- A partial denial is simply an operational boundary line; it means the carrier is separating the sudden damage they will pay for from the maintenance issue they will not.

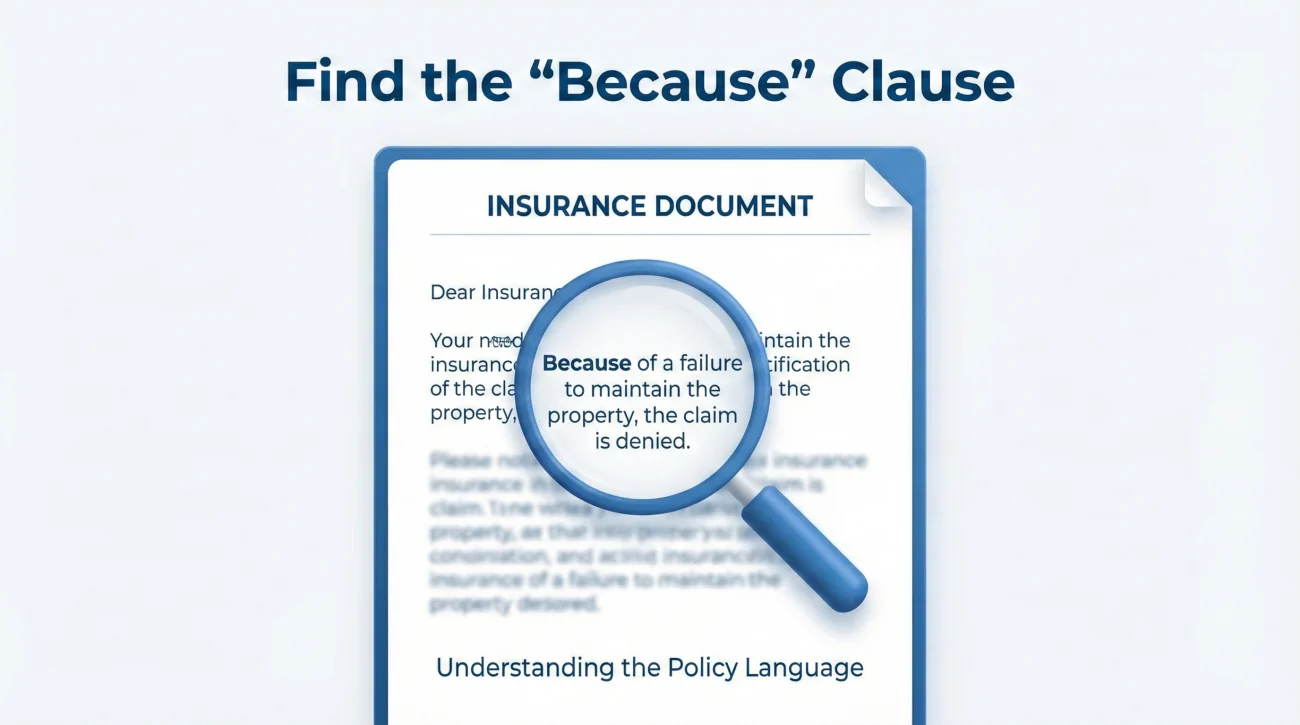

- Stop arguing about fairness and start dissecting the letter to find the exact “Because” clause that triggers the exclusion.

- Respond by asking the adjuster to explicitly map the excluded wording to specific physical areas of your home, so your contractor knows exactly what to dispute.

The Shock of the Split Decision

There is a very specific kind of whiplash you experience when you open a letter from your insurance company and find a check attached to a rejection notice. You read the first page and see they have approved $8,000 for your ruined hardwood floors. You feel a wave of relief. Then, you turn to page two and see bold text stating that the claim for the plumbing pipe itself is “denied.”

In my time working inside claims operations, I audited hundreds of these files. I frequently saw homeowners get so angry at the denial paragraph that they completely derailed the approved portion of their claim. They would call the hotline, threaten to hire lawyers, and refuse to cash the check, assuming the company was trying to trick them.

If you have a partial denial letter sitting on your kitchen table right now, take a deep breath. A partial denial is often just a boundary decision, and it does not mean your policy is worthless. It is a standard operational procedure. The adjuster has simply taken your house and drawn a boundary line down the middle of it. On one side is sudden damage; on the other side is a maintenance failure.

We are going to walk through how to read that letter like a claims professional. I will show you how to find the exact sentence that matters, how to translate the dense policy language, and what operational questions you need to ask to either accept the boundary or challenge it with facts.

Dissecting the Document: Finding the “Because” Clause

Insurance denial letters are written by legal departments, which means they are intentionally dense. They usually start with three paragraphs of generic boilerplate language confirming your policy dates and limits. You can usually skim that part.

You need to scan the document until you find the specific physical description of your property. You are looking for the paragraph where the adjuster stops quoting the policy book and starts describing the actual broken item in your house.

Example of the “Because” Clause:

Once you locate this paragraph, you have found the operational heart of the dispute. The insurance company has stated a physical fact (“severe corrosion”) and applied a policy rule (“wear and tear”). To respond effectively, you must understand the logic behind this specific split.

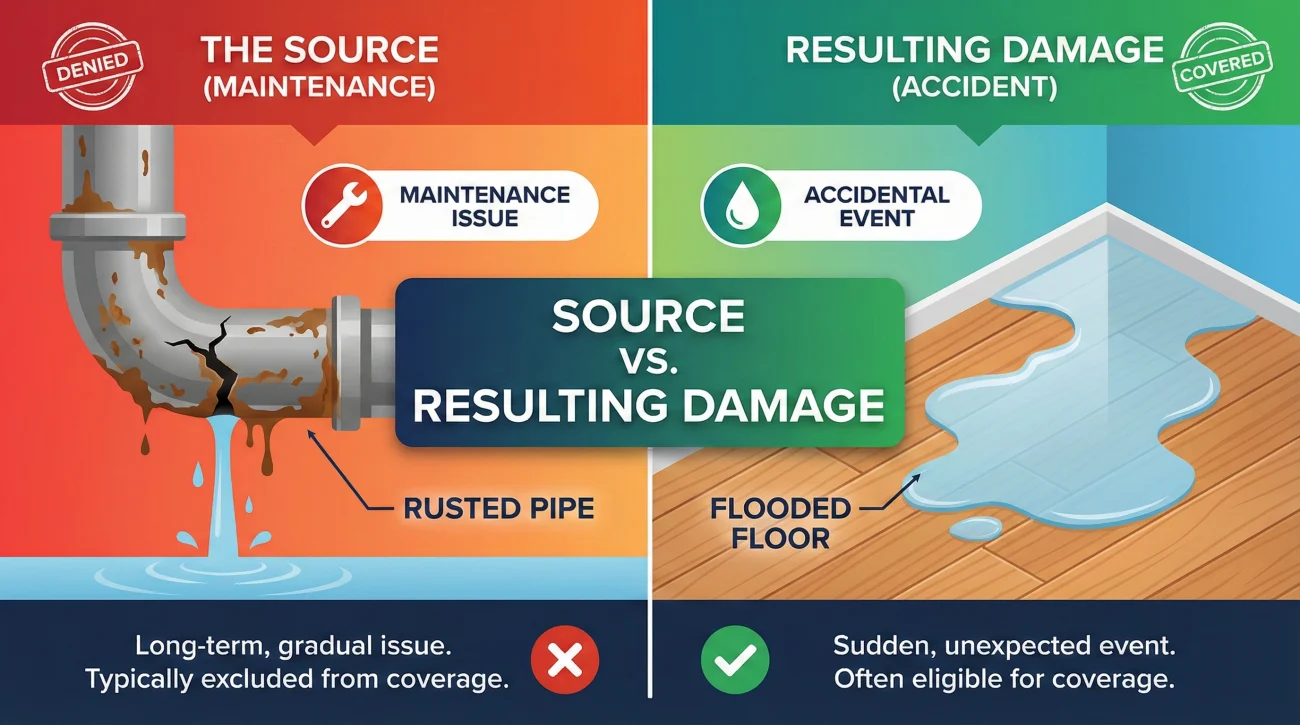

The Golden Rule of Claims: Source vs. Resulting Damage

The vast majority of partial denials fall under one specific operational framework. In the claims world, it is known as the separation of “source” and “resulting damage.”

Homeowners insurance exists to protect you from sudden, catastrophic accidents. It does not exist to replace your appliances when they get old or fix your roof when it naturally reaches the end of its twenty-year lifespan. If the insurance company believes an item failed because you failed to maintain it, they will deny the source.

Key Point: If a washing machine hose degrades over ten years and finally splits, the insurance company will not buy you a new twenty-dollar hose. That is a maintenance failure. But they will pay twenty thousand dollars to replace the flooded living room, because the flood was a sudden accident.

We see this pattern across all types of claims. To make this operational logic easier to visualize, here is how adjusters typically map the boundary between what is denied and what is covered:

| Denied Item (The Source) | Covered Resulting Damage | What Physical Evidence Decides the Line |

|---|---|---|

| Worn roof flashing or aged shingles | Ruined drywall ceiling below the leak | Age of the flashing vs. evidence of recent wind uplift |

| Rusted plumbing pipe or fitting | Flooded hardwood flooring | Gradual corrosion vs. sudden pressure burst |

| Cracked foundation slab | Interior wall shifting | Natural earth movement vs. washout from a broken main line |

When you read your letter, map this rule to your situation. Are they refusing to pay for the original broken item (the source) while paying for the cleanup (the result)? If so, this is a normal structural limit of your policy, not an arbitrary punishment.

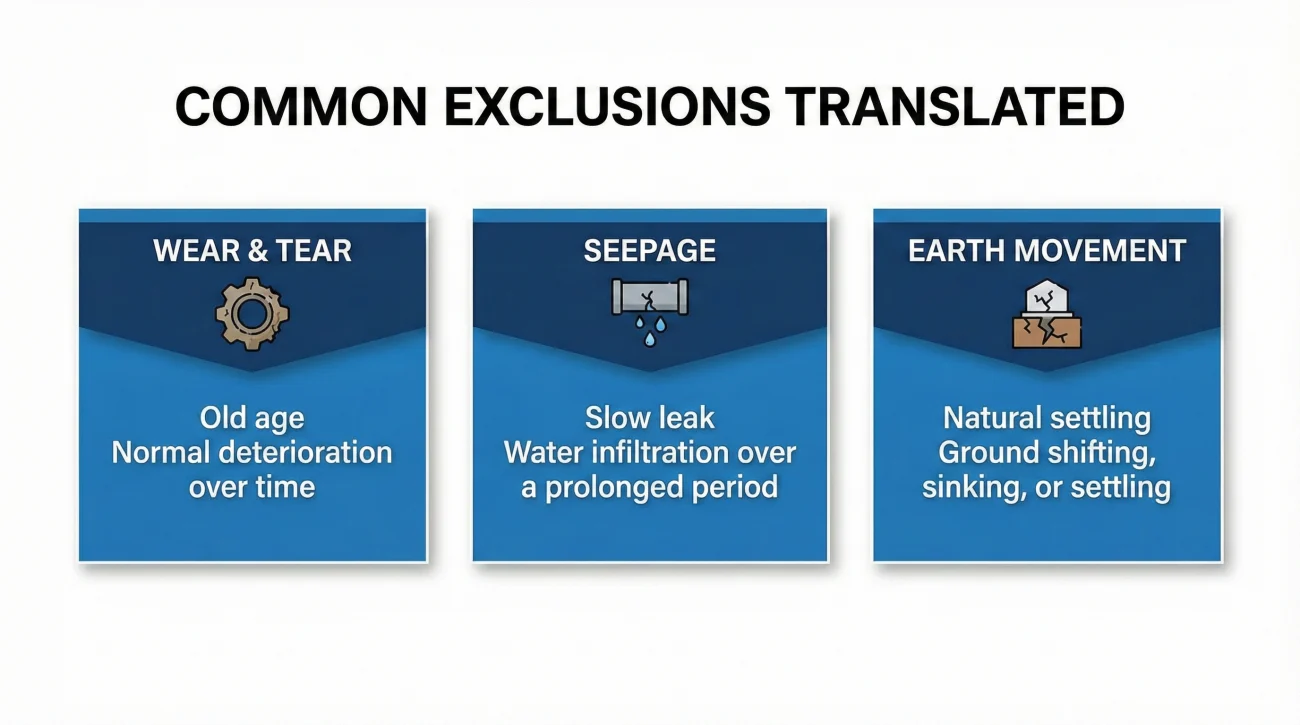

Translating the Three Most Common Exclusions

Adjusters use specific industry codes and phrases to justify where they draw the boundary line. You do not need a law degree to understand them, but you do need to know what physical evidence they are implying when they use these terms. Let us translate the three most common exclusions you will see in a partial denial.

1. “Wear and Tear” or “Deterioration”

When an adjuster cites wear and tear, they are saying the broken item died of old age. Operationally, they looked at photos of the damage and saw rust, brittle rubber, missing shingles, or heavily weathered materials. They are concluding that there was no sudden storm or impact; the material simply gave up.

⚠️ Warning: To fight a “wear and tear” exclusion, you cannot just say the item was fine yesterday. You need a licensed contractor to inspect the break and state in writing that the failure point shows signs of sudden, forced trauma rather than gradual degradation.

2. “Seepage Over a Period of Time”

This exclusion is the nightmare of water claims. If the adjuster cites seepage, they are stating that the leak has been happening for weeks or months. They usually base this on finding black mold, heavy rot in the wood studs, or calcified water stains. The policy boundary here is time. Sudden bursts are covered; slow, ignored leaks are excluded.

However, be aware that a sudden burst can happen near old staining. The presence of an old stain does not automatically invalidate a new, sudden rupture if your contractor can prove the recent event.

3. “Earth Movement”

If you claim foundation damage or cracked walls, you might see this exclusion. The adjuster is arguing that the soil under your house naturally expanded, contracted, or settled over the years, causing the cracks. They are explicitly separating this natural shifting from covered perils like a burst pipe washing out the soil.

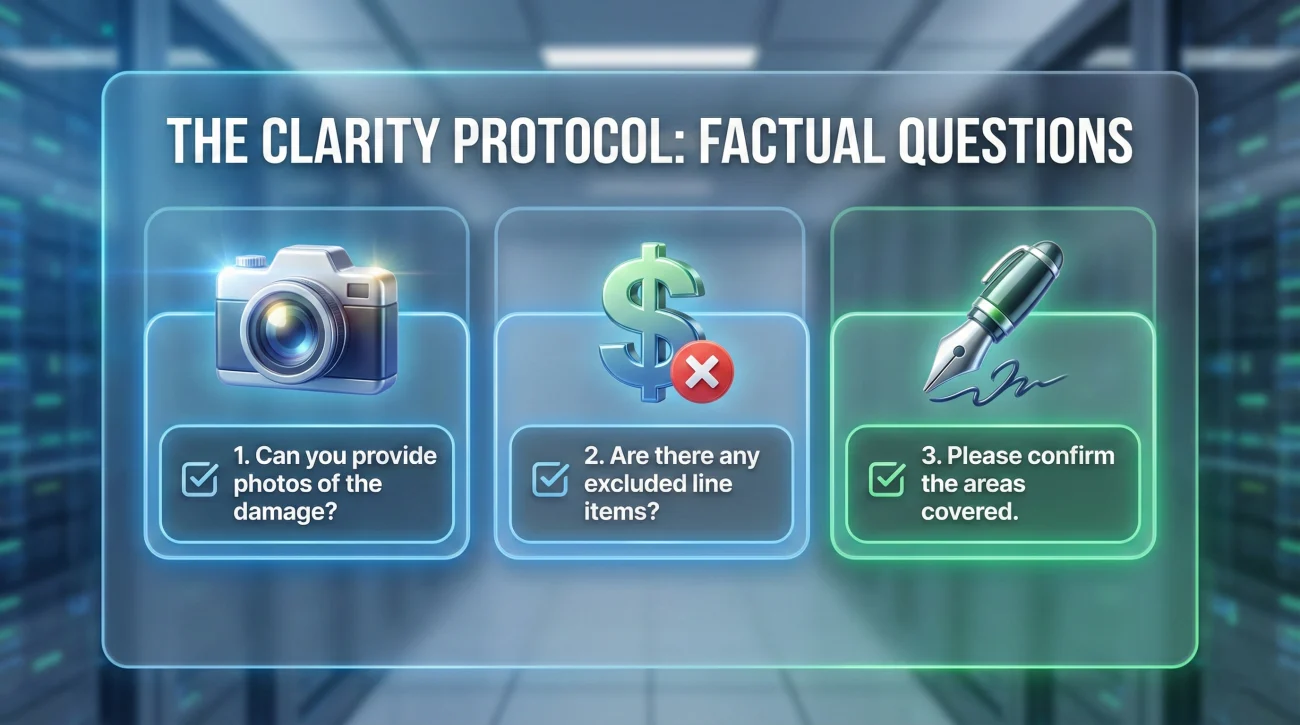

The Clarity Protocol: What to Ask Next

Now that you know how to read the letter, you have to decide what to do next. A common but ineffective response is calling the general hotline to argue about fairness. Fairness is a subjective concept; claims are paid based on objective physical facts.

If you believe the adjuster drew the boundary line in the wrong place, you need to ask factual clarification questions. Your goal is to force the adjuster to clearly state what physical evidence they relied on, so your own contractor can physically examine that exact same spot.

Send a written message through your claim portal containing these specific questions:

- Could you please point out the specific photos from the field inspection that show evidence of gradual deterioration?

- For my contractor’s reference, exactly which line items in the current estimate are excluded under this partial denial?

- Can you confirm in writing that all resulting interior damage remains fully covered, and that only the source repair is excluded?

- If my licensed contractor examines the failure point and finds physical evidence of a sudden rupture rather than long-term wear, what is the exact process to submit that report for a revision review?

💡 Pro Tip: Always ask these questions before you pay a contractor to start tearing out the damaged area.

What to Preserve for Your Dispute

If you are planning to challenge the exclusion, you must preserve the evidence. If the contractor destroys the broken pipe or the damaged roof section, you destroy the physical evidence you need to challenge the adjuster’s conclusion. Make sure you keep:

- 🛑 The broken part itself: The burst pipe, the failed fitting, or the torn flashing.

- 🛑 The surrounding materials: Anything that shows the context of how the break happened.

- 📸 Extensive photography: Clear, well-lit photos taken from multiple angles *before* any demolition or cleanup begins.

Closing the Gap with Your Contractor

Once the adjuster answers your questions, you hand those answers directly to your contractor. If the adjuster says they denied the pipe because of “heavy rust around the fitting,” your plumber now knows exactly what to look at.

If your plumber inspects the fitting and agrees it is rusted out, you must accept the operational reality: you will pay out of pocket to fix the pipe, and the insurance will pay to fix the flooded house. However, if your plumber finds that a sudden pressure spike shattered a perfectly good fitting, you have grounds for a dispute.

Have your contractor document their findings in a formal report with clear, close-up photos. You will then package this report and submit it. If you are unsure how to format this submission so the adjuster actually reads it, review our core guide on building a low estimate documentation response. A clean, fact-based supplement packet is the only operational tool that can reverse a partial denial.

Take the Emotion Out of the Exclusion

A partial denial letter feels like a personal accusation that you failed to maintain your home. It is easy to take offense, but doing so will only slow down the recovery of your property. In the claims system, exclusions are just data points.

Read the letter purely to find the “Because” clause. Identify the exact physical boundary the adjuster drew between the source and the resulting damage. Ask targeted, written questions to clarify their evidence, and then let your contractor inspect that evidence. By treating a partial denial as an information gap rather than a final judgment, you maintain control of the claim and ensure you receive every dollar of coverage you are entitled to.

❓ FAQ

📄 What exactly is a partial claim denial?

It is a formal decision where the insurance carrier agrees to pay for specific portions of your damage while explicitly citing policy language to exclude other portions (often the original cause of the loss).

💧 Why did they pay for the water damage but not the broken pipe?

Insurance covers sudden accidents, not home maintenance. If a pipe degrades over years, the pipe replacement is a maintenance cost (excluded). The sudden flood it caused is the accident (covered).

🔍 Where do I find the real reason for the denial in my letter?

Skip the introductory policy quotes. Look for the paragraph that describes your specific property, usually starting with phrases like “Our inspection found” or “Because the damage resulted from.”

📞 Can I call customer service to get the denial overturned?

Usually not. Customer service representatives generally cannot override an adjuster’s coverage decision. You must present new, contradictory physical evidence from a licensed professional to trigger a secondary review.

🏚️ What does “wear and tear” mean operationally?

It means the adjuster determined the item failed because of age, natural degradation, or lack of upkeep, rather than being broken by a sudden, one-time event like a storm or impact.

⏳ Does a “seepage” exclusion mean my whole claim is void?

Not necessarily. While they may deny the rotten wood that sat wet for months, they might still cover the sudden burst that happened yesterday. You must ask the adjuster to define the exact physical boundary of the seepage exclusion.

🔄 Can I request a reinspection after a partial denial?

Yes. If your contractor’s report provides new physical evidence that contradicts the desk adjuster’s exclusion, submitting that report is often the first step in requesting a formal reinspection of the damages.

👷♂️ How do I prove my damage was a sudden accident?

You hire a licensed professional (like a plumber or roofer) to inspect the exact point of failure. Ask them to write a factual report detailing why the break shows signs of sudden trauma rather than gradual decay.

📝 Should I cash the check if they partially denied my claim?

Cashing the check often does not prevent you from disputing the excluded portion later. However, this depends heavily on the check wording and release language, so ensure it does not say “full and final settlement.”

📸 Can I throw away the broken item after they deny it?

If you plan to dispute it, do not discard it. You must preserve the physical evidence so your own contractor can inspect it to prove the adjuster wrong.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.