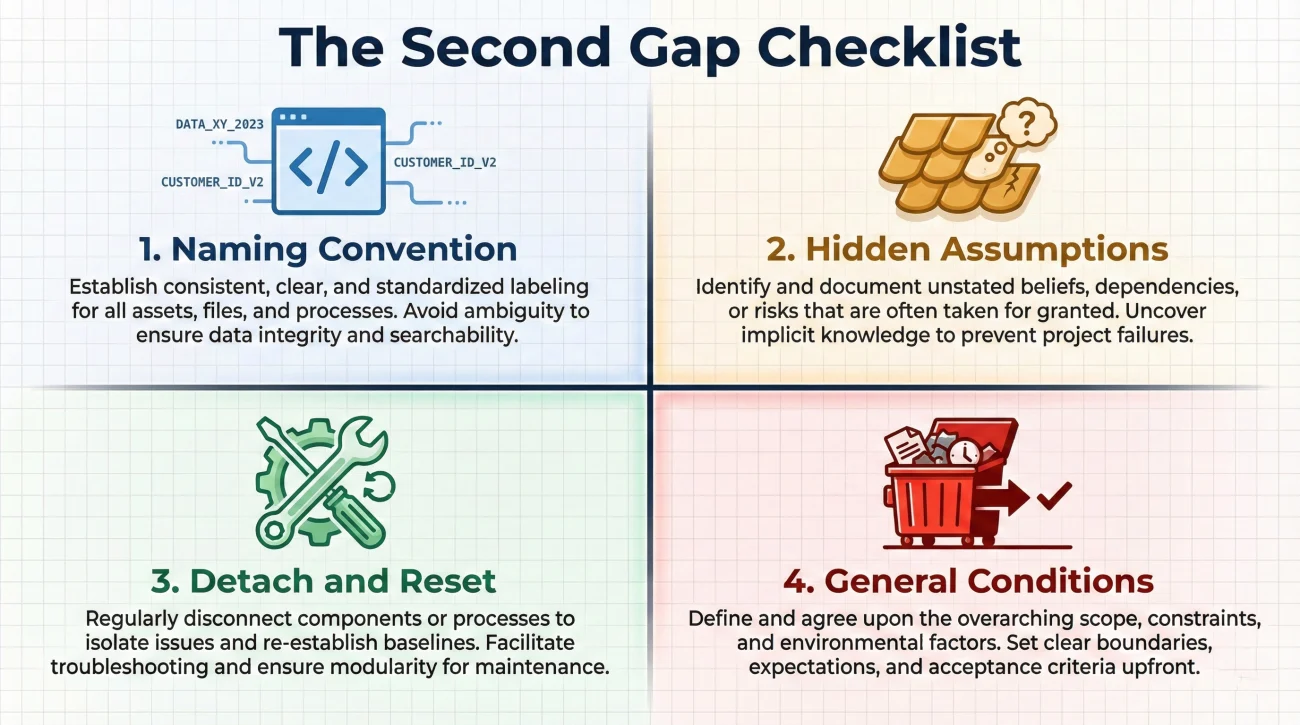

The Second Gap Checklist

Once you have your Delta Scope List, you need to diagnose why those specific items were rejected or ignored during the first supplement review. In claims operations, we see the same types of items fall off estimates repeatedly. They usually fall into four specific operational buckets.

Take your red circled items and run them through this checklist to diagnose the problem.

- 🔍 The Naming Convention Gap: Did the adjuster actually approve the work, but use a different software code? For example, your contractor asked for “Remove and Replace Drywall,” but the adjuster used two separate lines for “Demo Drywall” and “Install Drywall.” Ensure you are not fighting for money they already gave you under a different name.

- 🔍 The Hidden Assumption Gap: Did the adjuster change the grade of the material? Your contractor might have priced “Premium Grade Shingles,” while the adjuster slipped in pricing for “Standard Grade Shingles.” This creates a dollar gap without a missing line item.

- 🔍 The Detach and Reset Gap: Did they approve replacing the damaged siding, but refuse to pay for temporarily removing the exterior light fixtures and gutters to actually do the work? Detach and reset items are commonly rejected because reviewers often incorrectly assume those actions are included in the base labor rate.

- 🔍 The General Conditions Gap: Items like dumpster rentals, protective masking for clean floors, or scaffolding. Reviewers frequently push back on these, asking for explicit photo proof that they were absolutely necessary.

If you systematically map these gaps, you can begin to build a much stronger case. This process integrates directly into the broader Low Estimate Documentation Response framework, giving you a structured way to handle negotiations without relying on emotion.

Field Scenarios: Finding the Missing Scope

Let me show you how this looks in practice with two common scenarios I frequently observe in the field.

The first involves missing hazard pay. I reviewed a file where a homeowner submitted a roofing supplement for $8,000. The revised check was only for $6,500. By running the 30-minute workflow, we found that all materials matched in green. The only red circle was “Additional Labor: Two-Story Steep Roof Pitch.” The adjuster had not rejected the roof; they just missed the steep charge because the original photos were taken from across the street. We took a new photo with a level tool on the roof to prove the pitch angle, submitted just that one item, and it was usually approved within a few days.

The second scenario involves general conditions. I often see claims where a $400 dumpster fee is silently dropped from the revised estimate. The adjuster is not denying that construction debris exists; they simply need concrete proof to release those specific funds. Submitting a clear photo of the actual rented dumpster sitting in the driveway, along with the rental invoice, usually solves this operational gap immediately.

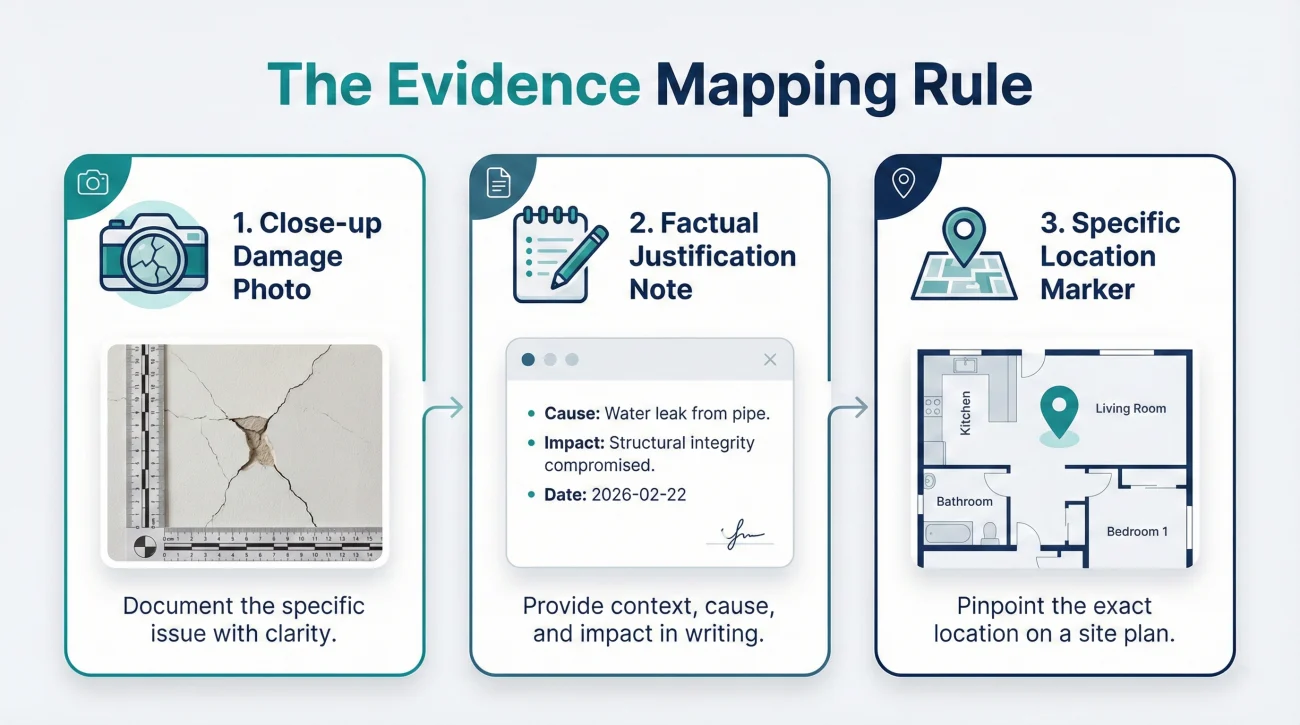

The Evidence Mapping Rule for Round Two

Knowing what is missing is only half the battle. To get those remaining items approved, you have to package the proof so the desk adjuster can process it effortlessly. In round two, you cannot just send a pile of photos and hope the reviewer connects the dots.

You must follow a strict Evidence Mapping Rule. Every single item on your delta list must be accompanied by three specific pieces of data:

- 📸 The Close-Up Photo: Provide a new, clear image that isolates only the disputed item (like the steep pitch, the specific light fixture needing removal, or the dumpster).

- 📝 The Justification Note: Write exactly one factual sentence explaining why the item is required (e.g., “Gutters must be detached and reset to safely access the damaged fascia board”).

- 📍 The Exact Location: Clearly state the room or exterior elevation where the item belongs, matching the structure of the adjuster’s estimate.

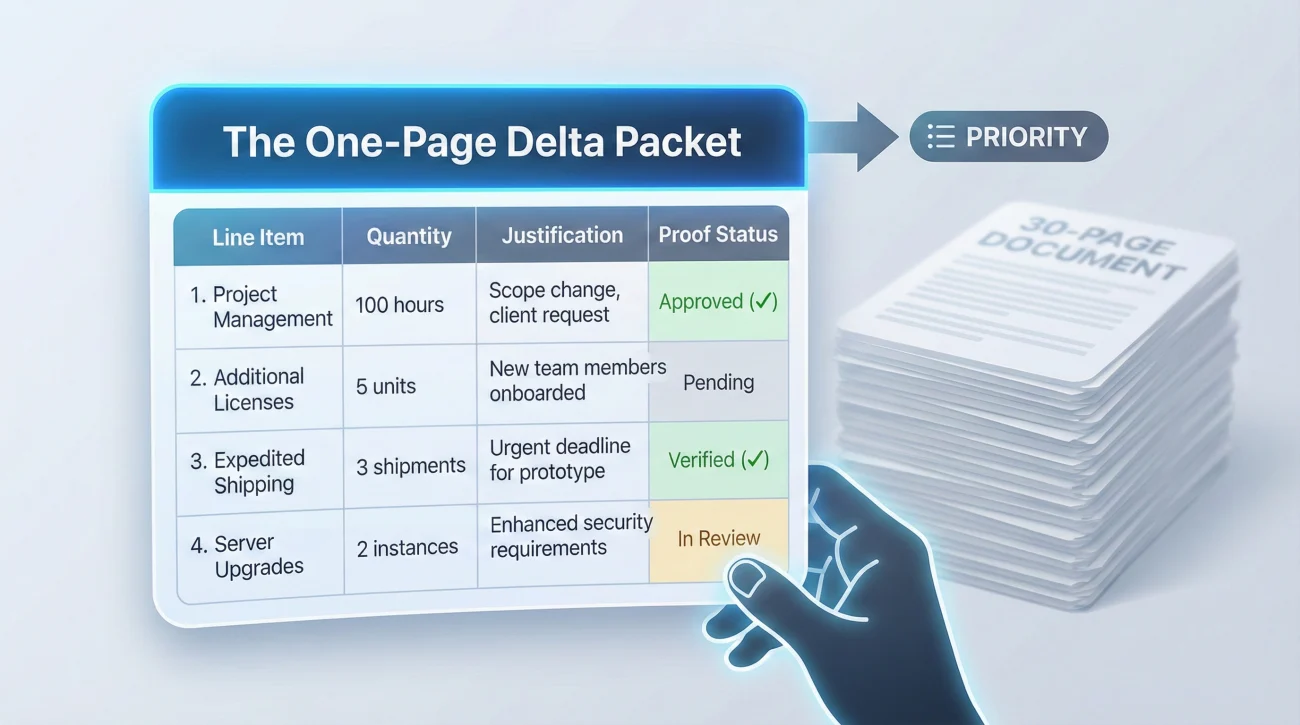

Delta Packet Structure (One-Page Only)

A reviewer’s worst nightmare is being asked to re-read a massive 30-page document they already spent hours reviewing. If you send the whole bid back, they will likely just reply with a standard denial. You must curate the data for them.

I highly recommend structuring your second request as a One-Page Delta Packet. The front page should be a simple table containing only your red circled items. The columns should be: Line Item Name, Quantity, Why It Is Required, and Proof Attached. Behind that single page, include your appendix of mapped photos and receipts.

While specific deadlines, building code requirements, and carrier processes can vary widely by state and policy, the operational principle of submitting a targeted, one-page delta list is a universal best practice. It reduces the reviewer’s cognitive load, which can often improve the chances of a smoother approval.

Common Traps in Round Two

When you are preparing to ask for the remaining money, it is very easy to fall back into bad habits out of frustration. Avoiding unforced errors in this second round is critical.

Sending the exact same contractor bid back to the adjuster, stating “You are still short by $3,000. Please review the whole thing again and pay the remaining balance.”

Sending a one-page Delta Packet that isolates the three specific line items they missed, accompanied by new mapped photos proving why those specific items are required.

How to Request the Second Revision

Communication in this phase requires precision. You have already won a partial victory, so your tone should be cooperative but firm. You are simply pointing out an administrative oversight regarding a few leftover items.

When you email the desk adjuster, you want to acknowledge the progress made, define the remaining gap clearly, and provide the new evidence that justifies closing that gap. You are creating a very narrow, easy path for them to say yes.

Script: The Targeted Delta Request

Use this phrasing to structure your follow-up email. Notice how we do not argue about the total dollar amount; we only discuss the specific missing scope.

Hello [Adjuster Name],

Thank you for processing the revised estimate last week. We have successfully aligned on the majority of the repair scope.

After comparing the revised estimate against the contractor’s requirements, there are [Number] specific line items that appear to have been omitted. To complete the repairs, we still need alignment on these remaining items:

1. [Missing Item Name] – [Brief Reason it is required, e.g., Necessary for safe removal]

2. [Missing Item Name] – [Brief Reason it is required]

I have attached a single PDF containing only the documentation and photos for these specific omitted items, rather than resending the entire bid.

Could you please review this delta list and advise if you need any additional clarification to add these to the scope?

Thank you,

[Your Name]

❓ FAQ

📉 Does accepting a partial supplement mean I agree to their final number?

Usually, no. Accepting a payment for undisputed items does not typically waive your right to pursue the remaining disputed items, unless you sign a document explicitly stating it is a full and final settlement release.

⏳ How long do I have to submit a second supplement request?

There is commonly a deadline set by the policy, often within months to a year. Always confirm this exact date in writing with your adjuster, but it is best practice to submit your revisions within a few weeks to maintain momentum.

📑 Should my contractor just write a new, smaller bid for the missing items?

Yes. Operationally, it is highly effective to have your contractor generate a “Delta Bid” that only includes the missing line items. This prevents the adjuster from having to re-read the original long document.

🧱 What if the remaining shortage is just a difference in material pricing?

If the scope matches but the price is too low, you can support the local market rate with supplier quotes or receipts proving that the material cannot actually be purchased for the price the insurance software suggests.

🏗️ What if the missing item is a building code upgrade?

Code upgrades are frequently left off initial approvals because they require strict proof. Ask your local building department for the written requirement, bulletin, or code section, and submit that document with your delta packet.

📸 Do I need to send new photos for the second review?

Absolutely. If an item was missed, it is usually because the first set of photos did not justify it clearly enough. Always take new, highly specific macro photos focusing only on the disputed delta items.

🏢 Can I demand a supervisor if the second request is denied?

Yes. If you have provided clear, itemized proof of a missing line item and the desk adjuster still refuses to add it without a valid policy reason, escalating to a supervisor for an operational review is a common next step.

🏷️ What if the item is approved under a different code name?

This is the naming convention gap. Before arguing that a scope item was missed, ask the adjuster for their exact line item mapping to confirm they did not already pay for the work under a different terminology.

🛠️ What if the adjuster says an item is ‘included in labor’?

This happens frequently with detach and reset items. Request their estimating software’s line item definition report to verify if those specific actions are actually included in the base yield, or if they require a separate charge.

⚡ What is the fastest way to get a clear answer on a single line item?

Send a single-question email. Instead of a full packet, attach one mapped photo and ask a direct, polite question about that specific missing item. Narrowing the focus makes it much easier for the reviewer to respond quickly.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.