- The “issued” status in your portal usually means the payment was approved by the adjuster, not that the physical check has been printed or placed in the mail.

- Before escalating, it is best practice to verify the exact mailing date, the address on file, and whether the payment was routed through a third-party vendor.

- Try not to assume the check is lost until you have tracked the operational steps: batch printing, mailroom delays, and realistic transit time.

- If the payment is legitimately late, use a structured communication loop to request a status check or a stop-payment reissue, keeping a clear written record.

The Frustration of the “Payment Issued” Status

You check your insurance portal, and there it is: a green checkmark next to the words “Payment Issued.” It is a moment of relief. You assume the funds are on their way and will be in your mailbox within a few days. But a week passes. Then two weeks. The mailbox is empty, your contractors are asking for updates, and you are stuck wondering if your insurance check is lost in the mail.

In my experience handling claims operations, this specific waiting period creates a lot of unnecessary anxiety. The core problem is often a translation error between what the insurance company’s internal software means and what a homeowner expects. When you see a status that says the payment is issued, it is easy to assume someone put a stamp on an envelope that very same day. However, the operational reality of how large carriers disburse funds is usually much more complicated.

I often see homeowners call their adjuster in a panic, demanding to know where the money is, only to find out that the check is sitting in a standard processing queue. This causes frustration on both sides. The adjuster feels they have done their job by approving the payout, and the homeowner feels they are being given the runaround. Keep in mind that the exact disbursement process can vary heavily depending on your specific carrier, your state, and your policy setup, but the core operational flow generally follows a similar path.

Key Point: Try not to mistake the date your adjuster clicked “approve” for the date the post office received your envelope. These are often two completely different milestones in the life cycle of an insurance claim.

To navigate this waiting period smoothly, you need to know exactly what to look for and how to track the status efficiently. I am going to walk you through the operational checks I recommend making before you assume the worst, and I will show you how to ask the right questions to get your claim unstuck without resorting to threats or empty ultimatums.

Why “Issued” Does Not Always Mean “Mailed”

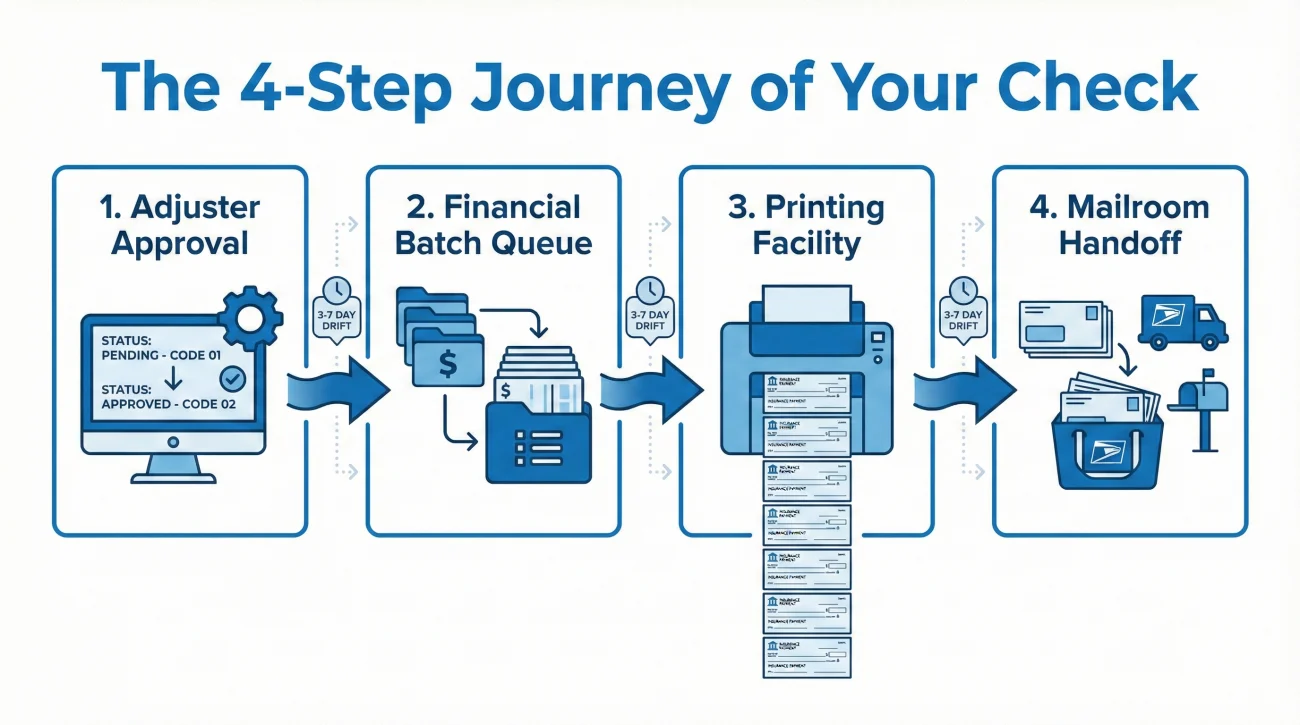

Before we dive into the specific troubleshooting steps, it helps to understand how the money actually moves. When an adjuster finishes their review and authorizes a payment, they are usually just changing a status code in their local file system. They are not walking down to a printer, signing a piece of paper, and dropping it in a mailbox.

Instead, that authorization goes into a massive daily or weekly batch. This batch is then routed to a completely separate financial department. In many cases, it is sent to an entirely different physical facility or even a third-party payment vendor. This vendor is responsible for printing thousands of checks, stuffing envelopes, applying postage, and handing them over to the postal service.

This handoff is where the timeline commonly drifts. If the adjuster approves the payment on a Friday afternoon, the financial department might not process that batch until Tuesday. The printing facility might not generate the physical paper until Thursday. By the time it actually hits the mail stream, several days or even a full week has passed, even though your portal has said “Payment Issued” the entire time.

Issued vs. Mailed vs. Cleared

To make sense of the timeline, it helps to understand the three most common financial status codes. “Issued” typically means the funds have been authorized and sent to a batch queue. “Mailed” usually means the physical envelope was handed over to the postal service. “Cleared” is trickier: while it often means you have cashed the check, some internal systems actually mark a payment as “cleared” the moment the batch is fully processed internally, before the post office even touches it.

Assuming “issued on the 1st” means it was mailed on the 1st, and panicking when it has not arrived by the 5th.

Recognizing that “issued on the 1st” likely means “printing authorized on the 1st,” and planning for a realistic window for physical delivery based on the actual mail date.

This is why maintaining clear communication is a best practice. You cannot manage a delay if you do not know where the bottleneck actually is. Gathering the operational facts first is usually the fastest way to get answers.

The 8 Operational Checks for a Missing Insurance Payment

If you have a “payment issued” status but no check, work through this specific checklist before you pick up the phone to complain. These eight checks will help you diagnose the stall point and give you the exact facts you need to ask a targeted, effective question.

1. Verify the Actual Disbursement Date

As I mentioned, the approval date is not necessarily the mailing date. Log into your portal and look for a specific line item that says “disbursement date,” “cleared date,” or “mail date.” Often, this information is hidden under a billing or payments tab, separate from the main claim summary. If you only see an “approved” date, you might not have the full picture yet.

2. Confirm the Exact Mailing Address on File

This sounds incredibly basic, but it is one of the most common reasons files go missing. People often move out of a damaged home into temporary housing. If you updated your address with the adjuster verbally, there is a chance it did not make it into the financial disbursement system. The payment system often defaults to the “property address” listed on the original policy, even if the home is currently unlivable.

❌ Note: It is risky to assume a verbal address update applies to the billing department. Always verify the mailing address in writing.

3. Check for Third-Party Vendor Involvement (The Missed Email)

Many modern carriers use third-party financial clearinghouses to handle disbursements. If this is the case, you might receive an email from a company you do not recognize (like a digital payment processor) asking you to select how you want to be paid. I commonly see claims completely stall because a payment preference email landed in a spam folder. The homeowner is waiting for a physical check to arrive, while the insurance company’s vendor is waiting for the homeowner to click “accept digital payment” or “mail a check.” If you do not select an option, the funds just sit there. Search your inbox and spam folder for any messages referencing your claim number alongside words like “payment preference.”

4. Review Co-Payee and Lienholder Requirements

If your payment requires a dual signature, the check might not have been sent to you at all. If you have a mortgage on the property, the insurer is often legally required to protect the lender’s interest. Because of this, the check might be made out to both of you. In many operational setups, the physical check is actually mailed directly to the mortgage company’s loss draft department first. It bypasses you entirely until the lender processes and endorses it. Always check your portal to see exactly who the payee is listed as.

5. Look for EFT or Direct Deposit Routing Errors

If you signed up for electronic funds transfer (EFT) or direct deposit to speed up the process, check your portal to ensure the status does not say “returned” or “bounced.” A simple typo in a routing number will cause the automated system to reject the payment. When an EFT bounces, the system usually defaults back to issuing a paper check, which resets the timeline and can add delays.

6. Check for Multiple Claim Numbers or Split Payments

Sometimes, a large payout is split into multiple checks for different coverages (for example, one check for the dwelling and a separate check for personal property). If you received a partial payment, do not immediately assume the rest is lost. Look at your breakdown. The remaining funds might still be pending a different internal review phase.

7. Calculate Realistic Mail Transit Time

Once you have confirmed the actual mailing date, add realistic postal time. Standard bulk mail from a financial center can often take anywhere from 5 to 10 business days. Do not count weekends or federal holidays. Keep a log of these dates. If it has been over 14 business days since the confirmed mailing date, it is reasonable to suspect the item might be lost in transit.

8. Review Your Communication Log

Before you reach out, review your own records. Did you miss a request for a final signature? Did they ask for a W-9 form from your contractor that you forgot to forward? Make sure the ball is entirely in their court before you escalate the inquiry.

| What You See | What It Usually Means | Your Next Action |

|---|---|---|

| Status: Approved | Adjuster finished review. | Wait for a disbursement date. |

| Status: Issued | Sent to financial batch queue. | Check payee and mailing address. |

| Status: Mailed / Cleared | Handed to postal service (often). | Track realistic transit time. |

| Status: Returned | Bad address or routing number. | Contact adjuster to correct data. |

A Realistic Mini-Scenario: Getting the Real Status

Let us look at how this plays out in a real-world setting. Imagine a homeowner named David. His portal shows that a payment for his roof repair was “issued” on the 4th of the month. By the 15th, he still has nothing in his hands.

Instead of calling and yelling at the customer service desk, David does his homework. He checks his portal and realizes the mailing address listed is still his damaged home, even though he is living in a rental. He also realizes he does not have an exact “mailed” date, only an “issued” date.

David sends a polite, structured email to his adjuster. He does not complain about the delay; he simply states the facts, asks for the operational data he is missing, and provides the correct information to fix the potential error.

Because David kept the emotion out of it and asked specific, process-oriented questions, the adjuster quickly sees the problem. The adjuster replies, confirming that the check was indeed mailed to the damaged property on the 9th. The adjuster then offers to void that check and issue a new one to the rental address. While David got a relatively quick turnaround, sometimes it still takes longer depending on the carrier’s specific reissue process. However, getting the facts straight always prevents unnecessary, prolonged delays.

How to Ask for a Payment Status Update

When you have completed your checks and given the process enough time, you need to reach out. The goal here is to get a written record of the exact status and encourage the adjuster to verify the information in the financial system, not just their claim notes.

In day-to-day operations, vague requests like “Where is my money?” usually get vague answers like “It is processing.” You often get much better results by asking for precise data points.

💡 Pro Tip: It is highly recommended to make these requests in writing. Phone calls leave no paper trail. If you do call, follow up with an email summarizing what was discussed.

Here is a clean, professional script you can use to request a status update. It focuses purely on process and documentation.

Subject: Status update request – Payment disbursement – Claim #[Your Claim Number]

Hello [Adjuster Name],

I am writing to check on the status of the payment for [mention what the payment is for, e.g., the dwelling repair estimate].

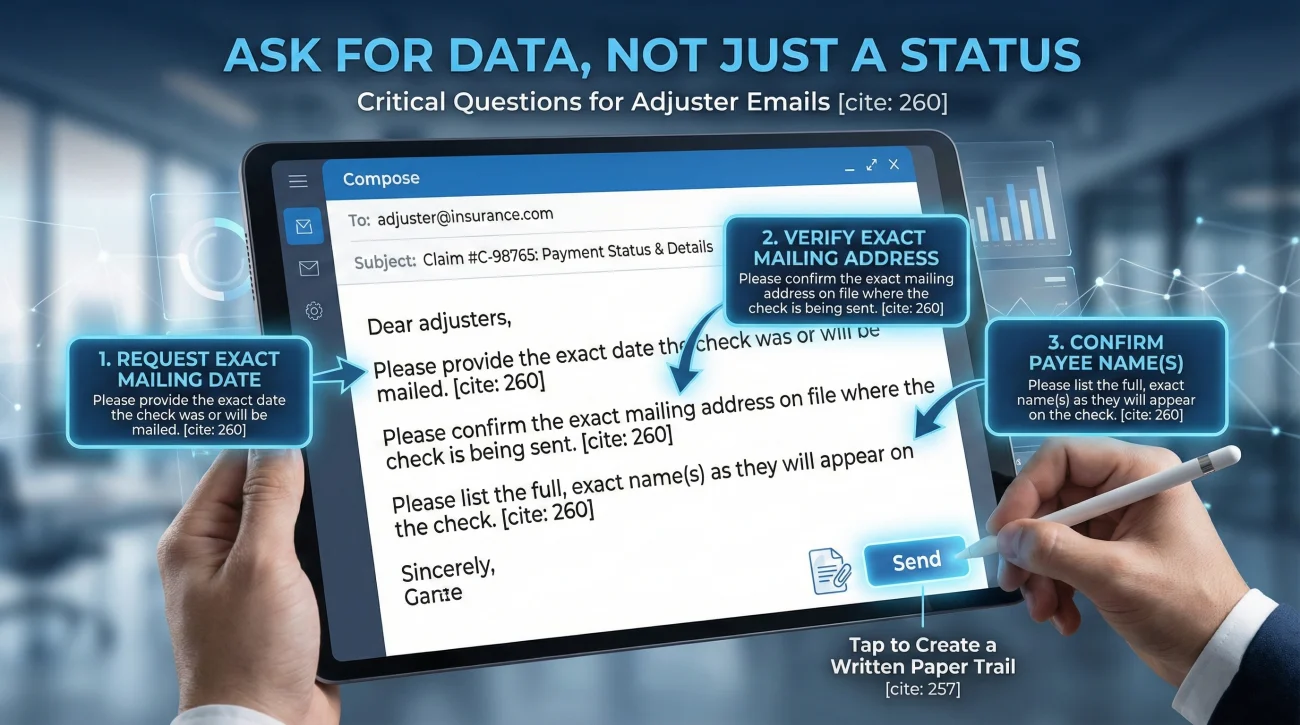

My online portal shows this was issued on [Date], but I have not received it yet. To help me track this, could you please confirm the following details in writing:

1. The exact date the physical check was placed in the mail or the transfer was initiated.

2. The exact mailing address or account it was sent to.

3. The name of the payee(s) listed on the disbursement.

Once I have this information, I can keep a proper lookout for it. If it was returned or delayed internally, please let me know what steps we need to take to resolve it.

Thank you,

[Your Name]

This script works well because it leaves little room for assumptions. It prompts the person on the other end to open the billing software, verify the address, and confirm the mailing date. If there is a problem, this format helps identify it quickly.

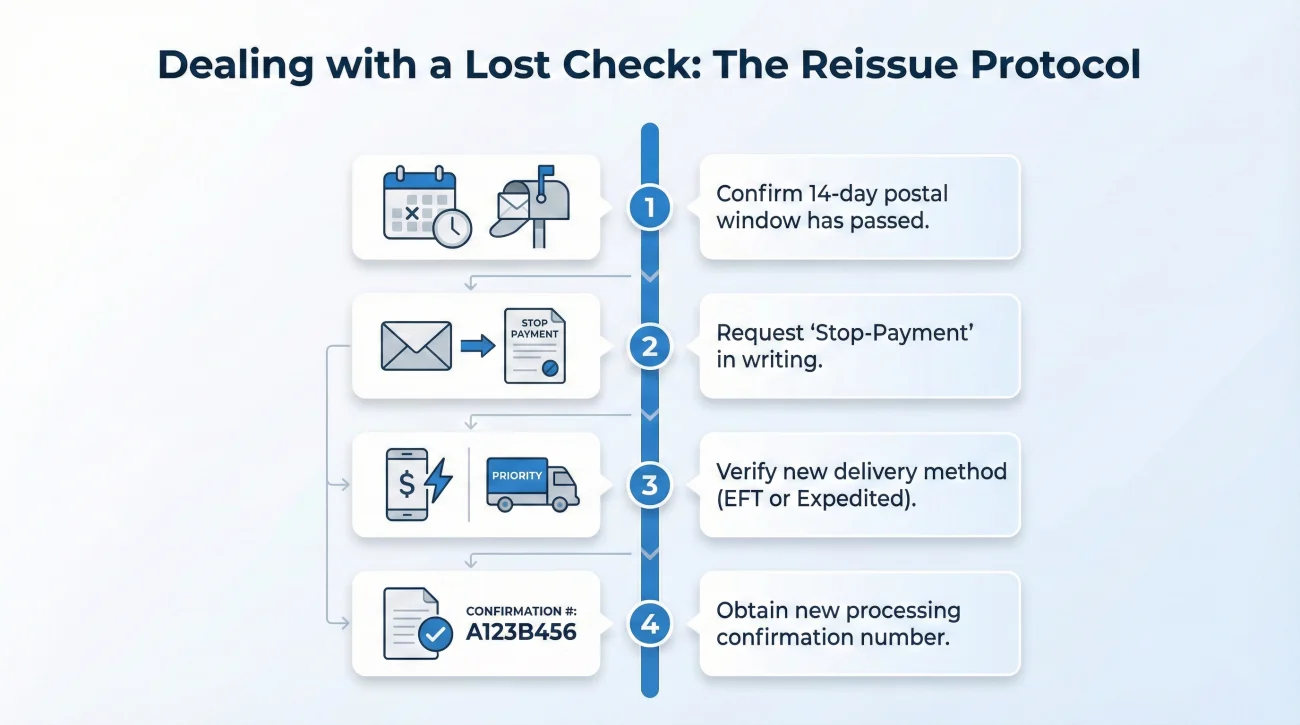

The Protocol for a Truly Lost Check

Sometimes, the mail simply fails. If you have confirmed the exact mailing date, the address is correct, and a reasonable transit window has passed (like 14 business days), you might officially be dealing with a lost check. This is an operational hurdle, but it is a common one with a clear protocol.

You typically need to formally request a “stop-payment and reissue.” This process cancels the original check so that no one else can cash it, and triggers the billing department to print a new one. Waiting indefinitely only makes it harder to track.

- 📄 What to confirm: The timeline in writing using the script above.

- ✅ What to state clearly: That the item has not arrived after the standard postal window.

- 📄 What to request: Formally ask the adjuster to initiate the stop-payment process.

- ✅ What to ask for next: A confirmation number or a new processing timeline for the reissued funds.

Here is how you can execute that in writing:

Hello [Adjuster Name],

Following up on our last message, you confirmed that check #[Check Number if known] was mailed on [Date] to [Address]. As of today, [Current Date], it has been over 14 business days, and the check has not arrived.

At this point, it appears to be lost in transit. Please initiate a stop-payment on that check and issue a replacement. If possible, I would appreciate it if the new payment could be sent via electronic transfer or expedited mail to prevent further delays.

Please confirm once the stop-payment is processed and let me know the timeline for the new disbursement.

Thank you.

This creates a helpful record showing that you did your part, waited the appropriate time, and formally requested a resolution. It documents your proactive approach to resolving the issue.

Final Thoughts on Managing the Wait

Waiting for a large payment is stressful, but understanding the machinery behind it gives you more control. When you recognize that “issued” does not automatically mean “delivered,” you can start tracking facts instead of expecting miracles. By verifying addresses, checking for vendor emails, and holding the insurer to specific dates, you eliminate a lot of the guesswork.

If you find that your payment issues are just one part of a larger pattern of delays, I highly recommend establishing a reliable claim follow-up system. Keeping a simple log of dates and requested items is often the best way to keep the operational side of your claim moving smoothly.

❓ FAQ

⏳ How long does an insurance check take to arrive in the mail?

Once the check is physically placed in the mail system by the carrier’s financial department, it commonly takes 5 to 10 business days. Do not start counting from the day the adjuster approved the payment, as printing and batching can add several days before it is actually mailed.

🤔 Why does my claim say closed but I have no check?

A “closed” status usually means the adjuster has finished their estimating process and authorized the final payment. It reflects the administrative status of the file, not the delivery status of the mail. Check your portal for a specific disbursement date.

🏦 Can I ask my insurance company to wire the money instead?

In many cases, yes. Many modern insurers offer Electronic Funds Transfer (EFT) or direct deposit options. You usually have to set this up in the online portal or sign an authorization form before the payment is approved. Ask your adjuster if an EFT form is available.

📬 What happens if my insurance check is lost in the mail?

You typically need to contact your adjuster in writing and request a “stop-payment and reissue.” The insurer will void the original check so it cannot be cashed, and then they will print and mail a new one. This process can often add extra time to your timeline.

🛑 Will the insurance company charge a fee to reissue a lost check?

In most cases, no. Insurance companies generally do not pass stop-payment fees onto the homeowner if the check was lost in transit. It is typically considered an operational cost of doing business. Just ensure you report it promptly.

🗓️ Does the “issued” date mean the day it was printed?

Usually, no. The “issued” date frequently refers to the moment the funds were authorized and sent to the billing batch queue. Actual printing and mailing might commonly happen days later, depending on the carrier’s internal processes.

🧩 Why did I only receive a partial payment?

If a large payout is split into multiple checks for different coverages (like dwelling repair versus personal property), you might receive one portion while another is still processing. Check your portal breakdown to see if the remaining funds are pending a different review.

📧 I got an email about an e-check, is this a scam?

It might be legitimate if your insurer uses a digital payment vendor. However, never click links blindly. Cross-reference the claim number in the email with your actual claim, and if you are unsure, email your adjuster directly to confirm if they sent a digital payment link.

✍️ Who do I contact if the check has the wrong name on it?

Do not attempt to cash or alter it. It is best practice to return the physical check to the insurance company and request a reissue with the correct names. Email your adjuster immediately to get the correct return mailing address and document the error.

📞 Should I call every day if the payment is late?

No, calling daily creates noise but not progress. Get the exact mailing date in writing. If the realistic transit time has not passed, wait. If it has passed, follow the formal stop-payment request process once, clearly and in writing.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.