- A claim that goes completely quiet usually means it has fallen off the active operational dashboard, often due to desk turnover or missing system triggers.

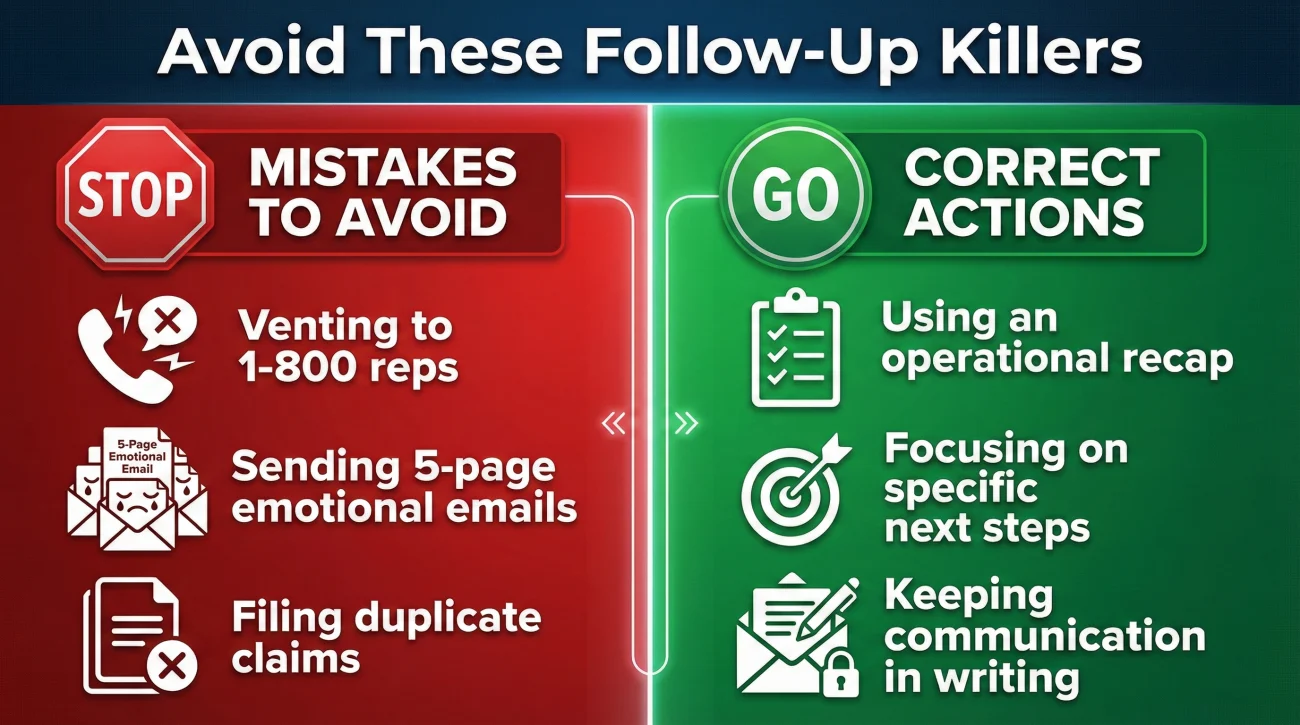

- Do not send an angry email or start a brand new claim; both actions create more administrative mess and often delay the process further.

- Use the “Continuity Recap” method to provide a short summary of the last completed action, helping to force the file back into active status.

- Never assume your previously submitted documents are lost, but be prepared to point the adjuster to the exact date and time stamp you sent them.

- When you try to reactivate a claim, keep communication in writing whenever possible to re-establish a clear, traceable timeline.

The Silence Phenomenon: When Your File Goes Dark

You sent in the contractor estimate, answered all the questions, and waited. At first, you checked your email every day. Then every week. Now, two or three months have passed, and you have heard absolutely nothing. In the operational world of property claims, we call this the silence phenomenon. You feel like you have been ghosted, and you are left wondering if you need to restart the claim from scratch.

In day-to-day claims ops, I see this happen all the time. As a homeowner, your natural instinct is to assume the insurance company is intentionally ignoring you to avoid paying. While policy rules and timelines vary by carrier and state, the reality behind the scenes is usually much more mundane: your file has likely slipped off the active dashboard.

Insurance adjusters handle massive volumes of files. If a task notification clears without generating a new follow-up date, or if your adjuster leaves the company and their files are bulk-transferred, your claim can sit in a digital filing cabinet gathering dust. The system does not always flag it as “overdue” if the internal software thinks it is waiting on you.

My goal here is to help you break that silence without starting over. We are going to use an approach I call the “Ghosted” Protocol. It is not a secret trick; it is simply a clean, operational way to format a recap so your file gets pulled from the bottom of the digital pile and put directly in front of a decision-maker.

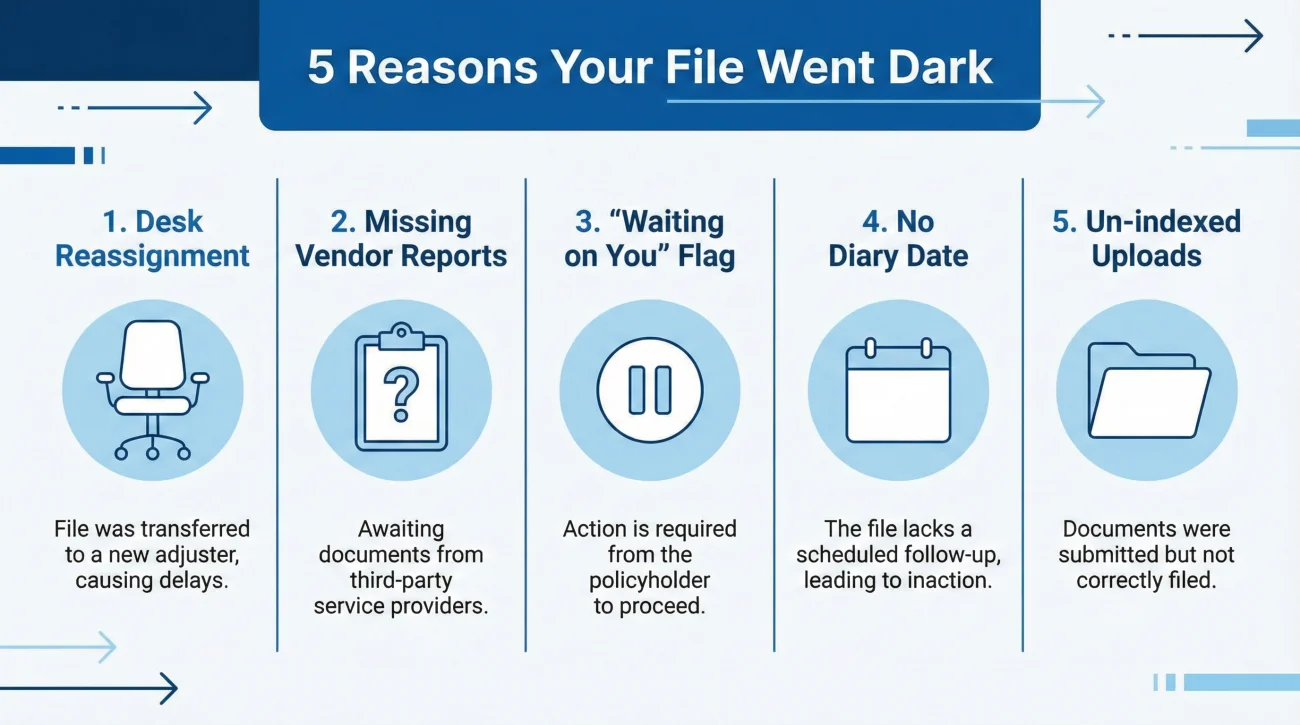

Why Files Go Dark: The 5 Operational Reasons

Before fixing the delay, it helps to understand why the file stopped moving. In most cases, it falls into one of five operational buckets:

- Desk Reassignment: Your adjuster left, and the file is sitting in a bulk transfer queue waiting for a new owner.

- Missing Vendor Reports: The desk adjuster is waiting on an independent field inspector or engineer to upload their findings.

- The “Waiting on You” Flag: The software thinks it sent you a request for information, and the system clock is paused until you reply.

- No Diary Date: A diary date (or follow-up task) was cleared by mistake, meaning the file will not pop back up on the adjuster’s daily screen.

- Un-indexed Uploads: You uploaded a document to the portal, but it was not properly tagged or routed to the adjuster’s immediate attention.

The Biggest Mistakes When Reactivating a Dead File

When a claim has been stalled for months, stress takes over. Homeowners often try to force the issue using tactics that accidentally create more delays. Before we walk through the framework, we need to eliminate the common mistakes that ruin a clean restart.

📌 Note: The most common error is calling the general 1-800 number and venting to a first-level customer service representative. They do not have the authority to move your claim forward; they can only leave a generic note in the system. This does nothing to solve the underlying routing bottleneck.

Another major trap is the emotional email. When you send a five-page email detailing every frustration over the last six months, you bury the actual operational request. If a new adjuster inherits your claim and opens a massive wall of text, it takes them longer to figure out what is missing. We want to establish clear ownership and ask for a specific next action date, rather than focusing on the past.

“I have been waiting for three months and no one is calling me back! This is unacceptable. Are you guys ever going to process my claim or do I need to start a whole new one? Call me immediately!”

“Following up on Claim #12345. It has been 60 days since the last action. Below is a brief continuity recap to help us get this back on track. Please advise on the current status.”

Finally, avoid filing a duplicate claim for the same event just because the first one stalled. Duplicate claims often trigger administrative freezes or fraud alerts. It will lock your progress entirely until a supervisor manually merges the two files.

The Pre-Contact File Audit

Before you send any communication to restart the process, you must know exactly where the process stopped. You cannot rely on the adjuster to remember your file. You need to become the authority on your own claim timeline.

In many cases, the insurer’s system might show that they are waiting on you. Perhaps your contractor promised to send a revised line-item estimate directly to the desk adjuster, but forgot to attach it to the email.

Key Point: The person who controls the timeline is the person who has the most organized documentation. Always know exactly what was sent, when it was sent, and who acknowledged it last.

Do a quick review of your records. Find the very last email you received from the insurer, or your notes from the last phone call. Identify the “Last Action Completed.” Did they acknowledge receipt of your photos? Find the exact date of that action. Then, identify the “Pending Action.” What was supposed to happen next?

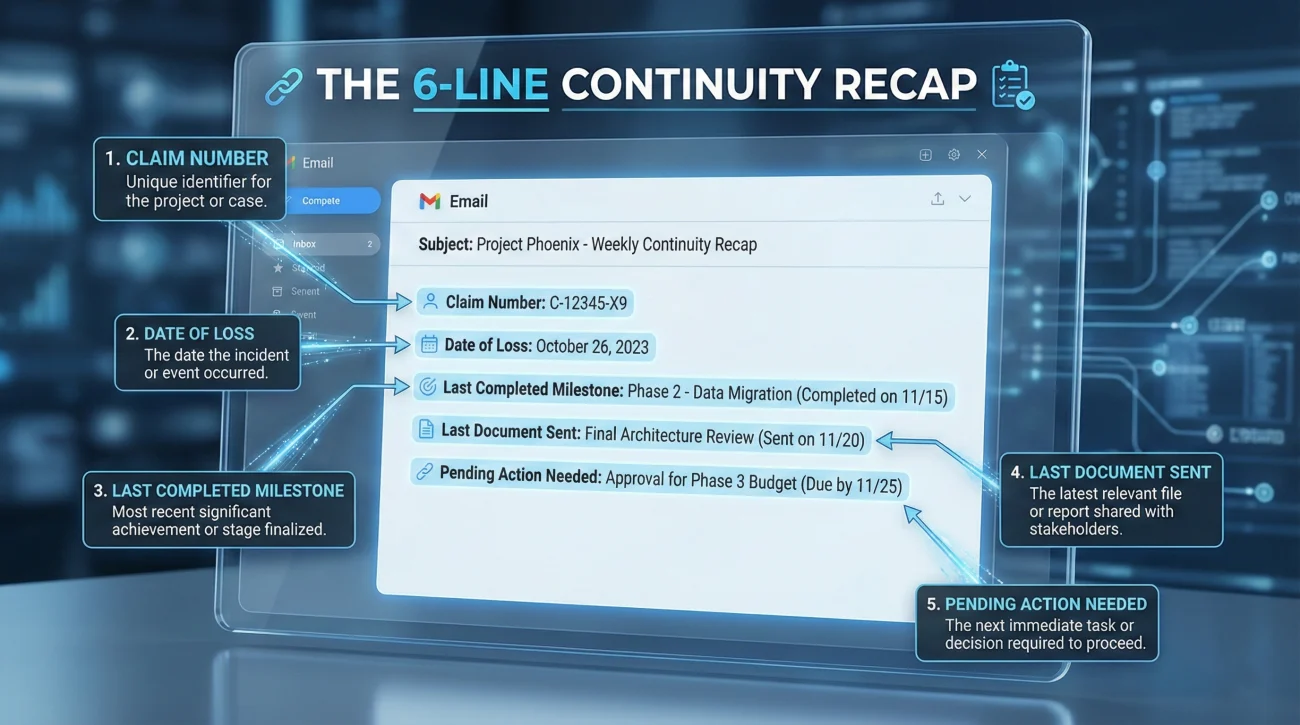

Building the Continuity Recap

A Continuity Recap is a highly structured, plain-text summary of your claim’s current status. It serves a very specific operational purpose: it allows an adjuster (especially a new one who just inherited a messy desk) to understand exactly what is needed without reading past emails.

When I review files that have been stuck, the fastest way to get them unstuck is to see this summary. It removes all the guesswork and provides the exact file dates needed to move forward.

Your Continuity Recap should ideally be a 6-line format that includes these specific data points:

| Recap Field | Purpose in the Process |

|---|---|

| Claim Number | Ensures immediate routing to the correct digital file. |

| Date of Loss | Anchors the timeline. |

| Last Completed Milestone | Proves what has already been done (e.g., “Field inspection completed on Oct 12”). |

| Last Document Sent | Points them to the exact file they need to look for (e.g., “Estimate emailed on Nov 5”). |

| Pending Action Needed | Tells them exactly what you are waiting for them to do. |

Field Note: The Reality of Desk Handoffs

Let me share a common pattern you see behind the curtain. Often, a claim goes silent because the original adjuster left the company. Their pending files are reassigned to a new adjuster.

Imagine being that new adjuster. You log in on Monday and find 80 unfamiliar claims dumped into your queue. If Homeowner A sends an email saying, “Why haven’t I heard back?”, you have to dig through the entire history to figure out what is missing. That takes time, so it gets put off.

But if Homeowner B sends an email with a Continuity Recap that says, “I am waiting on the review of the mitigation invoice sent on March 4th,” you know exactly what to do. You open the file, find the March 4th document, review it, and move it forward. When possible, aim to be Homeowner B.

Executing the Request (With Scripts)

Now that your audit is done and your recap is built, it is time to send the message. Send this via email if possible, or through the official online claim portal. You want a time-stamped record that you initiated the restart.

Here is a highly effective template. Notice how it assumes positive intent while remaining incredibly firm about getting a status update.

Subject: CLAIM STATUS UPDATE REQUIRED: Claim # [Your Claim Number] – [Your Last Name]

Hello [Adjuster Name, or “Claims Department” if unknown],

I am writing to check the status of my property claim, as I have not received an update in over [number] days. To help quickly bring this file up to date, I have provided a brief continuity recap below:

– Claim Number: [Number]

– Last Action Completed: [e.g., Independent adjuster inspected the property on Date]

– Last Document Submitted: [e.g., Contractor’s supplemental estimate sent via portal on Date]

– Pending Action: [e.g., Waiting for the desk adjuster to review the supplement and issue the updated estimate]

Could you please review the file and reply with a written confirmation of the current status? If you are missing any documents from me, please provide a specific list so I can send them immediately.

Thank you for your help in keeping this moving.

[Your Name]

If they reply and say they need a document you already sent, do not argue. Simply reply, “Thank you for confirming. I originally sent that on [Date], but I have attached it here again for your convenience.” Getting the file moving is the priority.

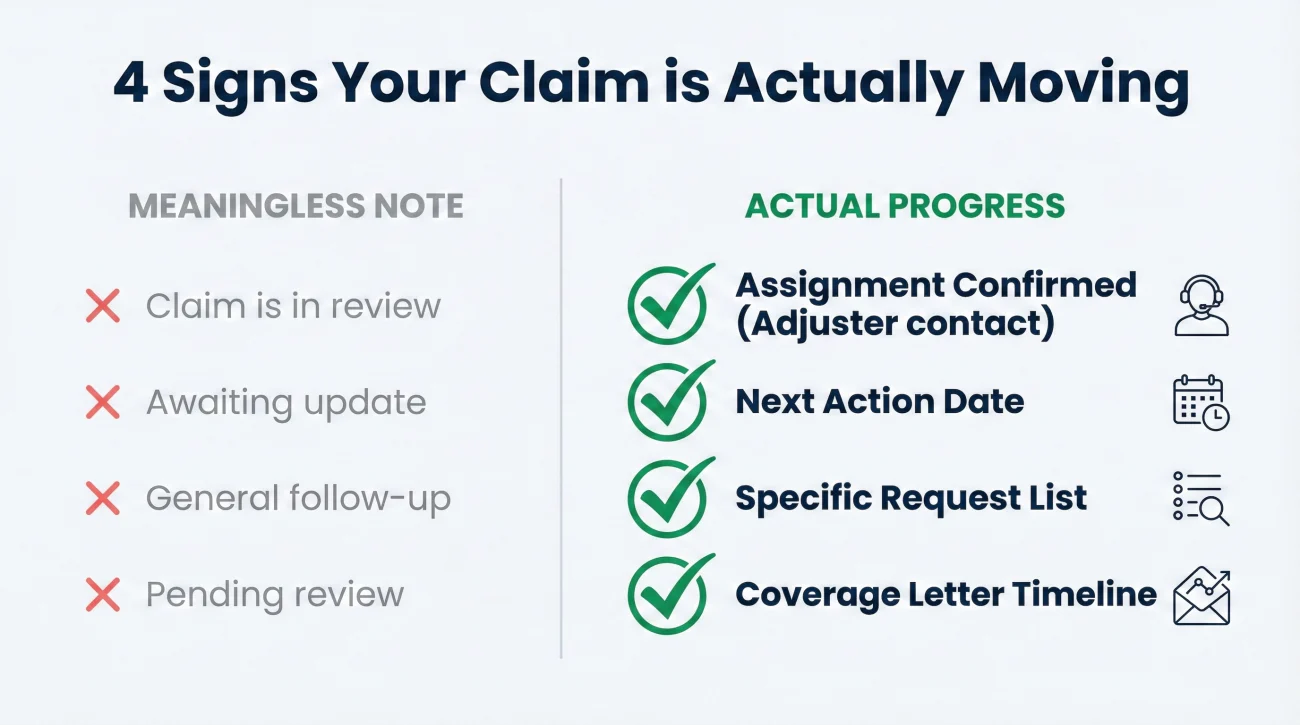

Is It Just a Note, or Actual Progress?

When you do get a response, you need to differentiate between a generic “note added” and actual file movement. A customer service rep saying “I left a note for the adjuster” is not progress. Real progress has specific operational markers. Look for these four signs that your file is actually moving forward:

- Assignment Confirmed: You receive the name and direct contact info of the specific person who now owns the file.

- Next Action Date: You are given a specific date by which a review or decision will be made.

- Specific Request List: Instead of “we are reviewing,” you get a bulleted list of exactly which documents are missing.

- Coverage Letter Timeline: You are told when the formal coverage or estimate letter will be issued.

Real-World Scenarios: Getting It Unstuck

Let’s look at two realistic mini-scenarios to see how this plays out in practice.

Case 1: The Unmonitored Queue

One homeowner suffered water damage and submitted final drying logs in early February, but by late April, they had heard nothing. Instead of calling the routing desk, they drafted a Continuity Recap noting the February submission and stating they were waiting on the final coverage determination. They emailed it in, and two days later received a reply from a new adjuster. The original adjuster was on extended leave, and the file had been sitting in an unmonitored queue. Because the recap was provided, the new adjuster verified the drying logs and pushed the file to the next status immediately.

🎯 Conclusion: Good process bypasses operational chaos.

Case 2: The Stuck Vendor Report

In another case, a roof claim stalled for 45 days after the field inspection. The homeowner sent a Continuity Recap and learned the desk adjuster was waiting on the third-party inspector’s photo report, which had failed to upload correctly to the system. By identifying the exact missing piece, the adjuster was able to call the vendor, get the photos emailed directly, and issue the estimate the next day.

👉 The lesson: Pinpointing the exact bottleneck is faster than simply complaining about the delay.

What If The Recap Is Ignored?

In most cases, the recap works because it gives a busy adjuster an easy win. But what happens if another week goes by with absolute silence? Now you have an operational failure that requires escalation.

Do not jump to legal threats. When you threaten an insurer, many internal protocols dictate that the file must be transferred to a legal or compliance department, which can stall your claim for even longer. If the recap approach does not work, here is one possible escalation path aimed at keeping a clean timeline:

- 📄 Action 1: Forward your email to the general claims support address. Add a line stating: “I have not received a reply from the assigned adjuster. Please route this to the managing supervisor for this file.”

- ✅ Action 2: Call the general support line. Give them your claim number, tell them you sent a status request that went unanswered, and ask for the direct email of the claims manager.

- 📄 Action 3: Send the Continuity Recap directly to that manager, noting clearly how many days the file has been inactive.

Managers often assign stalled files to a senior adjuster to fix the delay once they see a clear timeline of an unworked file.

Maintaining Momentum: The Follow-Up Habit

Once you successfully revive the claim, you cannot go back to simply waiting. A stalled claim is a symptom of a weak tracking process. You have to take control of the timeline moving forward.

This means implementing a rigid logging habit. Every time you send an email, you log it. Every time you have a phone call, you follow up with a quick email summarizing the call. If you need a guide on how to build a bulletproof tracking habit, you should review our core claim follow-up system.

From this point on, you must end communication by asking for a date. The formula is simple:

[Action] + [What you need in writing] + [Confirmation request of the next date]

💡 Pro Tip: If the adjuster says, “I will review this and get back to you,” your immediate response should usually be, “Thank you. Just so I can mark my calendar, by what date should I expect to hear back from you on that review?”

Final Thoughts on Regaining Control

Having a claim stall out is an isolating experience, but it is vital to remember that it is almost always a paperwork or system routing failure, not a personal attack. By stepping back, auditing your own file, and communicating like a fellow claims professional, you strip away the confusion.

The Continuity Recap is a solid tool for cutting through the noise. Keep it brief, keep it factual, and routinely ask for the next steps in writing. Once you get the file moving again, protect that momentum by maintaining a strict follow-up schedule.

❓ FAQ

⏳ How long should I wait before considering my claim “stalled”?

In general, if you have not received an update or a request for information in 14 to 21 days after your last submission, the file is drifting. If it hits 30 days of total silence, it usually requires an operational restart.

🔄 Will restarting a stalled claim put me at the back of the line?

No. You are not filing a new claim; you are reactivating an existing one. Providing a clear continuity recap often helps you bypass the line because it makes your file easier for the adjuster to work on.

📂 Do I have to resend all my documents if the claim went quiet?

Not necessarily. Start by pointing out the dates you already sent them. However, if a new adjuster asks for a specific document again, it is usually faster to just resend it.

👤 What if my original adjuster quit or was fired?

This is a common cause of delays. Your file will be reassigned. A good approach is to send your continuity recap to the general claims email address, asking them to route it to the newly assigned desk adjuster.

🚫 Should I just start a new, duplicate claim to get their attention?

Generally, no. Filing duplicate claims for the same loss creates administrative confusion, often triggers internal fraud alerts, and can stall your progress even further.

🔎 How do I find out who has my file now?

Call the main customer service number, provide your claim number, and politely ask to check the system for the name and direct email address of the current assigned adjuster.

🔒 Can the insurance company close my claim for inactivity?

Yes, many systems are programmed to auto-close or suspend files if there is no activity from the homeowner for a certain period (often 60 to 90 days). A written request is usually required to reopen it.

📝 What if they reply and ask for things I know I already sent?

Stay calm. Reply nicely: “Thank you for confirming what is needed. I originally submitted those on [Date], but to keep things moving quickly, I have attached them to this email again.”

☎️ Should I call or email to restart a dead claim?

Email or portal messages are generally better for restarting a claim. You need a written, time-stamped record of your summary and your request for status.

❌ Does a stalled claim mean it is going to be denied?

No. A stalled claim usually points to a workflow problem, such as staff turnover, a missed software alert, or a missing document, rather than a definitive coverage decision.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.