- Escalating an insurance claim is an operational process, not an emotional reaction. Screaming for a manager rarely works.

- You must hit specific, measurable triggers before escalating, such as broken timeline promises or repeated requests for the same documents.

- Never ask for a supervisor without your “Escalation Pack” ready: a clear timeline log, a list of ignored requests, and a specific next-action goal.

- Keep the focus entirely on file movement. Leave out threats, legal language, or venting about how unfair the situation is.

- Always request the escalation in writing first to create a paper trail before trying to catch a manager on the phone.

The Reality of Demanding a Claims Manager

In claims operations, I see a distinct pattern when homeowners get frustrated. The adjuster stops responding, the timeline stretches out, and the immediate reaction is to pick up the phone, call the main customer service line, and yell, “I want to speak to a manager right now.” I understand the impulse completely. When your home is damaged and you are met with silence, the lack of control is maddening.

But from the inside looking out, an emotional demand for a supervisor is the least effective way to get your claim moving. Claims managers are essentially operations directors. They oversee hundreds, sometimes thousands, of open files. When a customer service representative flags a call with “homeowner is angry and wants a manager,” that file gets placed in a defensive posture. The manager will review it, sure, but they will be looking for ways to defend their adjuster, not necessarily ways to help you.

If you want to unstick your file, you have to learn when to escalate insurance claim internally using facts, not feelings. You need to speak the language of claims operations. While internal workflows vary slightly by carrier, state, and policy form, the core operational principle remains the same: presenting a clear, documented breakdown in the process forces management to step in and correct the workflow.

Key Point: Escalation is not a punishment for your adjuster. It is a procedural tool used to bypass an operational bottleneck when normal communication has completely failed.

In this guide, I will walk you through the exact triggers that justify an internal escalation, how to prepare your file so a manager takes you seriously, and the exact steps to initiate the handoff cleanly. If you follow this checklist, you are far more likely to be treated as a highly organized homeowner rather than just an angry caller, which helps keep your file moving.

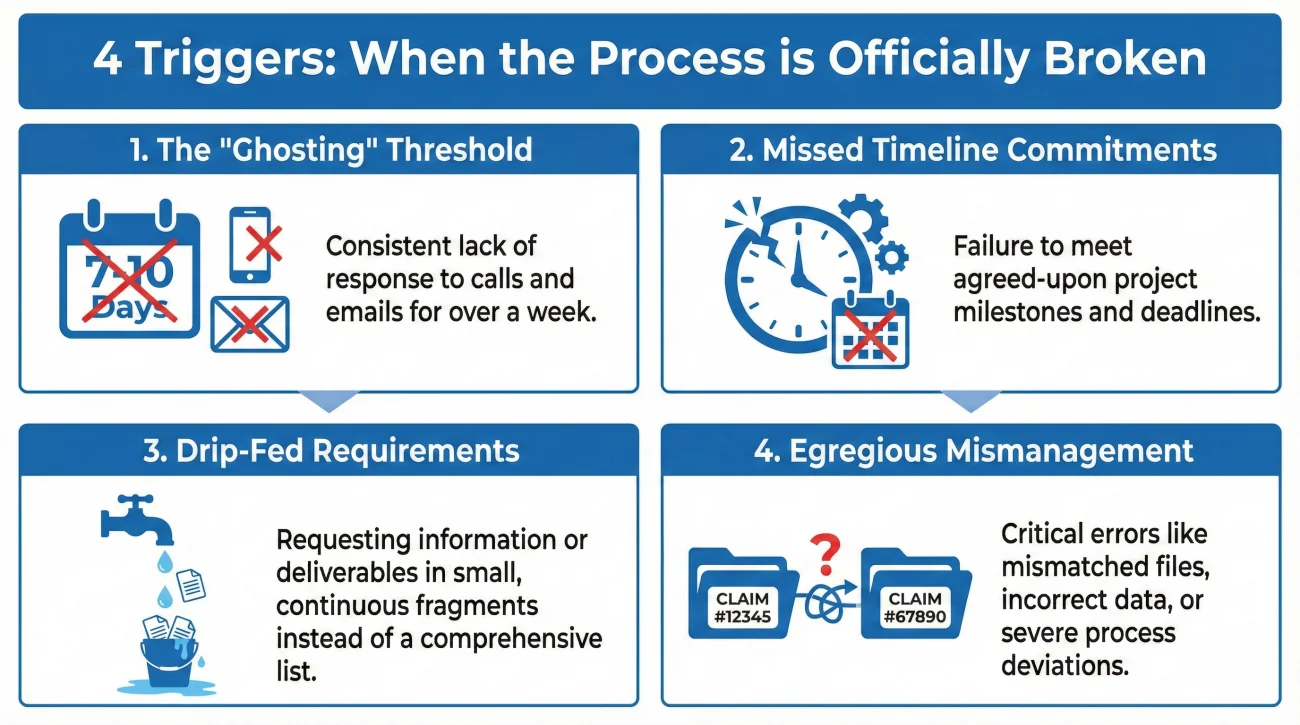

The 4 Concrete Triggers for Internal Escalation

You cannot escalate just because the process feels slow. Insurance claims are inherently slow. To get a manager’s attention, you need to prove that the process has broken down entirely. I tell people to wait for one of four specific operational triggers before they even think about asking for a supervisor.

Trigger 1: The “Ghosting” Threshold

Silence is common, but total ghosting is an operational failure. I define ghosting not as “they did not call me back today,” but rather a sustained period of ignored communication across multiple channels. If you have sent two emails and left two voicemails over the span of seven to ten business days, and you have received zero acknowledgment, you have hit an escalation trigger.

Managers track “contact metrics.” If an adjuster is failing to return calls within the company’s internal service level agreement (often 24 to 48 hours), the manager needs to know. But you must have proof of your outreach attempts.

Trigger 2: Repeatedly Missed Timeline Commitments

Adjusters frequently miss deadlines. However, there is a difference between a slight delay and a pattern of broken promises. If your adjuster explicitly states in writing, “I will have the estimate to you by Friday,” and two Fridays pass with no update and no explanation, the workflow is broken.

This trigger is powerful because it relies on the adjuster’s own words. When I review a stalled file, the first thing I look for is what was promised versus what was delivered. If a homeowner can point to three specific missed deadlines, I immediately know the adjuster has lost control of their desk.

“They take forever to do anything.”

“The adjuster promised the field report on May 12th, May 19th, and May 26th. None were delivered, and no explanation was provided.”

Trigger 3: The Endless Loop of Drip-Fed Requirements

One of the most frustrating bottlenecks is the “drip-feed.” This happens when you submit a requested document, wait two weeks, and then the adjuster asks for a different document they should have asked for on day one. You send that, wait another two weeks, and they ask for a third item. This usually indicates that the desk is not reviewing your file deeply; they are just glancing at it, finding one missing piece, and pushing it back to buy time.

In one instance I reviewed, a homeowner was asked for a contractor estimate, then two weeks later for photos, then another week later for a W-9 form. Instead of continuing the cycle, they sent a single email mapping out the three delayed requests and asked management for a “final, exhaustive checklist of all remaining requirements.” That stopped the drip-feed and forced the desk to consolidate their review. The lesson here is to escalate to cap the endless requests.

Trigger 4: Egregious File Mismanagement

Sometimes, files just get messy. If your claim number keeps changing without explanation, or if the adjuster repeatedly asks you for documents you have already submitted (and you have the email receipts to prove it), the file needs a manager’s intervention.

In one mini-scenario, a homeowner had their file passed between three desk adjusters in a single month. Suddenly, they started receiving letters referencing a commercial property they did not even own. They did not call and yell. Instead, they packaged the incorrect letters, attached timestamped emails of their actual submissions, and escalated the mix-up to a manager. The manager caught the routing error, reassigned it correctly, and approved the next step the following day. Document the chaos calmly, and let management fix the routing.

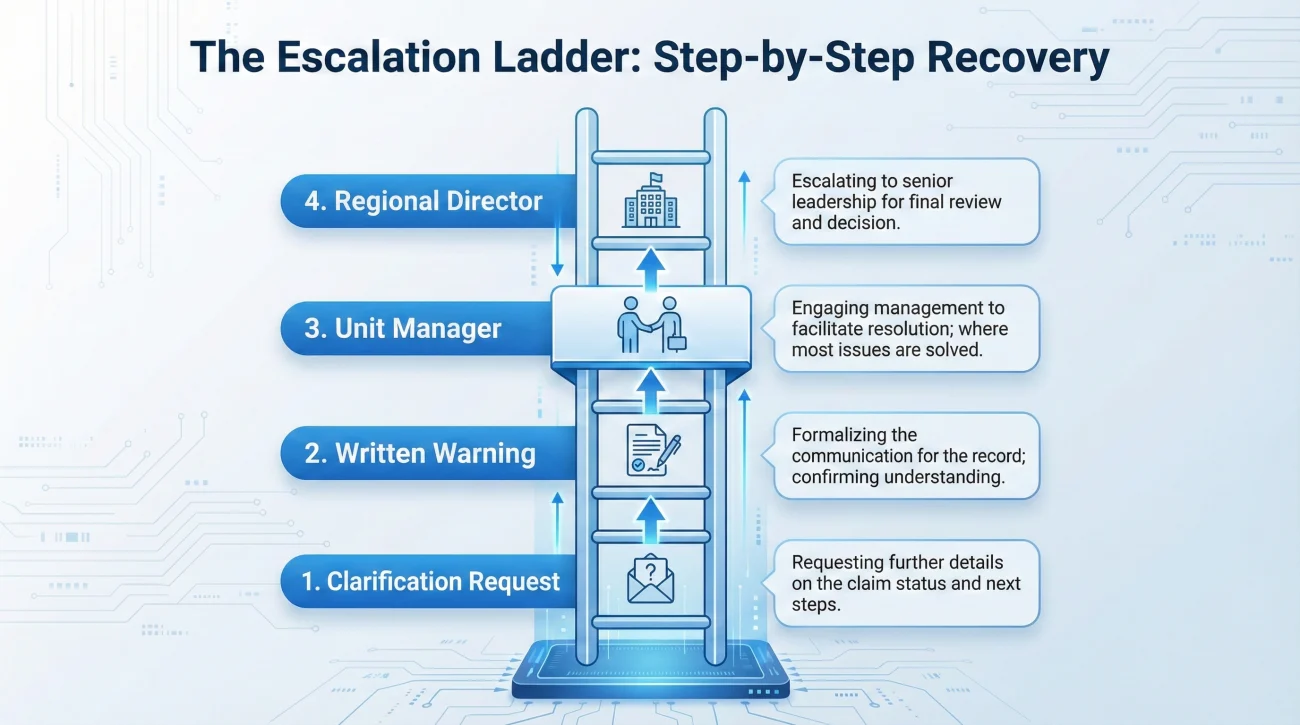

The Escalation Ladder (Severity Map)

Escalation is not a single leap to the top. It is a ladder. Jumping straight to the highest executive level usually backfires. Here is the general progression I recommend to avoid unnecessary reassignment, which only slows things down further.

- 1. The Clarification Request: Ask the adjuster directly for the next action date and confirm who owns that action. Give them a chance to self-correct.

- 2. The Written Warning: State the missed dates clearly in an email to the adjuster, establishing your paper trail.

- 3. The Unit Manager: Escalate to the direct supervisor using the broken timeline as proof. This is where 90 percent of bottlenecks are solved.

- 4. The Regional Director: This step is only used if the unit manager also ghosts you or fails to enforce the new timeline.

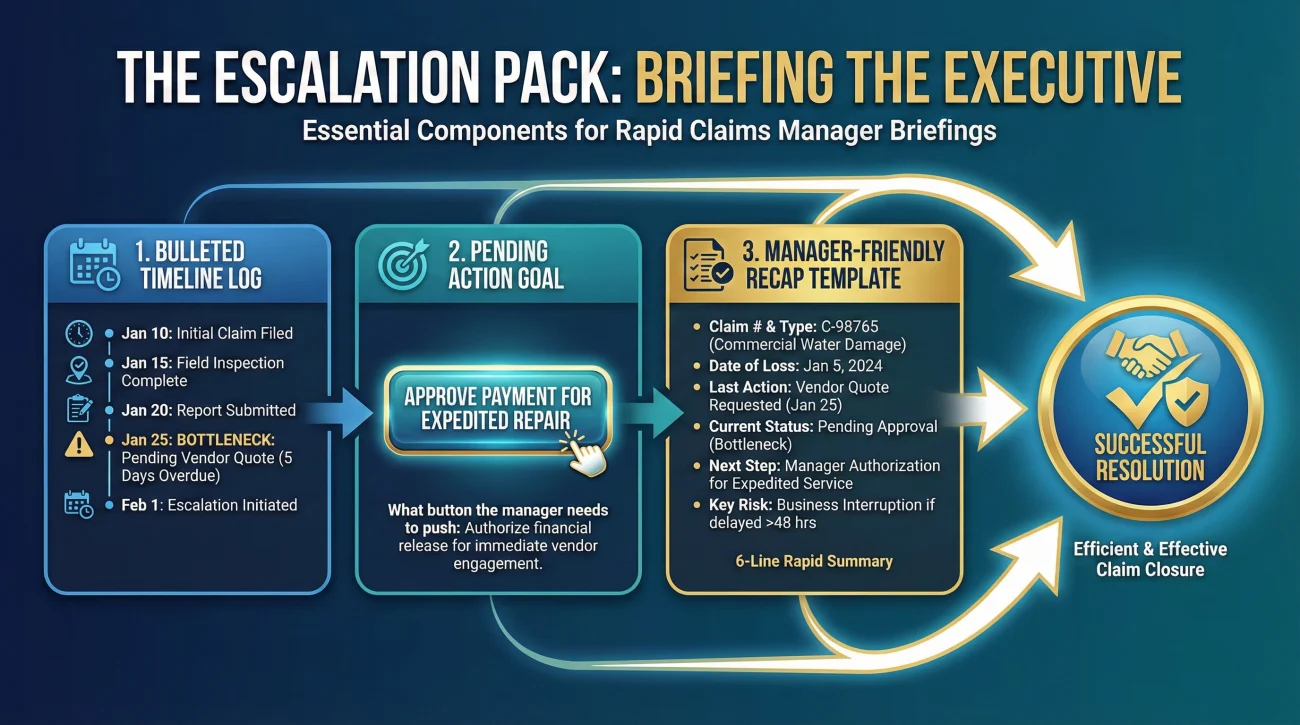

Building Your Escalation Pack (The Preparation Phase)

Before you ever type an email or pick up the phone to request a supervisor, you must build your case. Think of this as preparing a briefing for an executive. A claims manager needs to see the promised-vs-delivered gap immediately, not a ten-page emotional history of your claim.

If you have been using a standard systematic claim follow-up routine, building your “Escalation Pack” takes ten minutes. You need three specific components.

1. The Bulleted Timeline Log

This is your strongest weapon. You need a chronological list of the recent breakdown. Do not go all the way back to the date of the loss if the first three months went fine. Focus only on the current bottleneck.

- ✅ June 1: Submitted final contractor estimate via email.

- ✅ June 5: Called adjuster for status. Left voicemail. No return call.

- ✅ June 8: Emailed adjuster for status. No reply.

- ✅ June 12: Called adjuster again. Left voicemail. No return call.

2. The Pending Action Goal

Never escalate just to complain. You must clearly state exactly what action is currently pending. Are you waiting for a coverage decision? Are you waiting for a revised estimate? Are you waiting for a field adjuster to be assigned? If you say, “I am waiting for the approval on the supplemental roof estimate submitted on June 1st,” the manager knows exactly what button they need to push in their system.

3. The Manager-Friendly Recap Template

To make it effortless for a manager to review, I highly recommend formatting your core message into a rapid, 6-line recap. Paste this right at the top of your escalation request:

Pending Action:

Last Promised Date:

Missed Dates:

Previously Submitted Items:

What Is Needed Next:

💡 Pro Tip: If your trigger involves ignored documents, save your previous sent emails as PDF files so you can attach them cleanly to your escalation request. This removes any “he said, she said” debate.

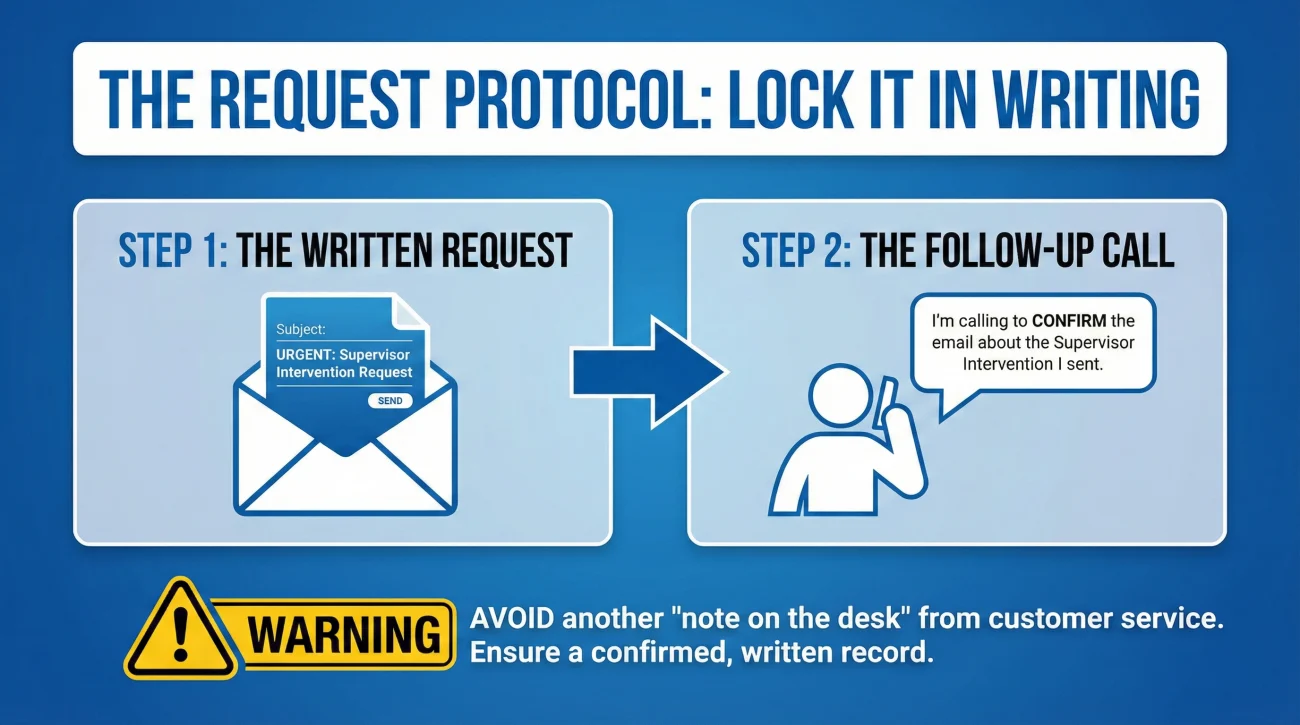

How to Actually Request the Manager

Once your Escalation Pack is ready, the method you use matters just as much as the message. Call centers are designed to de-escalate you and route you to a “team lead” who might just be another adjuster filling in for the day. The best way to escalate is in writing.

Step 1: The Written Request to the Adjuster

Your first move is to email your current adjuster, but this time, explicitly request supervisor intervention. Keep your tone perfectly neutral. State the facts and make the request.

Subject: CLAIM #12345678 – Escalation Request / Next Steps Required

Hello [Adjuster Name],

I am writing to formally request that this claim be escalated to your direct supervisor or the unit claims manager.

As of today, the claim appears to be stalled. For your reference, here is the recent timeline:

– Oct 1: I submitted the requested structural report.

– Oct 5: I emailed requesting a status update (no response).

– Oct 10: I left a voicemail requesting an update (no response).

– Oct 15: I emailed again requesting next steps (no response).

Since we have not been able to connect for over two weeks, and the structural review is still pending, I need management intervention to establish a clear timeline for the next steps.

Please forward this request to your supervisor and provide me with their name and direct contact information by the end of the next business day.

Thank you,

[Your Name]

Step 2: The Follow-Up Call

If the adjuster ignores that email, you now have leverage. Call the main customer service line. When the representative answers, you do not need to explain your whole story. You use a very specific formula.

[Action] + [What you need in writing] + [Confirmation request]

“Hello, I am calling about claim number 12345678. I have an unresolved escalation request pending with my adjuster. I need you to look up the name and direct phone number of the manager assigned to this unit, and I need you to send a high-priority internal message to that manager stating that I am holding for a call back regarding a stalled file.”

⚠️ Warning: Customer service reps often try to just leave another note for your adjuster. Politely but firmly try to ensure the message goes directly to the supervisor, rather than settling for another note left on the adjuster’s desk.

What Happens Inside the Carrier When You Escalate

Understanding the internal mechanics helps you manage your expectations. When you successfully get a manager’s attention, they perform an operational triage.

First, the manager will open your file and read the internal notes. Adjusters are required to log every interaction. If your timeline says you called on the 5th, 10th, and 15th, and the system shows no notes from the adjuster on those days, the manager instantly knows the failure is internal.

Second, they will look at the pending documents. Often, files get stalled because the adjuster does not have the authority to approve a certain dollar amount and forgot to route it up the chain. The manager can often approve these internally right then and there.

Finally, the manager will contact you. Have your Escalation Pack in front of you. They will likely apologize and ask what you are looking for. Answer operationally.

“Thank you for calling me back. I am looking for the final approval on the supplemental estimate submitted on June 1st, and I need to know exactly what day the payment will be issued.”

| Homeowner Action | Manager’s Internal Reaction |

|---|---|

| Yelling about unfairness | Defensive posture, looks to protect the company. |

| Presenting a timeline of ignored emails | Audits the adjuster’s logs, realizes the failure is internal. |

| Demanding a totally new adjuster | Hesitant, as reassignment slows the claim down further. |

| Demanding a clear list of missing items | Happy to oblige. It creates a concrete checklist for everyone. |

What Escalation Is NOT

To keep your credibility intact, it helps to understand what this process is not meant to achieve.

- ❌ Not a punishment: It is a workflow correction tool. Leave personal attacks out of it.

- ❌ Not a threat: Keep it strictly operational and focused on moving the claim forward.

- ❌ Not a demand for a new adjuster: Reassignment usually means starting over while the new person reads the history. Avoid it if possible.

- ❌ Not a social media war: Public complaints usually get routed to a PR team, adding unnecessary steps instead of unblocking your actual claim file.

Common Escalation Mistakes That Hurt Your Credibility

In my experience, homeowners often sabotage their own escalations by making predictable operational mistakes. Avoid these pitfalls to maintain a strong position.

Mistake 1: Using Legal Threats Prematurely

The absolute fastest way to shut down communication with an operations manager is to say, “If you don’t fix this, I am calling my lawyer.” The moment you threaten legal action, the timeline often slows down or communication gets rerouted entirely to their legal counsel. Once it is in the legal department, the daily workflow freezes. Never use legal threats as a negotiation tactic.

Mistake 2: Jumping to the CEO

Finding the email address of the insurance company’s CEO and sending them a massive complaint usually achieves nothing. Executives do not handle claims. The email will just get filtered down through five layers of management until it eventually lands on the desk of the exact same unit supervisor, except now it has taken an extra two weeks.

Mistake 3: Escalating Without a Paper Trail

If you have only been communicating by phone and nothing was recorded, an escalation becomes a frustrating game of “he said, she said.” Without written proof (emails, logged portal messages), the manager will default to trusting their employee. Always create a written trail before pulling the escalation trigger.

Final Thoughts on Taking Control

Learning when to escalate insurance claim internally is about recognizing the difference between a naturally slow process and a fundamentally broken workflow. It requires discipline. When you are waiting weeks for a simple answer, it feels entirely unacceptable. But you must channel that frustration into organized, documented action.

Build your timeline. Wait for the operational triggers. Remove the emotion from your emails, and present a clear gap in the workflow with absolute clarity. When you approach an escalation as an operational problem to be solved, you separate yourself from the thousands of other callers. You become credible, and in claims operations, credibility gets files moved.

❓ FAQ

🕒 How long should I wait before asking for a manager?

Wait until you hit a clear operational trigger, such as being completely ignored for 7 to 10 business days after multiple written attempts, or when the adjuster misses specific promised deadlines.

📞 What is the best way to contact a claims supervisor?

Request their contact information in writing via email from your adjuster first. If ignored, call the main customer service line and ask the representative to send an internal priority message.

😡 Will my adjuster be mad if I go over their head?

They might be mildly annoyed, but claims operations are strictly business. If they failed to manage the timeline, supervision is a normal internal process. Focus on your file.

🔄 Can a supervisor assign me a completely new adjuster?

Yes, but they prefer not to because it slows the claim down further while the new adjuster reads the history. Usually, the manager will just force the current desk to prioritize your file.

📝 Do I need to write an email or just call the main line?

Always write an email first. You need a timestamped paper trail proving that you requested escalation cleanly and professionally before navigating the phone system.

🛑 What if the supervisor also ignores my calls and emails?

If a supervisor ghosts you for more than 3 business days, you may want to consider moving one step higher. Call customer service and ask for the Regional Manager when appropriate.

🗣️ How do I find out who the adjuster’s manager is?

The easiest way is to ask customer service representatives when you call the main line. They have access to the internal directory and can see the reporting structure.

🤷♂️ Is it better to complain on social media or escalate internally?

Always escalate internally first. Social media complaints get routed to a separate PR team who will eventually just send it back to the same claims manager, causing more delays.

📁 What should I have in front of me when I talk to the manager?

Have your Escalation Pack ready: a bulleted timeline of the recent breakdown, a list of ignored emails, and the specific pending action you need them to unblock.

⏱️ Does escalating my claim reset the timeline?

It should not reset the whole claim, but expect often a short pause while the manager reviews the file history. After that, the timeline typically accelerates.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.