- An insurance supplement is a routine operational process, not a penalty. It is simply the formal workflow used to request funds for damage that was hidden or missed during the initial inspection.

- Adjusters and contractors speak different languages. A major cause of delayed supplements is when a contractor submits a standard lump-sum business invoice instead of the line-item format the insurance carrier requires.

- Your role is not to argue technical building codes. Your role is to act as the workflow manager, ensuring both parties have the right documentation and tracking the timeline so the file does not stall.

The Reality of the Supplement Phase

When you receive your first insurance estimate, it is completely normal to feel a wave of panic if the dollar amount looks far lower than what your contractor says the repairs will cost. Many homeowners mistakenly believe this initial estimate is a final, non-negotiable offer. In claims operations, we view the initial estimate very differently. It is simply the starting line.

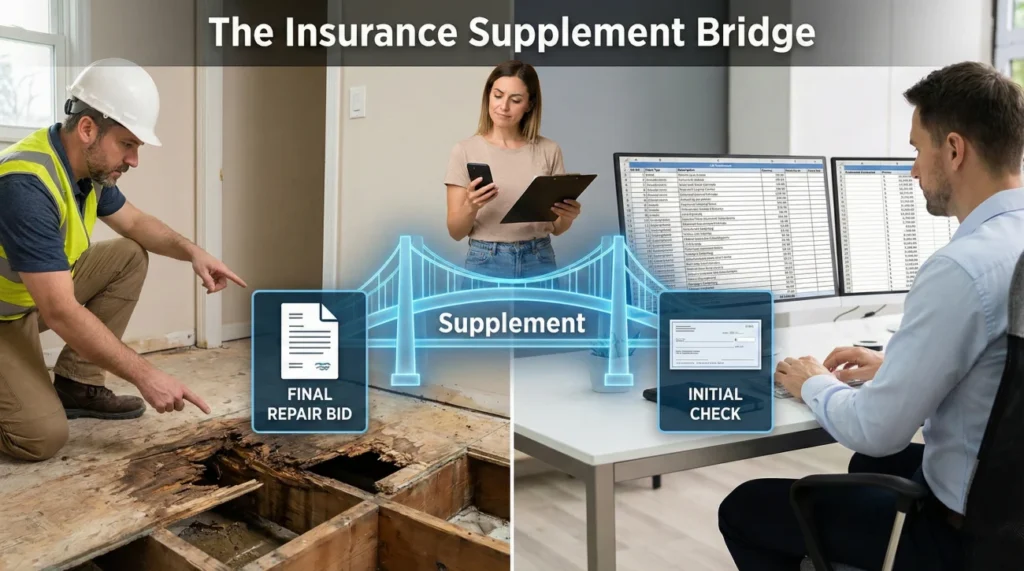

The initial estimate is based only on what the adjuster could physically see and verify on day one. But houses are complex structures. When your contractor actually starts tearing out drywall or pulling up shingles, they inevitably find hidden damage. When this happens, the contractor submits a supplement to bridge the gap between the initial estimate and the reality of the repair.

In my experience reviewing thousands of claim files, the supplement phase is where claims most frequently break down. The breakdown usually does not happen because the insurance company refuses to pay for legitimate damage. It happens because of friction in the process. The contractor sends the wrong type of document, the adjuster pushes it to the bottom of their pile because it is hard to read, and weeks pass with no progress.

Understanding how the contractor submits a supplement request, and what the adjuster actually needs to approve it, is the key to keeping your project funded and moving forward.

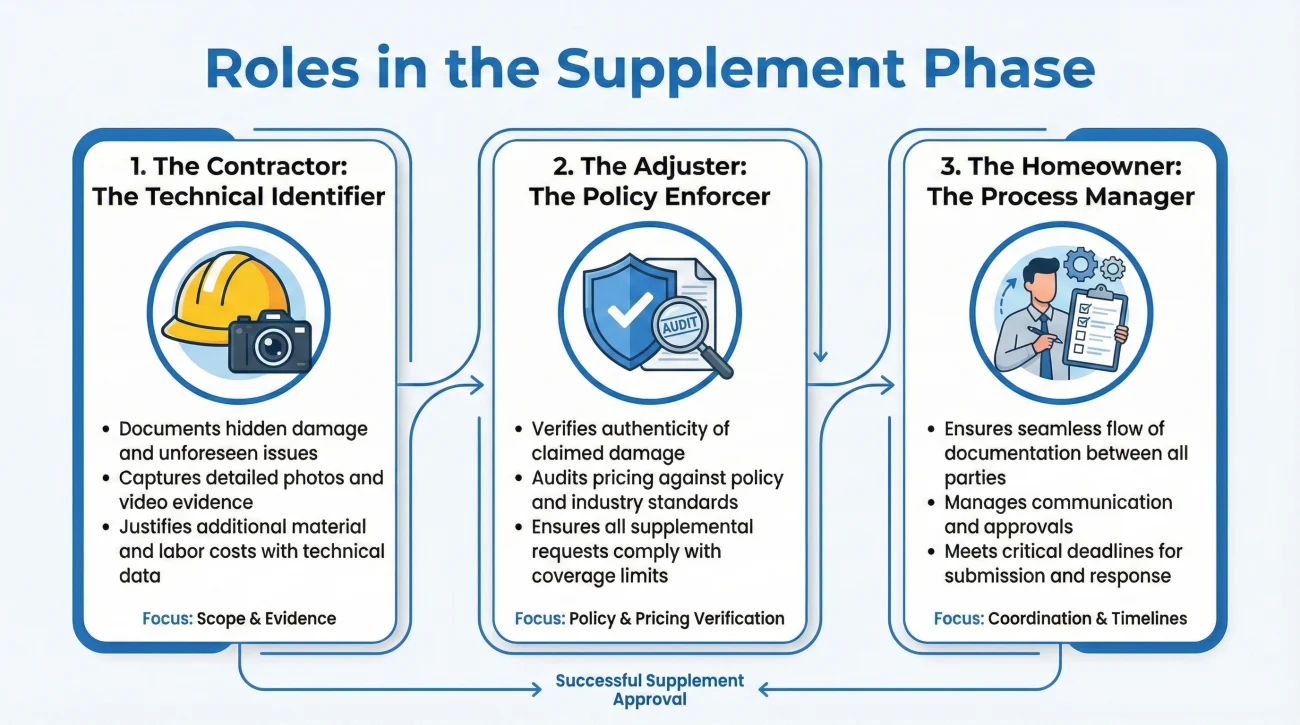

Mapping the Roles: Who Does What

To keep the supplement process clean, you have to understand the operational role each person plays. When these roles blur, files get stuck.

The Contractor: The Technical Identifier

Your contractor is the boots-on-the-ground expert. Their operational job is to identify exactly what is missing from the initial estimate, document it with clear photos before they fix it, and write a detailed request for the additional funds. They must prove that the requested work is physically necessary to restore the property.

The Adjuster: The Policy Enforcer

The desk adjuster is not a construction manager; they are an auditor and a policy enforcer. Their job is to look at the contractor’s request, verify that the damage was caused by the covered event (and not wear and tear), and confirm that the pricing matches the carrier’s approved software models. They need evidence, not opinions.

The Homeowner: The Process Manager

You are the project manager of your own claim. Your job is not to argue with the adjuster about the price of a sheet of plywood. Your job is to connect the contractor and the adjuster, ensure the contractor submits the paperwork in the format the adjuster requires, and follow up relentlessly to ensure deadlines are met.

Estimate vs. Invoice vs. Supplement

Before we look at the format clash, we need to clarify three terms that are constantly confused, causing endless back-and-forth between contractors and carriers.

- 📄 The Estimate: The insurance company’s initial baseline. It details what they believe the repair will cost based on early visible evidence.

- 📄 The Supplement: A line-item request for extra funds based on newly discovered, hidden damage. It is submitted before or during the repair.

- 📄 The Invoice: The contractor’s final billing document showing what was actually charged.

❌ Note: The single fastest way to get your file ignored is to send a paid, lump-sum invoice to your adjuster and call it a “supplement.” Adjusters cannot easily review post-repair invoices if they were never given the chance to review the line-item supplement request beforehand.

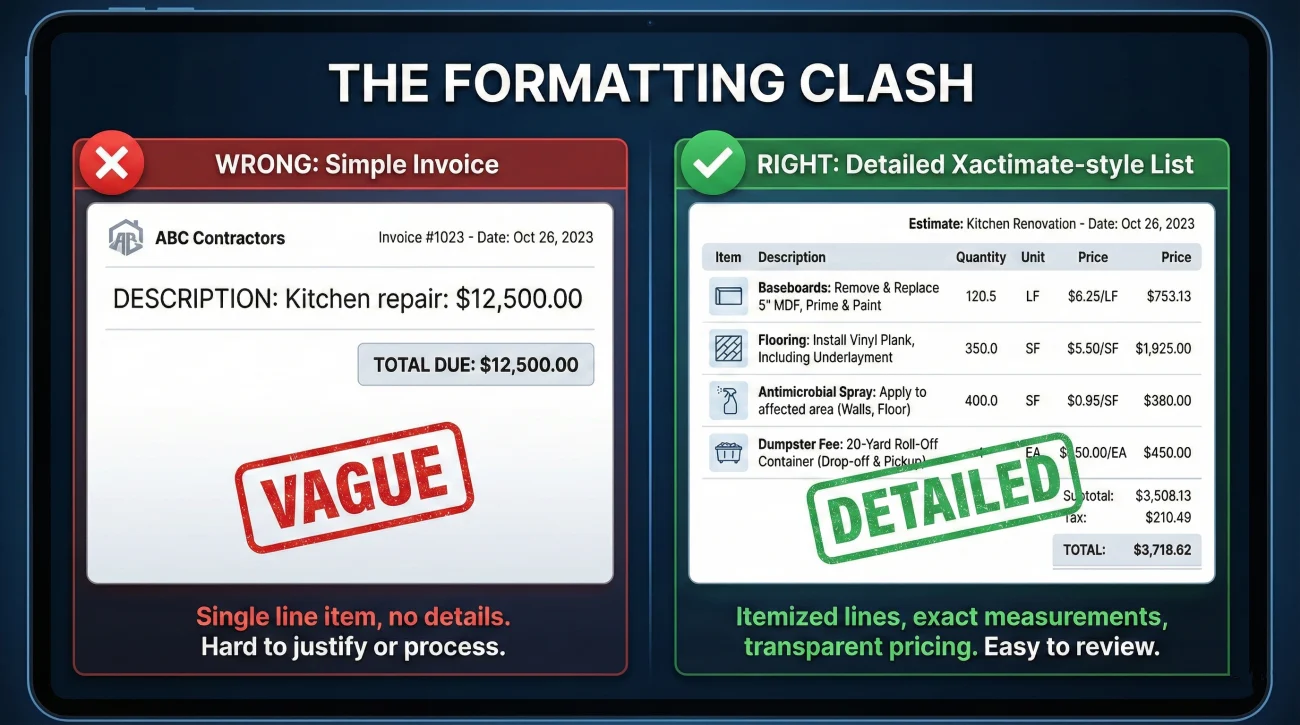

The Formatting Clash That Stalls Claims

If there is one process fact I want to share with you, it is this: adjusters and contractors do not naturally speak the same language.

Let me share a very common field note. A homeowner hires a great local contractor to rebuild their water-damaged kitchen. The contractor realizes the subfloor is rotted and needs to be replaced, which was not on the initial insurance estimate. The contractor writes up a document that says “Kitchen Subfloor Replacement: $3,500” and emails it to the adjuster.

Two weeks later, the adjuster responds with “Supplement denied pending proper documentation.” The homeowner is furious, and the contractor is frustrated.

Why did this happen? Because a single-line lump-sum statement is hard to review inside a claims management system. The adjuster’s software requires them to input exact measurements, material grades, and labor hours. They cannot just type “$3,500” into their system without justifying how they arrived at that number.

“Remove and replace damaged kitchen flooring, including labor and disposal: $4,200.”

“Room: Kitchen.

Tear out baseboards (32 linear feet).

Tear out wet laminate flooring (150 sq ft).

Apply antimicrobial spray to subfloor (150 sq ft).

Replace laminate flooring (150 sq ft).

Dumpster fee for debris.”

The “After” example is written in the itemized format the adjuster needs. When a contractor submits a request using detailed line items, ideally matching the exact software the carrier uses (like Xactimate), the adjuster can quickly copy, paste, and approve. When they submit a lump sum, the file often stalls in the queue.

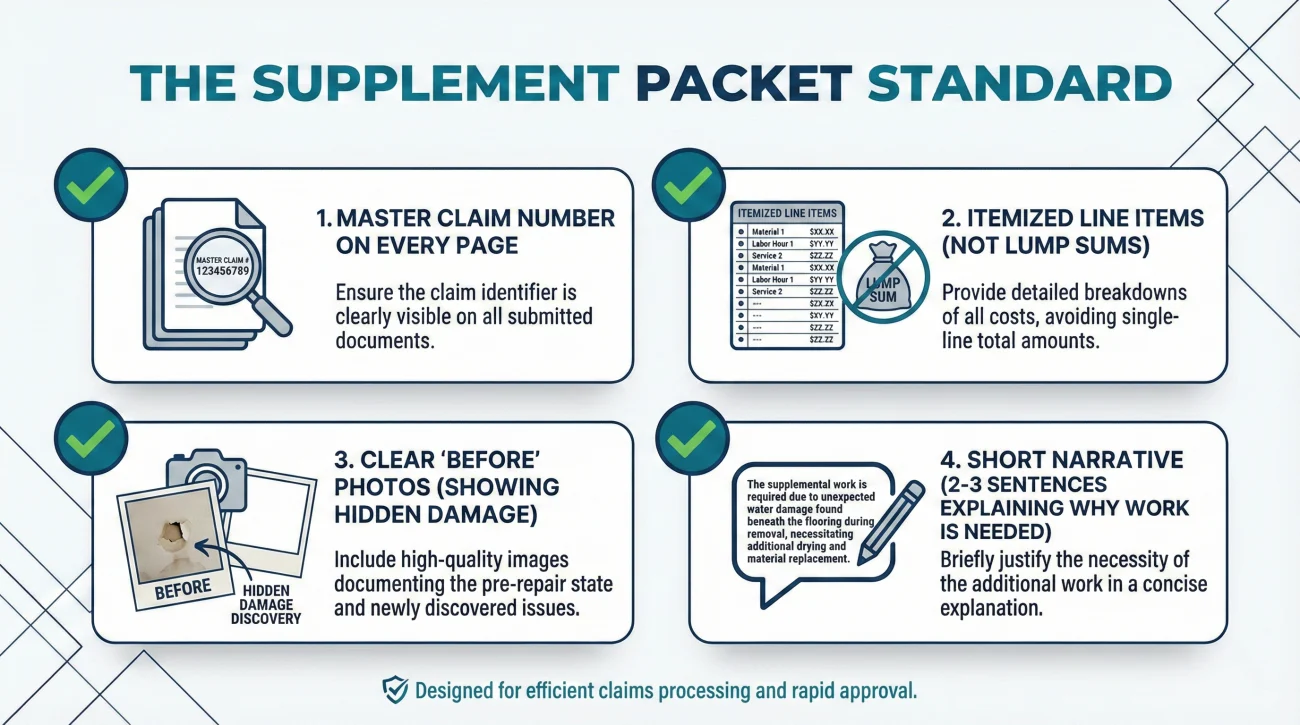

The “One-Page” Supplement Packet Standard

Before your contractor hits send on a request, you should do a quick alignment check. You do not need to understand the math, but you do need to verify the packaging. An incomplete packet usually triggers follow-up requests and unnecessary waiting.

Use this checklist to ensure your contractor’s supplement packet meets the standard required by most carriers.

- ✅ Master Claim Number: Every single page of the supplement, and every subject line in the email, must contain your exact claim number.

- ✅ Itemized Line Items: Verify that the document lists specific tasks, rooms, and quantities, not just “Misc Labor” or large lump sums.

- ✅ Clear “Before” Photos: The golden rule is that if the adjuster cannot see it, they cannot pay for it. The contractor must take photos of the hidden damage before tearing it out. Ideally, these photos are clearly labeled or organized in a named folder.

- ✅ A Short Narrative: A strong supplement includes 2 to 3 sentences explaining why the extra work is needed. For example: “Upon removing the drywall, we discovered the insulation was saturated behind the vapor barrier, requiring immediate removal.”

Managing the Communication Loop

A major operational trap homeowners fall into is playing the middleman. The contractor tells you what they need, you try to translate that technical jargon in an email to the adjuster, the adjuster replies with a policy limitation, and you try to explain that back to the contractor. This telephone game causes predictable back-and-forth and misunderstandings.

Your goal is to connect them directly for technical discussions while keeping yourself firmly in the loop for oversight.

When it is time for the contractor to submit the packet, use this formula to introduce them over email:

[State the purpose] + [Introduce the contractor] + [Establish the communication rule]

Here is a practical, copy-paste safe script to set up this connection cleanly.

Subject: Claim #12345 – Supplement Submission and Contractor Introduction

Hello [Adjuster Name],

I have selected [Contractor Name/Company] to complete the repairs for my property.

They have identified some additional damage that was not on the initial estimate and have prepared a detailed supplement for your review. I have CC’d my project manager, [Contractor Contact Name], on this email. They have attached the itemized supplement and the supporting photos.

Please feel free to communicate directly with [Contractor Contact Name] regarding the technical scope and line items. However, please ensure I am copied on all emails so I can track the progress of the file.

Please let us know if you need any additional photos or information to review this request.

Thank you.

This email is effective because it removes you as the technical bottleneck but maintains your authority as the owner of the record. If you want a deeper dive into exactly how to structure your overall documentation to support these requests, I strongly suggest reviewing our complete system to spot gaps and get paid.

Handling Normal Adjuster Pushback

It is very common for an adjuster to review a supplement and push back on certain items. This is part of the normal negotiation process. You should not view a partial rejection of a supplement as a final denial of your claim.

Typically, pushback falls into two categories.

| Type of Pushback | What It Means | How to Resolve It |

|---|---|---|

| Scope Disagreement | The adjuster agrees the repair is needed, but disagrees on the method. (e.g., Contractor wants to replace the whole floor; adjuster says it can be patched). | The contractor must provide manufacturer specifications or building code documentation proving patching is not viable. Note: Your job is to ask the contractor for this objective proof, not to debate building codes yourself. |

| Pricing Disagreement | The adjuster agrees on the scope of work, but their software says a sheet of drywall costs $15, while your contractor charges $25. | The contractor must provide actual material receipts or subcontractor bids to prove that local market rates exceed the carrier’s software estimates. |

The Supplement Follow-Up Cadence

A supplement does not process itself. Once the contractor submits it, the file often goes into a separate review queue. It might even be handed off from your initial field adjuster to an inside desk adjuster or a specialized supplement team.

Review queues vary by carrier and workload, but if you hear nothing for five business days, you must prompt the system.

Key Point: Never ask an adjuster “How is the supplement going?” That is too vague. You must ask questions that force a definitive answer about ownership and timelines.

To avoid being ignored or acting too aggressively, use this non-intrusive follow-up cadence to track the review:

- 📅 Day 0 (Submission): Contractor submits the full packet and you send the introductory email linking the two parties.

- 📅 Day 3 (Ownership Check): You ask: “Has this supplement been assigned to a specific reviewer yet, and do you have a direct contact number for them?”

- 📅 Day 7 (Missing Items Check): You ask: “Are there any missing photos, forms, or documents delaying the review process?”

- 📅 Day 10 (Target Date Check): You ask: “What is the target completion date for this supplement review?”

This cadence forces them to either confirm they have everything they need, or give you a specific checklist of what is missing so your contractor can provide it immediately.

Final Thoughts: Keeping the File Clean

Navigating an insurance claim is stressful enough without getting caught in a tug-of-war between your contractor and your adjuster. The supplement phase is the critical bridge between the insurance company’s initial desktop numbers and the physical reality of rebuilding your home.

By understanding what the adjuster actually needs to approve a request, keeping your contractor focused on itemized lines rather than lump sums, and managing the communication loop firmly, you prevent the most common administrative hurdles. You do not have to be a construction expert to get a supplement approved. You just need to run a clean, organized, and well-tracked workflow.

❓ FAQ

📝 What exactly is an insurance supplement?

A supplement is a formal request for additional funds added to an existing claim. It is used when a contractor discovers hidden damage, price changes, or code upgrades that were not included in the insurance company’s initial estimate.

👷 Who usually writes the supplement request?

Your hired contractor typically writes the supplement. They are the ones doing the physical work and possess the technical knowledge to document the exact materials, labor hours, and measurements required to fix the hidden damage.

📞 Can my contractor talk directly to my insurance adjuster?

Yes, and it is highly recommended. It is much more efficient for the technical experts to discuss line items directly. You simply need to give the adjuster permission to speak with them while ensuring you are copied on all communications.

⏳ How long does an insurance supplement review usually take?

A clean, well-documented supplement is often reviewed within 5 to 10 business days (though queues vary by carrier and workload). However, if the submission lacks supporting photos, the wait can stretch for weeks.

🛑 What happens if the adjuster denies the contractor’s supplement?

A denial of a supplement item usually means the adjuster needs more proof. The contractor must respond with objective evidence, such as clearer photos of the damage, manufacturer installation guidelines, or local building code requirements.

💰 Do I have to pay the contractor out of pocket if the supplement is pending?

This depends entirely on the contract you signed with your builder. Operationally, you should communicate clearly with your contractor to align payment schedules with the insurance company’s supplement approval timeline to avoid cash flow issues.

📨 Why did my contractor send the supplement to me instead of the insurance company?

Because you are the policyholder. The contractor works for you, not the carrier. It is often best for the contractor to send the supplement to you first so you can review it, and then you officially forward it to the adjuster to maintain control of the file.

💸 Does filing a supplement delay my initial insurance check?

No. The insurance company owes you the undisputed amount of the initial estimate immediately. The supplement is processed as a separate transaction for additional funds later in the project.

💻 Why is the insurance company asking for an Xactimate format?

Xactimate is the industry-standard software used by most adjusters. It breaks repairs down into specific line items and standardized pricing. Adjusters ask for this format because it allows them to review and approve the contractor’s numbers much faster.

🤝 What if the contractor and adjuster completely disagree on a price?

If they hit a wall on standard pricing, the contractor usually needs to provide actual material invoices or subcontractor bids to prove the real-world cost in your specific local market exceeds the software’s default numbers.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.