- An insurance check made out to your mortgage company alongside your name is standard procedure, not an adjuster error.

- Your lender holds a financial interest in the property and requires proof that repairs are being made before releasing funds.

- As a best practice, avoid mailing the physical check to your bank without first securing a written, finalized copy of the adjuster’s estimate, unless instructed otherwise.

- Document everything: take front-and-back photos of the check and send it using tracked, certified mail to avoid the “lost in the mailroom” trap.

- Keep the communication loop active by establishing a clear timeline for when the check will be endorsed or funds will be released.

The Surprise in the Mail: Two Names on the Payout

You have spent weeks going back and forth with your adjuster, organizing photos, answering questions, and waiting for a decision. Finally, the envelope arrives. You open it, expecting to take the funds straight to your local branch to kickstart the repairs. But when you look at the payee line, your heart sinks.

It is an insurance check made out to mortgage company and your name, joined by the word “and.”

In my years working in claims operations, I have seen the exact moment this reality hits homeowners. The immediate reaction is usually frustration, followed by a rush to call the adjuster to “fix the typo.” I want to pause you right there. Take a breath. This is not a mistake, and the adjuster did not do this to punish you or slow you down.

When multiple parties are listed on a settlement draft, it simply means there is a shared financial interest in the physical structure of your home. You own the home, but until the loan is paid off, the bank also holds a massive stake in it. Operational delays happen when homeowners assume they can just deposit the check or, conversely, just drop it in a standard envelope to the bank and hope for the best.

I am going to walk you through the operational realities of handling a co-payee check. We will not be diving into your specific bank’s internal portals, but we will cover exactly how you need to organize your documentation, what you need from your adjuster right now, and how to track the physical paper trail so your funds do not disappear into a corporate black hole.

Why the Adjuster Added Your Lender

Let us clear up the confusion about why this happens. When you signed your mortgage agreement, it almost certainly included a clause about property insurance. That clause protects the lender’s collateral. If your house burns down or suffers severe water damage, the house loses value. The bank needs a guarantee that the insurance money will actually go toward rebuilding that value, rather than paying off personal debt or funding a vacation.

From the insurer’s perspective, they are legally obligated to protect the interests of all known lienholders. If the insurance company were to cut a large check solely to you, and you decided to walk away from the damaged property, the bank could potentially hold the insurance company liable for bypassing them.

Key Point: The adjuster does not have the authority to remove your mortgage company from the check. Asking them to reissue it in only your name will almost always result in a firm “no,” and it will just waste valuable days on your timeline.

I always tell homeowners to expect this. If you have a mortgage, expect the bank to be on the settlement draft for the physical dwelling. (Note: Contents or personal property checks are usually made out just to you, as the bank does not hold a lien on your sofa or television).

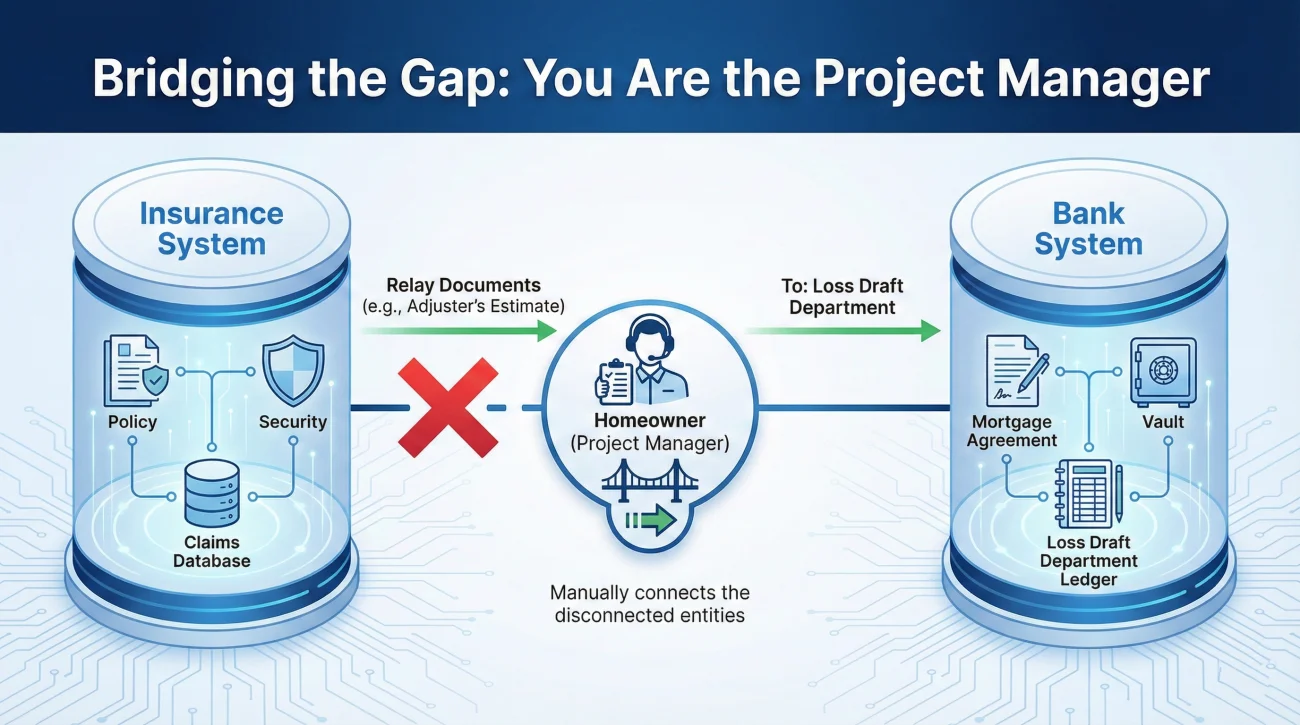

The Operational Disconnect: Where Files Go Quiet

Here is a field note from my daily operations: The biggest delays in the entire claims process often happen right after the first check is issued. The adjuster marks the file “payment sent” and moves on to their next emergency. The homeowner sees the bank’s name, mails the check to a generic address they found on their monthly statement, and waits.

Let me share a common scenario that illustrates this. I once saw a homeowner receive a large initial draft and immediately drop it in an envelope addressed to the standard P.O. Box where they sent their monthly mortgage payment. Three weeks went by. The contractor was ready to start and needed a deposit, but the bank claimed they had no record of the funds. It turned out the check was stuck in a massive general processing center because insurance drafts are handled by a completely different, specialized “Loss Draft” department. The resulting search for the paper trail delayed the repair schedule by nearly a month.

This happens because of a massive communication gap. The adjuster’s system does not talk to your bank’s system. If you send a physical check without the proper supporting documentation to the wrong department, it sits in a mailroom limbo.

Before you take any physical action with that piece of paper, you need a strategy to bridge this gap. You are the project manager here. You have to gather the documentation from the insurance side and present it perfectly to the mortgage side.

Co-Payee Wording: “And” vs. “Or”

Before we get into the paperwork, look closely at how the names are joined on the payee line. Most commonly, it will say your name “AND” your mortgage company.

When “and” is used, it legally requires the endorsement of both parties to be processed. Occasionally, you might see “or” used on a draft, though this is rare for property damage payouts. If it says “or”, the endorsement rules might be handled differently depending on the bank’s internal policies. My rule of thumb: always verify the endorsement requirement directly with the Loss Draft department, regardless of the conjunction used on the paper.

The Items to Secure From Your Adjuster

Your bank will not endorse a check or release funds blindly. They need proof of what the money is for. It is generally a bad practice to mail the check to your lender without the adjuster’s underlying paperwork, unless your bank has a specific portal upload flow that explicitly allows you to send the check first.

Even then, you must secure the final, written estimate from your insurance company. Often, an insurer will mail the check separately from the explanation of benefits or the line-item estimate. Do not assume the bank will call the adjuster to ask for it. They will not.

When you do prepare your envelope, you are essentially building a minimum information packet. At a conceptual level, this packet should typically include: your claim number, the property address, a copy of the final estimate, the payment breakdown, and your contractor’s information if you have selected one. This gives the bank the complete context they need to process the funds.

In many cases, incorporating this request into your claim follow-up system is the best way to maintain control.

Here is a safe, professional script to use if you received the check but do not have the final approved estimate:

Hello [Adjuster Name],

I received the settlement check in the mail today. Because my mortgage company is listed as a co-payee, they require a complete copy of the approved line-item estimate before they will process the funds.

Could you please email me the final PDF estimate that corresponds with this payment?

Thank you,

[Your Name]

Protecting the Paper Trail: Handling the Physical Check

When you are dealing with a live check that requires multiple endorsements, physical security and tracking become your top priorities. A lost check requires an affidavit of forgery or a stop-payment request, a reissue authorization, and weeks of waiting.

I strongly recommend avoiding treating an insurance check like a standard piece of mail.

Endorsing the check, putting a standard stamp on a plain envelope, and dropping it in a blue mailbox outside the grocery store.

Taking clear photos of the front and back of the check, logging the date, and sending it via USPS Certified Mail with a return receipt or FedEx/UPS with signature tracking.

Here is my operational checklist for the physical handling of the draft:

| Action Step | Why It Matters Operationally |

|---|---|

| Photograph Everything | If the check is lost, you need the exact check number, issue date, and exact spelling of the payee line to request a reissue quickly. |

| Verify the Address | Call your lender and ask for the specific address for the “Loss Draft Department” so it does not end up in general billing. |

| Use Tracked Shipping | A tracking number proves exactly when the bank received it. This is your proof if there is confusion later regarding its arrival. |

| Log the Journey | Write down the day you sent it, the day it arrived, and consider a follow-up shortly after confirmed delivery, usually within 1 to 2 business days. |

❌ Note: It is best practice to avoid endorsing (signing) the back of the check until you have confirmed your bank’s specific rules. Some banks require you to sign it before sending; others require you to wait. Always ask the Loss Draft department for their exact requirement before putting pen to paper.

Avoiding the “Stale Check” Trap

There is a hidden countdown clock on every piece of paper an insurer issues. Most insurance settlement drafts have a printed expiration date, usually “Void after 90 days” or “Void after 180 days.”

In the claims world, we call an expired draft a “stale check.” If your check gets stuck in a dispute with your bank, or if you hold onto it while trying to fight the adjuster for a higher amount, the clock keeps ticking. If the check goes stale, your bank cannot deposit it, you cannot cash it, and you have to go back to the insurer to request a reissue.

Requesting a reissue resets your timeline completely. The insurer’s accounting department has to verify the old check was not cashed, place a hard stop on it, draft a new one, and mail it out. This process often takes weeks depending on the carrier.

💡 Tip: Keep the paper moving. Even if you disagree with the total amount of the settlement, an undisputed actual cash value payment can usually be processed without waving your rights to supplemental claims later. (Always verify this in writing with your adjuster). Getting the initial funds processed by the bank allows your contractor to start demolition and mitigation while you work on the rest.

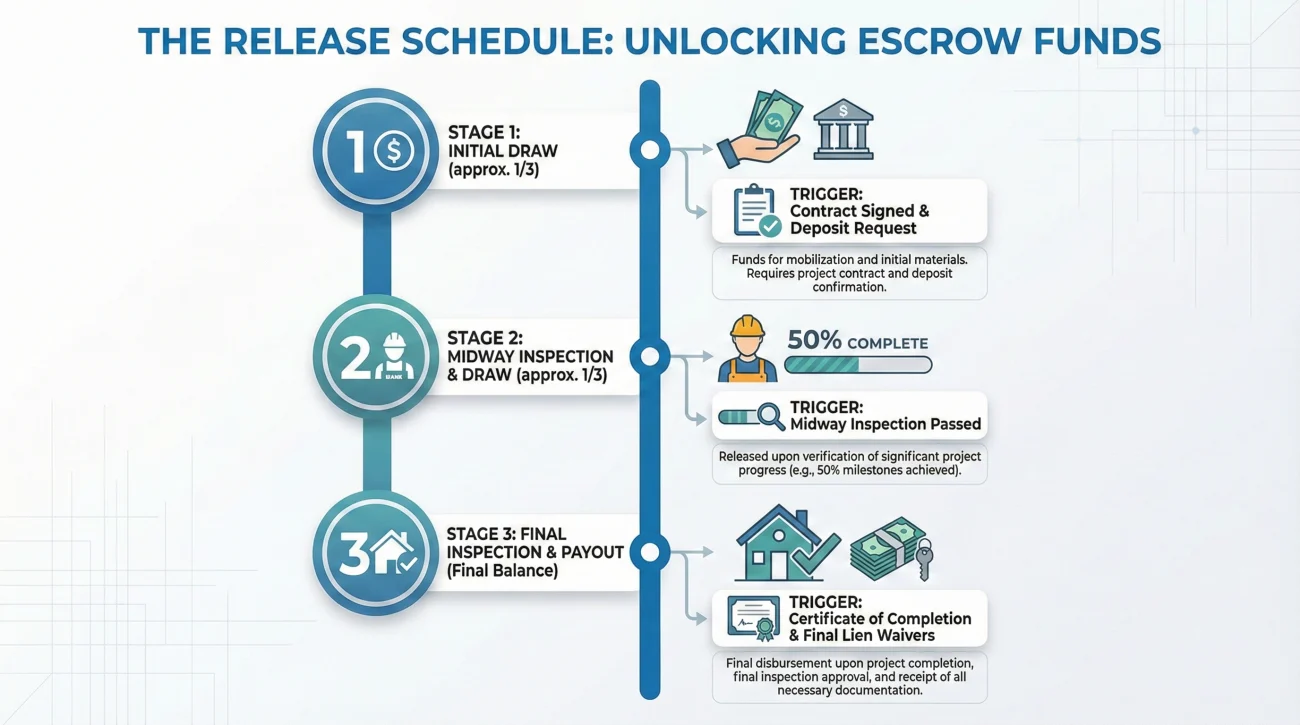

Managing the Bank’s Release Schedule

Once the bank has your check and the adjuster’s estimate, another operational hurdle appears: the release schedule. I often see homeowners shocked when the bank deposits a $30,000 check but only releases $10,000 to them.

This is standard risk management. Lender policies vary significantly, but they commonly release the money in fractions, often one-third upfront, one-third at the midway point, and the final third after a physical inspection proves the work is fully complete.

To avoid cash flow crises with your contractor, you need to establish this timeline on day one.

Action + What you need in writing + Confirmation request

When you speak to the Loss Draft department, request their release schedule in writing. You want an email or a portal document that explicitly states what triggers the next payment. Is it an inspection? Is it a signed w9 from the contractor? Is it a certificate of completion?

- ✅ Ask: “What documentation is required to release the first draw?”

- ✅ Ask: “How do we schedule the midway inspection?”

- ✅ Ask: “Are there any contractor documents you need on file before releasing funds?”

When you have these answers, pass them immediately to your contractor. If your contractor expects 50% upfront but the bank only allows 30%, you need to negotiate that gap before the hammer swings, not after.

Final

Seeing an insurance check made out to mortgage company is just a procedural step in a much larger machine. It feels like a roadblock, but it is really just a routing issue. By understanding that the adjuster and the bank do not communicate directly, you can step in to keep the loop active.

Gather the underlying paperwork, confirm the correct Loss Draft mailing address, track the physical package carefully, and request clear release milestones in writing. If you maintain strict documentation hygiene and control the paper trail, you will push through this bottleneck without letting your claim go stale. Stay organized, stay calm, and keep the process moving forward.

❓ FAQ

🏦 Can I just cash the insurance check without my mortgage company?

No. If the bank is listed as a payee, the check requires their endorsement to be legally deposited or cashed. Banks will flag and reject checks that lack the required secondary signature.

✍️ Should I sign the back of the check before mailing it to my lender?

It is best practice to check with your specific lender’s Loss Draft department first. Some require your signature beforehand, while others want to endorse it first and send it back to you. Do not guess; get their requirement in writing.

📬 Where do I mail the insurance check to my mortgage company?

Avoid mailing it to the address where you send your monthly payments. You should contact your lender and ask for the exact mailing address of their “Loss Draft Department” or “Insurance Claims Department.”

📑 What documents does the mortgage company need with the check?

They commonly require the insurance company’s final, approved line-item estimate, though this varies by lender. Many also ask for a contractor’s estimate, a W-9 from your contractor, and a signed conditional waiver of lien.

⏳ How long does the mortgage company hold the insurance money?

It depends on their internal procedures and the size of the loss. Typically, they release a percentage upfront to start repairs, and hold the rest in escrow until inspections prove the work is progressing or completed.

🔄 Will the adjuster talk to my mortgage company for me?

Generally, no. Adjusters issue the payment based on the policy and lienholder records, but they do not manage the bank’s escrow or release process. You are responsible for bridging that communication gap.

🛑 What happens if the insurance check expires while at the bank?

If the check passes its void date, it becomes a “stale check.” You will have to ask the adjuster’s accounting department to void the original draft and issue a new one, which causes significant delays.

📉 Does the mortgage company get to keep the leftover insurance money?

If repairs are completed to their satisfaction and the property is restored to its previous value, any remaining funds designated for the dwelling are typically released to you or applied to your principal balance, depending on your loan terms.

📱 Can I deposit a co-payee insurance check using a mobile app?

Almost never. Most lenders do not allow mobile deposits for two-party insurance drafts, especially for large amounts. They usually require physical presentation and verification of all endorsements.

⚖️ If I disagree with the claim scope, should I still send the check?

Usually, you can process an undisputed actual cash value payment to start initial mitigation and repairs. However, you should always confirm in writing with your adjuster that cashing the check does not waive your right to file supplemental claims later.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.