- Relying on your memory during a lengthy insurance claim is a trap; an insurance claim delay log turns vague frustrations into hard, operational facts.

- A practical log only needs five specific data points: the date, the person you spoke with, the exact action promised, the target deadline, and the actual outcome.

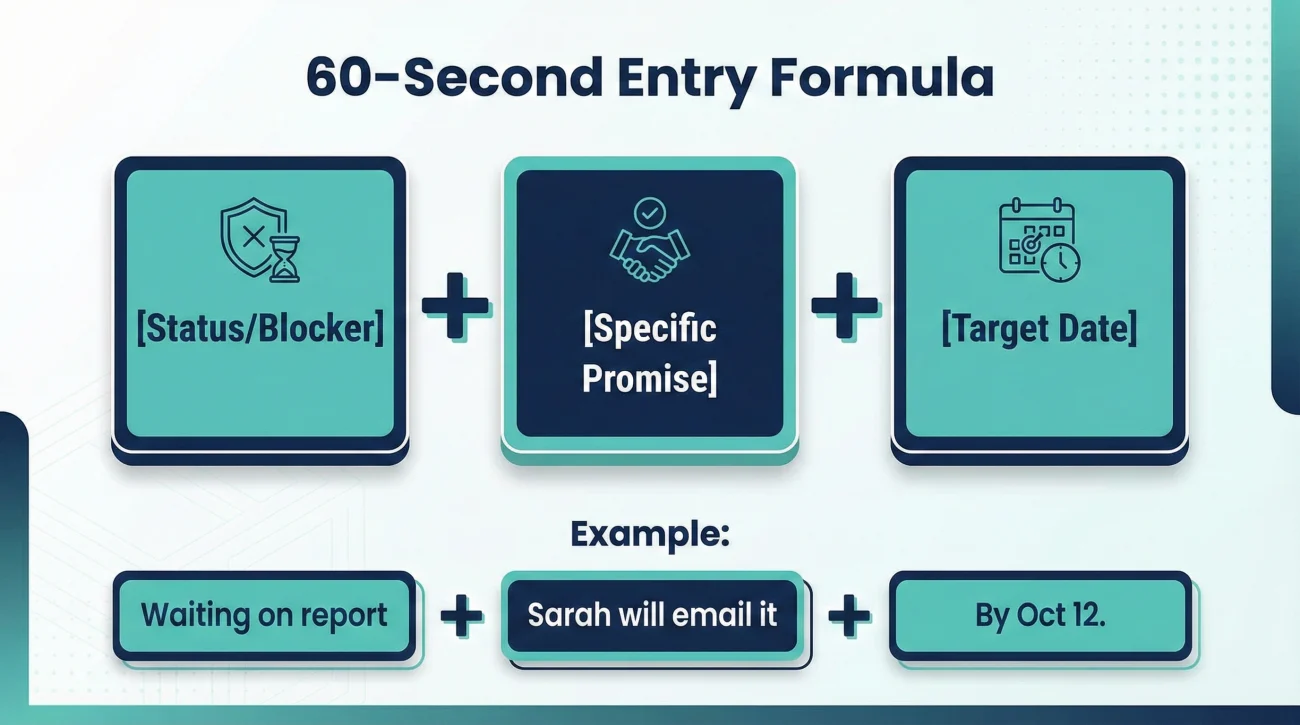

- Keep entries under 60 seconds using a simple formula: Status + Specific Promise + Date.

- Never log emotions or assumptions. Keep the document entirely neutral so it can be used to escalate internal reviews professionally without drama.

- If a promise is made over the phone, it does not truly exist until you log it and send a brief written confirmation to the adjuster.

The Memory Trap in Long Claims

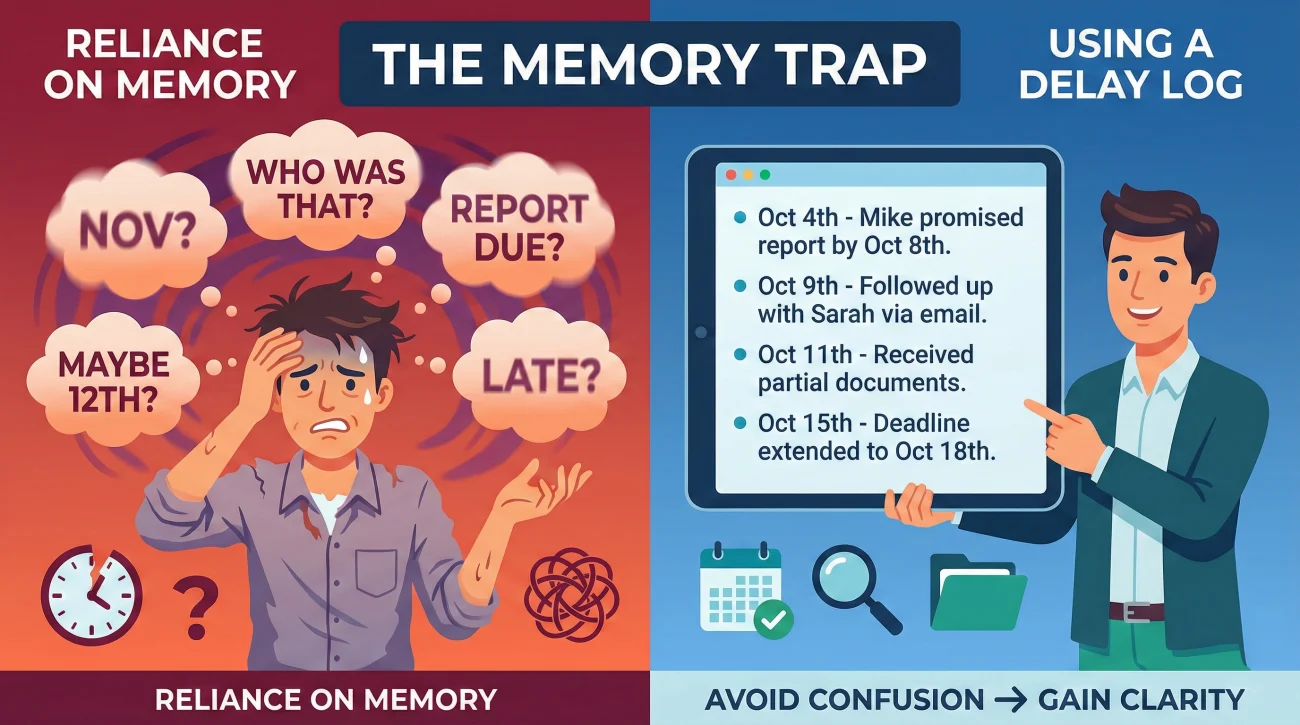

When an insurance claim drags on for weeks or months, the biggest enemy you face is not necessarily the insurance company itself. Often, your biggest enemy is reliance on your own memory. In my experience working through complex documentation processes, I see homeowners fall into the same trap repeatedly. They have a phone call on a Tuesday, the adjuster says an estimate will be ready by Friday, and then Friday comes and goes with silence. By the following Wednesday, the homeowner is frustrated, but the exact details of who promised what, and when, have already started to blur.

This blur is where claims get stuck indefinitely. If you cannot point to a specific missed date and a specific broken promise, it often becomes very difficult to force the process forward. You end up calling the general support line, expressing general frustration, and receiving a general apology. Nothing changes.

This is why building an insurance claim delay log is one of the first habits I encourage anyone to adopt when managing a large loss. You do not need complex software, and you do not need to turn this into a full-time accounting job. You just need a centralized place to record the promises made to you. When you shift from saying, “You guys are taking too long,” to saying, “On October 4th, Desk Adjuster Mike stated the vendor report would be uploaded by October 8th, and it is currently missing,” the entire dynamic changes. You move from being an emotional claimant to an organized project manager.

Relying on memory, leading to vague complaints like “I haven’t heard from anyone in weeks.”

Using a log to state, “It has been nine days since the November 2nd deadline for the field inspection report.”

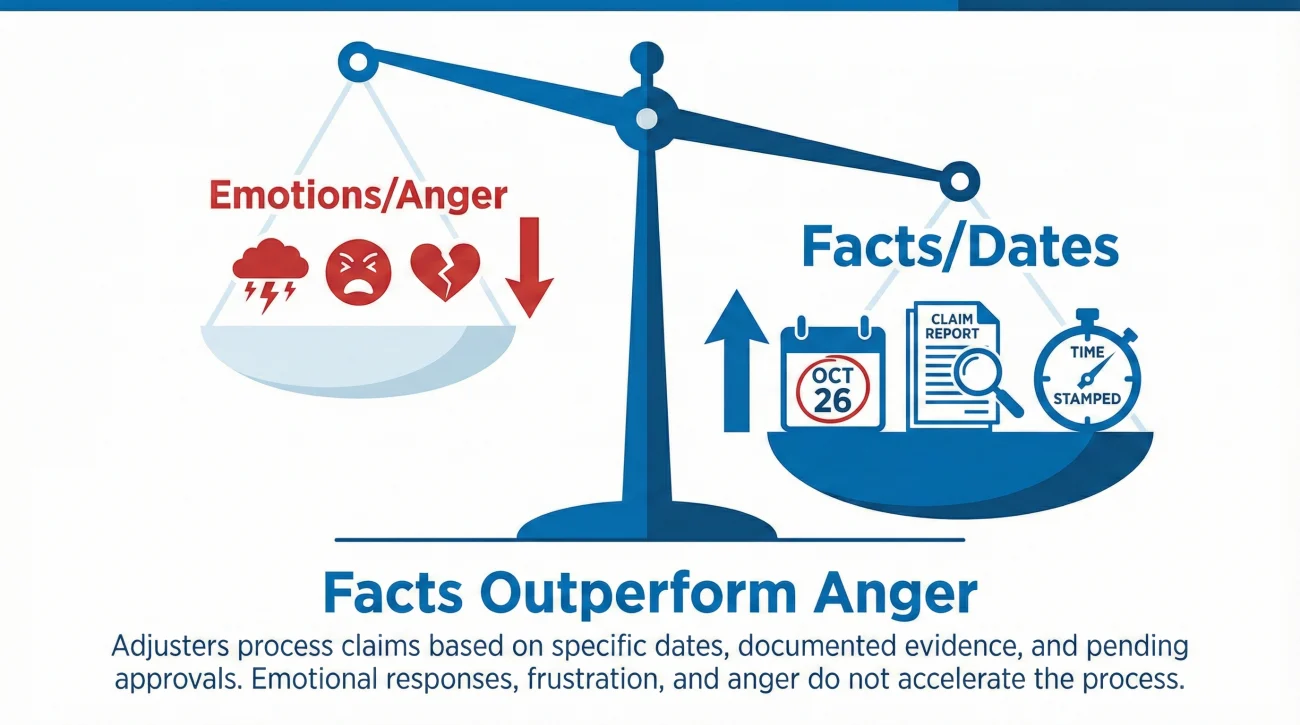

Why a Delay Log Outperforms Anger

It is entirely normal to feel upset when your home is damaged and the repair funds are delayed. However, in the operational reality of processing claims, anger is not a tracking metric. An adjuster sitting at a desk managing a hundred different files cannot process your frustration; they can only process missing documents, pending approvals, and specific dates.

While internal processes, timeline rules, and how adjusters take notes vary heavily from one insurance carrier to another, the core principle of tracking facts, dates, and written confirmations is universally helpful. When I review files where communication has completely broken down, I almost always find a lack of written history. The homeowner feels ignored, and the adjuster’s internal notes simply say “Spoke with insured, answered questions.”

Key Point: An insurance claim delay log is not a weapon to threaten the insurance company. It is an operational tool to keep both you and the adjuster anchored to the same factual timeline.

A delay log bridges that gap. In many files, it creates an external, highly reliable timeline of events. When you call to follow up and speak calmly, referencing specific dates from your log, it signals that you are meticulously organized. Often, just demonstrating that you are tracking every commitment on paper helps keep your file from being pushed to the bottom of the pile.

The 5 Essential Fields of a Claim Delay Log

One of the most common mistakes I see is people overcomplicating their tracking systems. You do not need a twenty-column spreadsheet with color-coded tags. If the system is too complicated, you will stop using it the moment you get busy or stressed. To keep a claim moving, you only need to track five specific pieces of information.

You can create this in a simple notebook, a basic word document, or a standard spreadsheet app. The format matters far less than the consistency of the habit. Here is exactly what you need to record every single time an interaction occurs.

| Date of Contact | Who You Spoke To | The Exact Promise/Action | Target Deadline | Outcome / Next Step |

|---|---|---|---|---|

| Oct 12 | Sarah (Desk Adjuster) | Will request the plumbing report from the 3rd party vendor. | Oct 15 | Missed. Called Oct 16 to follow up. |

| Oct 16 | Sarah (Desk Adjuster) | Escalating vendor request. Promised an update via email. | Oct 18 | Email received Oct 18. Report attached. |

1. Date of Contact

This is straightforward. Log the exact date the communication happened. If you are sending an email late at night, use the date you hit send. This creates the baseline for measuring how long a delay actually is.

2. Who You Spoke To

Never write down “the insurance company.” Insurance companies do not process claims; specific people do. Always ask for the name of the representative, the desk adjuster, or the manager you are speaking with. If they have an extension or an ID number, note that as well. If the file gets transferred, your log will show exactly who dropped the ball during the handoff.

3. The Exact Promise or Action

This is where you must be highly specific. Do not write “talked about the kitchen.” Instead, write “Adjuster stated they need the mitigation invoice to release the next payment.” You need to capture the exact operational block or the exact action they committed to performing.

4. Target Deadline

An action without a date is just a wish. If an adjuster says, “I will review this,” you must ask, “When should I expect to hear back regarding that review?” Log that specific date. This column is the engine of your delay log. It tells you exactly when to trigger your next follow-up.

5. Outcome and Next Step

Leave this column blank until the target deadline arrives. Once the date hits, update it. Did they deliver what they promised? If yes, log it and close that loop. If no, log “Missed deadline” and immediately record the next action you are taking.

The 60-Second Log Entry Formula

If updating your log feels like a chore, you are writing too much. The goal is rapid, factual documentation. To keep yourself from writing paragraphs, use a strict micro-framework for the “Promise/Action” column.

[Current Status / Blocker] + [Specific Action Promised] + [Target Date]

For example, I frequently see third-party vendor reports get stuck simply because the request was never formally sent out by the adjuster. A homeowner might write a vague note like, “Sarah is looking into the plumbing report.” That is not actionable. Instead, apply the 60-second formula.

- ✅ Status: Waiting on plumbing report.

- ✅ Promise: Sarah will officially request it today and email it to me.

- ✅ Date: By Thursday, Oct 12.

Your log entry simply becomes: “Waiting on plumbing report. Sarah promised to request it today and email it to me by Oct 12.” It is fast, highly specific, and gives you a clear trigger for your next follow-up.

Capturing the “Invisible” Phone Promises

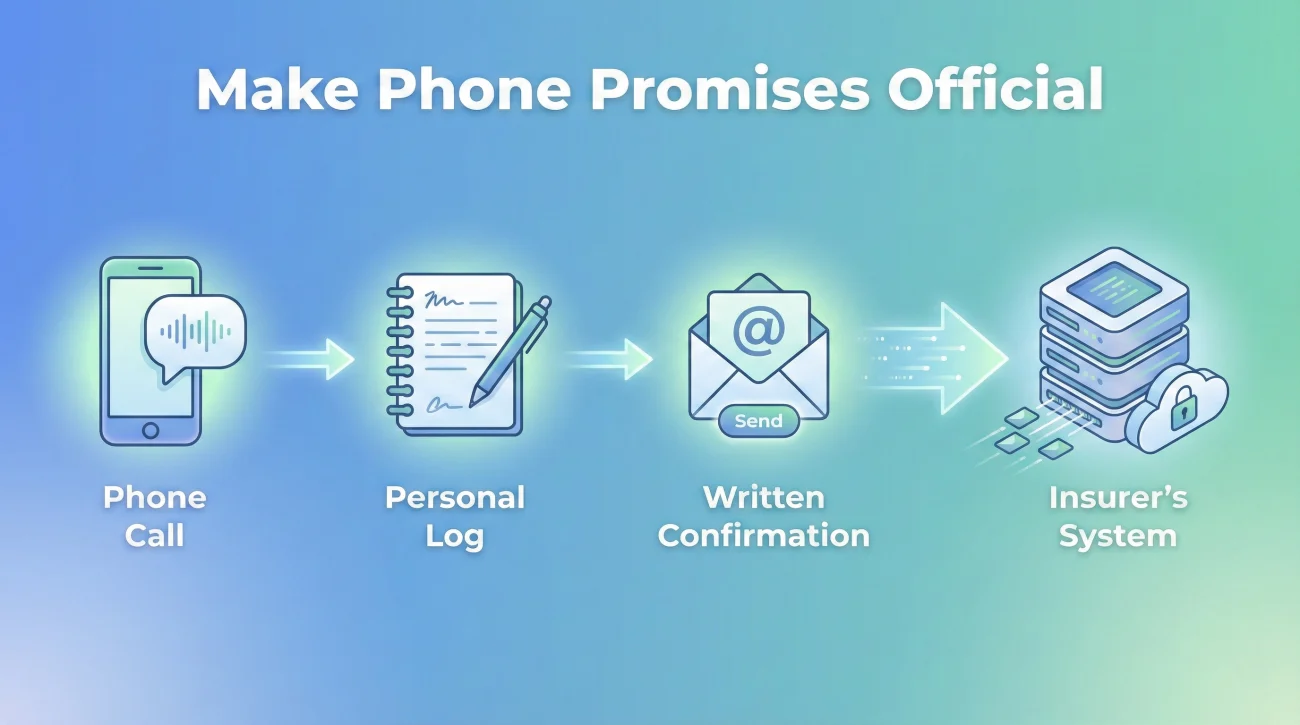

In the day-to-day reality of claims operations, the vast majority of delays originate from phone calls. A phone call feels productive because you spoke to a human being, but from a documentation standpoint, a phone call is invisible. If a promise is made over the phone and not written down, it effectively never happened.

I cannot stress this enough: your personal delay log is only half the battle. If you log a target date in your notebook, but the insurance company has no record of that date, you are tracking a ghost. You must force the phone promise into the written record.

Here is a typical scenario I see. A homeowner calls their adjuster to ask why the estimate is taking so long. The adjuster says, “I am waiting on my manager to sign off, I should have it to you by Thursday.” The homeowner hangs up, feeling relieved, and writes “Thursday” in their log. Thursday passes, Friday passes. The homeowner calls back next Monday, gets a different representative, and is told, “I don’t see any notes here about a Thursday deadline, it’s still pending review.”

To prevent this, every time you log a phone conversation, you must immediately send a brief email to confirm the entry. This aligns your personal delay log with their internal file.

💡 Pro Tip: Treat your delay log as your personal draft, and use email as the tool to publish those facts to the insurer.

Here is a safe, neutral way to document a phone promise right after you hang up:

Subject: Claim #1234567 – Confirming Next Steps from Today’s Call

Hello [Adjuster Name],

Thank you for taking the time to speak with me today.

I am writing to confirm my understanding of our conversation. You noted that the estimate is currently pending management review, and you stated that I should expect an update or the final document by this Thursday, [Insert Date].

If I have misunderstood the timeline or if you need any additional documents from me before Thursday, please let me know in writing.

Thank you,

[Your Name]

By sending this, you have taken the data from your log and injected it into their system. If Thursday is missed, your next follow-up is not based on your memory; it is based on the written email they received.

The Handoff Rule (When Your File Gets Reassigned)

Claims change hands frequently. An adjuster might go on leave, get promoted, or simply be reassigned to a different disaster zone. When a file is transferred, the most common outcome is a complete timeline reset. The new adjuster starts from scratch, and the promises made by the old adjuster disappear into the void.

When you are notified of a reassignment, your delay log becomes your continuity plan. You must immediately document the date of the transfer, the name of the outgoing adjuster, and the name of the incoming adjuster. Then, you proactively send a “recap timeline” email to the new handler so that old promises do not reset to zero.

Subject: Claim #1234567 – File Transfer and Pending Items Timeline

Hello [New Adjuster Name],

I understand you are taking over this file from [Old Adjuster Name]. To help ensure a smooth transition, I want to briefly recap the immediate pending items based on our established timeline.

Prior to the transfer, [Old Adjuster Name] confirmed on [Date] that the structural engineering report was complete and promised the final estimate would be uploaded by [Target Date].

Could you please review the file and confirm if we are still on track for that date? If you need anything else from me to get caught up, please let me know.

Thank you,

[Your Name]

This simple email bridges the gap and ensures the new adjuster is immediately aware of the operational deadlines that are already in motion.

The “Update Rule”: When to Actually Log an Entry

Consistency is what makes this tool powerful. If you only log events when you are upset, your log will be full of gaps. You must establish a strict personal rule for updating it. I recommend the “Touch It, Log It” rule. Every single time you touch the claim, you open the log and add a row.

Log it when:

- ✅ You leave a voicemail requesting a status update.

- ✅ You upload a requested contractor invoice to the portal.

- ✅ An inspector visits the property (log the date, name, and what they said happens next).

- ✅ The adjuster emails asking for a clarification.

A common mistake I see is logging emotions or assumptions instead of facts. Do not write, “Adjuster was rude and is stalling on purpose.” That statement cannot be proven and does not help you move the file forward. Instead, write, “Adjuster ended call without providing a target date for the estimate. Sent email requesting a firm timeline.” Stick to the operational mechanics.

❌ Note: Never use the delay log as a diary. If you eventually need to escalate your claim to a supervisor, you want to be able to hand them a clean, factual timeline, not a list of personal grievances.

Escalation Without Drama

A log sitting quietly on your computer does not speed up a claim by itself. Its value comes from how you use it to trigger action. When you track dates meticulously, patterns begin to emerge. You will quickly see if a file is moving normally or if it is legitimately stuck in an operational bottleneck.

Once your log shows two or three consecutive missed deadlines for the same item, it is time to change your approach. You can transition from simple logging to a more structured claim follow-up system. Instead of expressing general frustration, you use the data to escalate the issue cleanly and professionally.

Here is a neutral, three-sentence framework to escalate a stalled file without causing unnecessary drama:

If the adjuster cannot answer that question, your log gives you the credibility to ask for a manager. You are not escalating because you are impatient; you are escalating because the recorded operational timeline shows a breakdown in the process.

⚠️ Warning: Avoid the temptation to send the entire log to the adjuster as a way to say “look how bad you are doing.” Keep the log for your own tracking, and only pull specific, relevant dates from it when constructing your follow-up messages.

Organizing Proof Over Frustration

Navigating a property claim requires a shift in mindset. You must stop hoping the process will manage itself and start managing the timeline actively. An insurance claim delay log is the simplest, most effective way to take control of the pace of your file.

By writing down the dates, the names, the promises, and the deadlines, you protect yourself against the silent delays that drag claims out for months. You remove the confusion of “he said, she said,” and replace it with a clear, organized paper trail. It takes discipline to log every interaction, but that discipline is exactly what keeps your claim from falling off the radar. Stay factual, stay organized, and let the timeline do the heavy lifting.

❓ FAQ

🗓️ How do I keep track of my insurance claim delays?

The most effective method is maintaining a simple, five-column log that records the date of contact, the representative’s name, the exact action promised, the deadline for that action, and the final outcome. Update this log every single time you interact with the claim.

✍️ What should I write down when an adjuster calls?

During the call, write down the adjuster’s name, the current status they provide, any documents they say are missing, and most importantly, the exact date they promise to take their next action. Always follow up the call with an email confirming these points.

📧 Is an email better than a phone call for a delayed claim?

Email is almost always better because it automatically creates a time-stamped paper trail. While a phone call can be good for quick clarifications, any promises or deadlines discussed on the phone must be summarized and confirmed in an email to make them official.

⏳ How long should I wait before following up on an insurance claim?

You should follow up the day after a specific promised deadline is missed. If no deadline was given, a standard operational cadence is often to ask for a status update every 5 to 7 business days as a baseline, requesting a clear next step in writing.

📑 What proof do I need to show my claim is taking too long?

Your best proof is a written timeline showing missed deadlines. This includes your personal delay log backed up by the emails you sent confirming the target dates that the adjuster established but failed to meet.

🔁 What if my claim is transferred to a new adjuster?

Immediately log the transfer date and the names of both adjusters. Send a polite email to the new adjuster summarizing the pending items and the specific target dates promised by the previous adjuster so the timeline does not reset to zero.

📌 What if the adjuster refuses to give a target date?

If an adjuster says “we will get to it when we can,” send a confirmation email stating that no date was provided. Then, proactively set your own reasonable deadline in your log (e.g., 5 business days) and follow up when that date passes.

🎙️ Should I record phone calls with my insurance company?

Recording laws vary heavily by location and can create unnecessary friction. A far more universally effective and professional method is to simply take detailed notes in your delay log and send a summary email immediately after hanging up.

🏢 Who do I show my delay log to if the claim is stuck?

If the claim is severely stalled after multiple documented missed deadlines, you use the facts in your log to request an internal escalation. You can ask your desk adjuster to route the file to a supervisor, presenting the timeline of missed dates as the reason for the request.

🧾 What if the carrier says “we never received it”?

This is why you must maintain a robust property claim evidence pack alongside your log. If they claim a document is missing, your log should show the exact date you submitted it, allowing you to simply resend the initial transmission receipt rather than starting over.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.