- A holdback (often called recoverable depreciation) is a portion of your claim settlement that is held back until you prove the repair work is complete.

- To unlock these funds, you typically need to provide a final invoice from your contractor and clear photos showing the finished work.

- Avoid sending a final invoice with a blank subject line; always include your claim number, a polite request for the release, and an organized attachment list.

- If you are managing multiple contractors, you can often request partial holdback releases as each specific trade finishes their portion of the project.

The Shock of the First Check: Why It Looks “Short”

Opening that first piece of mail from the desk adjuster can be a highly stressful moment. You look at the contractor’s estimate, you look at the check in your hand, and there is a massive gap between the two numbers. For many people, the immediate reaction is panic. You might think the claim was partially denied, or that you are somehow expected to pay the difference out of pocket.

If you are looking at your paperwork and wondering why the numbers do not match up, take a deep breath. In most standard replacement cost policies, this is exactly how the process is designed to work. You are likely encountering the concept of a holdback. Understanding exactly what is holdback in insurance claim processing is the first step to getting your property fully restored and getting the rest of your funds released.

I have spent years looking at claim files, reviewing documentation, and helping untangle communication breakdowns. In my experience, the holdback process is one of the most common sources of confusion, simply because it is rarely explained in plain English upfront. The paperwork is dense, the columns of numbers are confusing, and the instructions on how to get the rest of your money are often buried in a generic form letter.

Today, I want to walk you through exactly what this mechanism is, why it exists, and most importantly, the reliable approaches you can take to organize your proof and request that final payment. Keep in mind that specific timelines and requirements can vary by policy, carrier, and state, but the core mechanics of proving completion remain similar across the board.

Key Point: A holdback is not a penalty. It is a standard accounting mechanism used to ensure that the damaged property is actually repaired or replaced before the final funds are released.

What Exactly Is an Insurance Holdback?

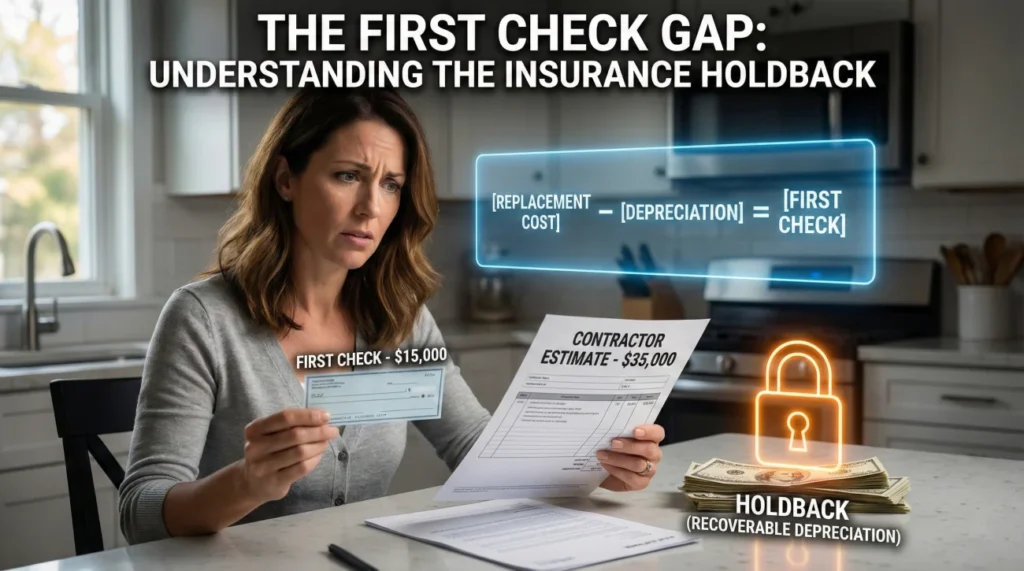

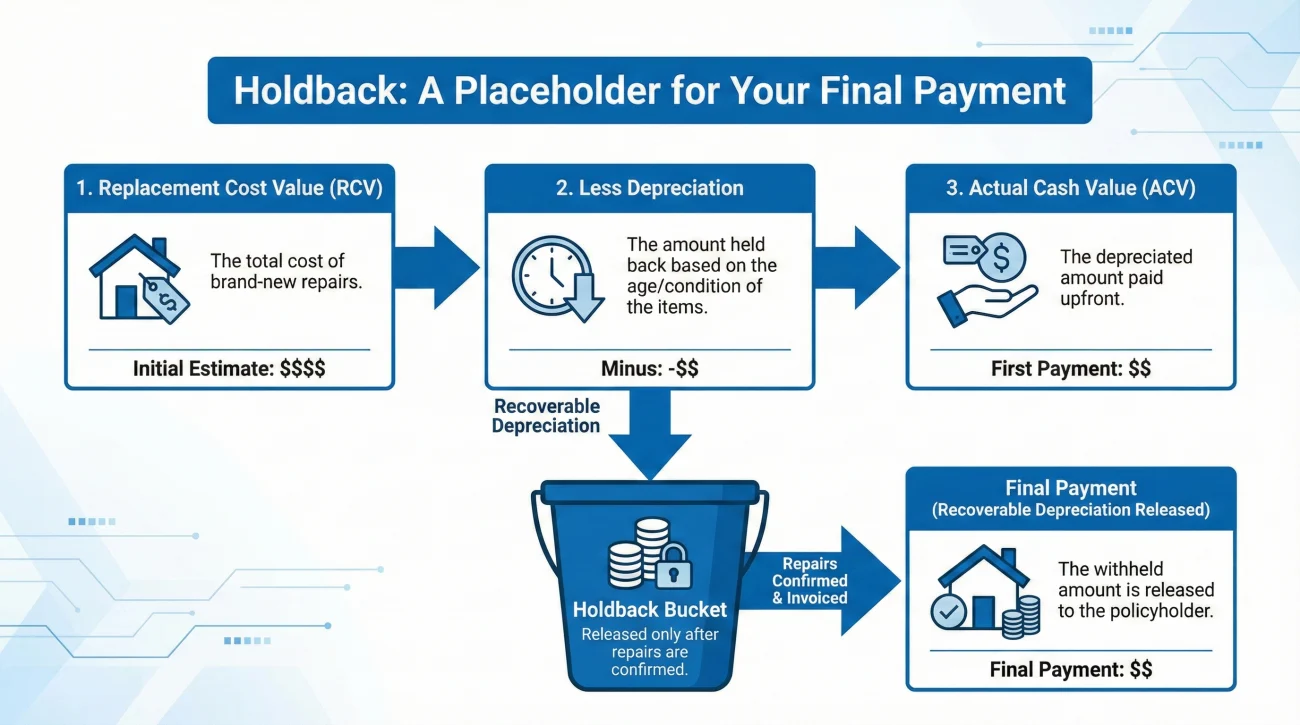

To understand the holdback, we have to briefly touch on how most property damage is valued. When a loss occurs, the adjuster writes an estimate for what it will cost to fix the damage at today’s prices. However, they do not usually hand over that entire amount on day one.

Instead, they calculate the current, “used” value of your damaged property. This is based on its age and condition right before the loss. They pay you that smaller, depreciated amount first. The difference between the total replacement cost and that initial payment is the holdback. In your paperwork, you will almost always see this referred to as “recoverable depreciation.”

Why do they do this? From an operational standpoint, the carrier needs a way to verify that the money is being used to fix the house. If they paid the full replacement cost upfront, there would be nothing stopping someone from taking the cash, selling the damaged house as-is, and walking away. The holdback is essentially a financial placeholder. It is your money, but it is locked behind a verification step.

How It Looks on Your Paperwork

When you read your estimate, you will usually see a summary page at the end. It often looks something like a math problem:

- 📄 Replacement Cost Value (RCV): The total cost to do the work.

- 📄 Less Depreciation: The amount they are holding back for now.

- 📄 Actual Cash Value (ACV): The RCV minus the depreciation.

- 📄 Less Deductible: Your out-of-pocket responsibility.

- ✅ Net Claim (First Check): What you receive upfront.

Your goal, once the repairs are done, is to submit the right documentation so they release that “Less Depreciation” amount to you. It is a strictly administrative hurdle, but it requires clean, organized proof.

Not Everything Has a Holdback (ACV-Only Situations)

It is important to note that not every item on your estimate will have recoverable depreciation. Some policies, or specific line items like wood fences or certain types of older roofs, are written as Actual Cash Value (ACV) only. This means the initial depreciated payment is the final payment for that specific item, and there is no holdback to recover later. Always check your policy declarations or ask your adjuster if you are unsure which items are RCV versus ACV.

A Realistic Scenario: The Kitchen Water Loss

Let’s look at a typical, generic mini-scenario to see how this plays out in the real world. Imagine a supply line breaks under a kitchen sink, ruining the base cabinets, the flooring, and some drywall.

The initial estimate comes in at $15,000 to replace everything (the RCV). Because the kitchen was 10 years old, the depreciation is calculated at $4,000. After applying a standard deductible, the homeowner receives an initial check for roughly $10,000.

That $4,000 is the holdback. The homeowner hires a contractor, uses the initial check to get the work started, and the contractor finishes the job. At this point, the contractor hands the homeowner a final invoice for the remaining balance. The homeowner takes that final invoice, takes pictures of the beautiful new kitchen, and sends a clean email to the desk adjuster requesting the release of the $4,000 holdback.

Once the reviewer sees the proof that the work is done, they issue the final check. The homeowner pays the contractor, and the file is closed. That is the ideal path. In reality, timelines vary; sometimes a reviewer asks for clarification on a specific line item. But starting with a review-ready packet keeps the momentum going and reduces the chances of long delays.

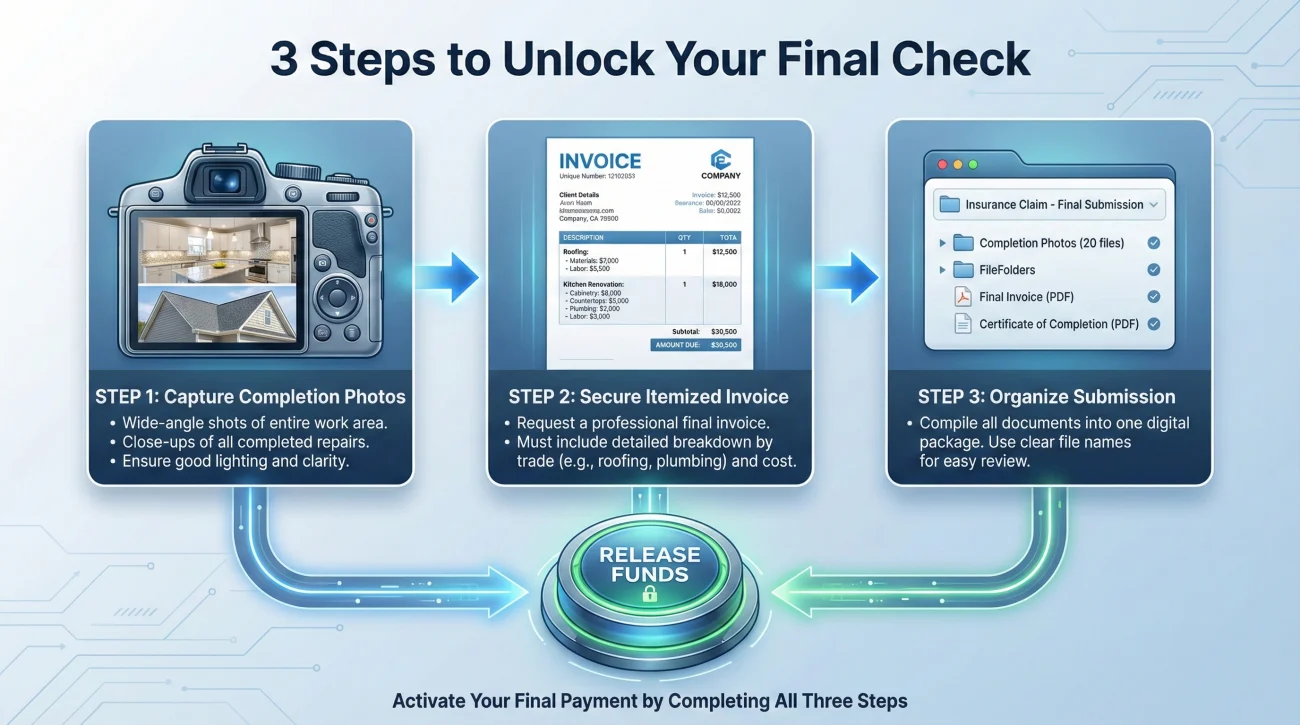

The Operational Checklist to Unlock Your Holdback

In day-to-day claims ops, the smoothest reviews usually come from submitting documentation that makes the review easier for the person on the other end. When a reviewer opens an email to process a holdback release, they are looking for clear proof of completion. If the file is messy, they will often set it aside to ask questions later.

Here is a reliable approach I recommend following to build a clean release packet.

Step 1: Capture Completion Photos

Do not assume that an invoice is enough. Many reviewers are required to have visual proof in the file before they can click the button to release funds. Before the contractor packs up their tools, take clear, well-lit photos of the finished work.

If you had multiple rooms damaged, take photos of each room. If you had roof damage, take a photo of the new shingles. You do not need professional photography, but you do need clarity. Save these photos in a single folder on your computer and name them clearly, such as “Kitchen_Completed_Flooring.jpg”.

⚠️ Warning: Sending 40 unsorted, unnamed photos taken from a cell phone can cause delays. The reviewer has to figure out what they are looking at. Pick the 5 to 10 best, clearest photos that show the completed scope.

Step 2: Secure the Final Itemized Invoice

A generic receipt that says “House Repairs – $15,000” will often trigger a delay. Reviewers need to see that the scope of work on the invoice matches the scope of work on their initial estimate.

If possible, request your contractor for a final invoice that breaks down the major trades. It should clearly show:

- The contractor’s business name, address, and contact info.

- Your name and property address.

- A breakdown of the work performed (e.g., Drywall repair, Cabinet installation, Flooring installation).

- The total cost of the project.

- A clear indication that this is the final invoice.

What If Your Contractor Will Not Itemize?

Some contractors simply write “Repairs per estimate” and refuse to break down trades, as it is not their standard billing practice. If you run into this, you have to bridge the gap for the reviewer. Ask the contractor for a brief scope summary in the email body, organize your completion photos strictly by room, and explain in your submission that the contractor’s standard format is a lump sum. The clearer your photo documentation is, the less the invoice format will slow you down.

Step 3: Organize Your Submission Packet

This is where people get stuck. They forward an email directly from their contractor to the adjuster with no context. You need to be the administrative filter. Download the invoice, attach your labeled photos, and write a clear, concise email.

If you have had to fight for missing items previously, or if the scope changed during repairs, you already know how important it is to keep your files organized. For a deep dive into structuring a response when the numbers do not align, you can review our guide on the low estimate documentation response. The same principles of clarity apply here.

Communication Hygiene: Scripts for Success

When you are ready to send your documentation, use a neutral, professional tone. Your goal is simply to inform them that the work is complete and provide the required proof.

Here is a safe, effective script for submitting your holdback release request:

Hello [Adjuster Name],

I am writing to confirm that the repairs at [Property Address] are now complete.

Please find attached the final invoice from my contractor, along with photos showing the completed work.

Could you please review these documents and process the release of the recoverable depreciation (holdback) for this claim?

Please let me know in writing if you need any additional documentation to process this release.

Thank you,

[Your Name]

[Your Phone Number]

Real-World Example: The Stalled Review

Even with a well-organized submission, delays can still happen. I recently reviewed a file where a homeowner submitted a clean packet, but a month passed with no check. The reviewer was confused because the invoice listed “paint supplies” but the estimate only accounted for drywall patching. Instead of calling and arguing, the homeowner sent a polite email asking for a “written list of missing items or needed clarifications.”

The reviewer replied, noting the paint discrepancy. The homeowner quickly clarified that the contractor threw in touch-up paint at no extra cost to match the patch. The reviewer noted the file, the confusion was cleared up, and the check was released. Getting the hold-up in writing is always the fastest way to unblock the process.

The Follow-Up Script

If you do not hear back after submitting your packet, do not immediately escalate to anger. Files get buried. A polite follow-up is usually all it takes to bump your file back to the top of their queue.

Hello [Adjuster Name],

I am following up on the final invoice and completion photos I submitted on [Date].

Can you please provide a status update on the review of these documents and the timeline for releasing the remaining funds?

If you are missing any items, please provide a written list so I can resolve it promptly.

Thank you,

[Your Name]

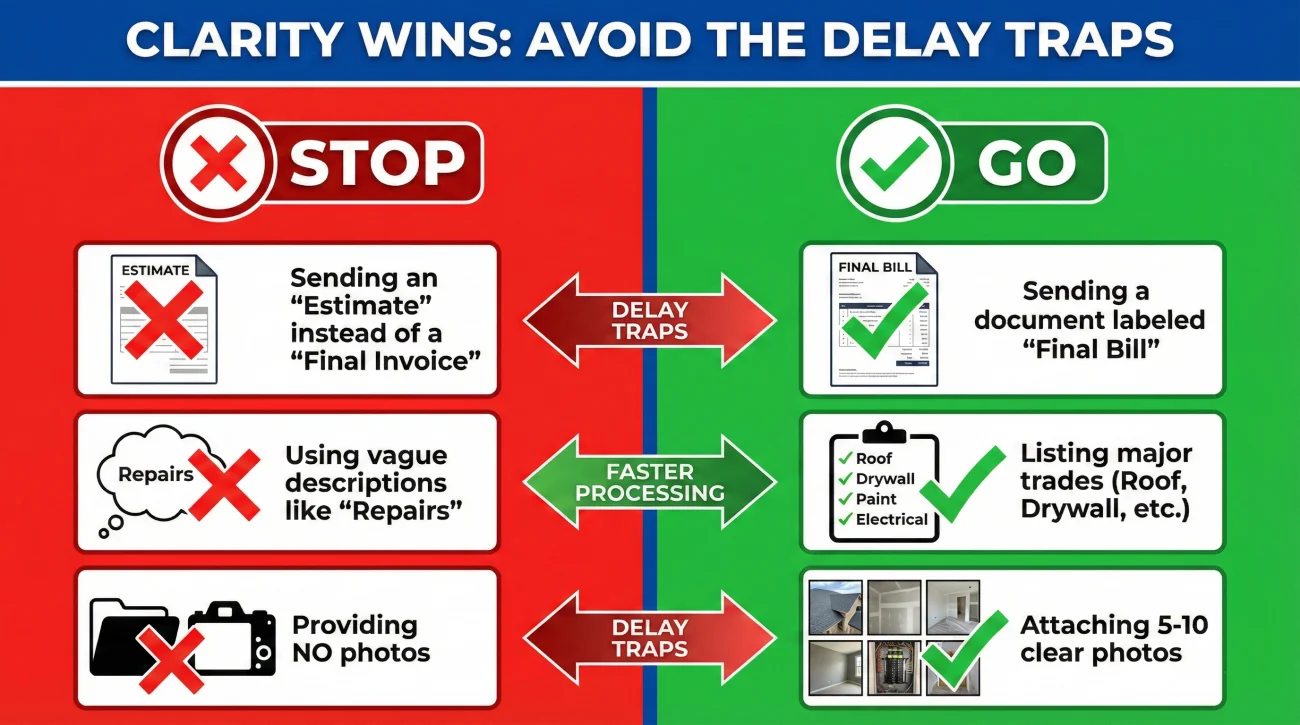

Common Mistakes That Delay the Final Check

I have seen hundreds of holdback releases get stalled for completely avoidable reasons. Review workflows are standardized, and clarity significantly reduces back-and-forth. Here are the most common operational errors I see, and how to avoid them.

| The Mistake | Why It Delays the Process | The Fix |

|---|---|---|

| Sending estimates instead of invoices | An estimate proves what the work might cost. An invoice proves what the work actually cost. Reviewers need the latter. | Ensure the document clearly says “Invoice” or “Final Bill,” not “Proposal” or “Estimate.” |

| Vague invoice descriptions | If the invoice just says “Repairs,” the reviewer cannot easily confirm that the specific items they paid for were actually fixed. | If possible, ask the contractor to list the major trades (e.g., Roof replacement, drywall repair, painting). |

| Missing the deductible conversation | Homeowners sometimes expect the final check to cover the contractor’s full remaining balance, forgetting they must pay their deductible out of pocket. | Always subtract your deductible from the total pool of money when calculating what you owe the contractor. |

| No photos provided | Many carriers require visual verification. If they do not have photos, they may try to schedule an in-person reinspection, which takes weeks. | Always attach 5-10 clear photos of the completed work with your final invoice. |

❌ Note: A common pattern I see is a file going entirely quiet because the reviewer noticed a discrepancy on the invoice, but never reached out to ask for clarification. This is why following up and asking for a written list of missing items is so crucial.

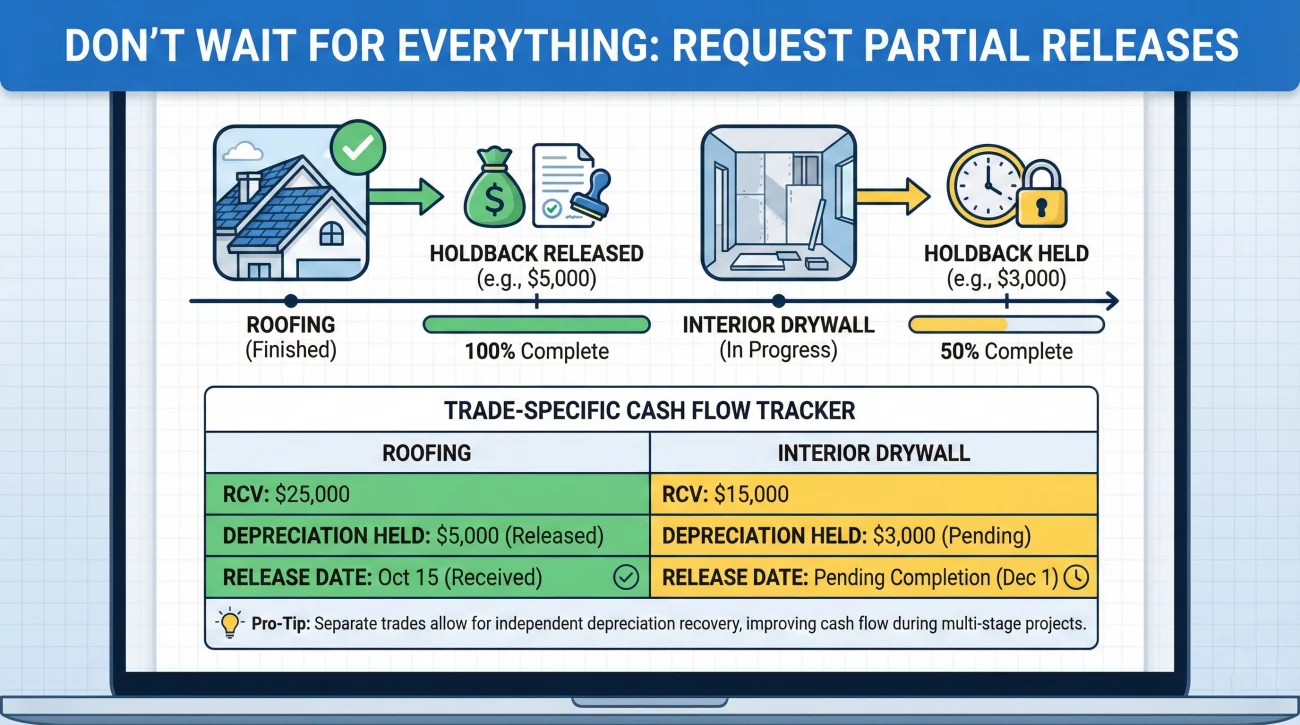

Managing Partial Holdback Releases

A situation that often confuses people is dealing with a large loss where multiple different contractors are involved. Let’s say a severe storm damages your roof, but also causes interior water damage. You might hire a roofing company to do the exterior, and a general contractor to do the interior.

Depending on your carrier, you do not always have to wait until the entire house is finished to ask for your holdback. In many cases, you can request a partial release.

For example, if the roof is finished but the interior is going to take another month, you can take photos of the new roof, get the final invoice from the roofing company, and submit that specific packet. You simply state in your email: “Please find the final invoice for the roof replacement. I am requesting a release of the recoverable depreciation associated with the roofing scope only. Interior repairs are still ongoing.”

Waiting 6 months for all trades to finish while contractors ask for payment, causing immense stress.

Submitting a clean invoice and photo packet for each trade as they finish, maintaining cash flow and keeping contractors updated.

The Simple Holdback Tracker

If you are managing multiple trades, keeping track of what has been released can get messy. I recommend creating a simple tracker in a spreadsheet or on a piece of paper to stay organized.

| Trade / Scope | Total RCV | Depreciation Held | Proof Submitted Date | Release Received Date |

|---|---|---|---|---|

| Roofing | $12,000 | $3,500 | Oct 12 | Oct 20 |

| Interior Drywall | $4,500 | $1,200 | Nov 05 | Pending |

This approach requires a bit more administrative tracking on your part, but it is often a highly practical way to manage a complex, multi-trade restoration project.

The Importance of a Dedicated Claim Folder

I cannot stress enough how important basic file hygiene is when you reach the end of a claim. By the time you are asking for your holdback, you likely have dozens of emails, multiple estimates, and various receipts. If these are scattered across your inbox, your spouse’s inbox, and the backseat of your car, you are going to struggle to build a clean submission packet.

Create a single digital folder on your desktop. Inside it, keep a sub-folder titled “Final Invoices” and another titled “Completion Photos”. When you save your final submission email, save a PDF copy of it into this folder. Keep a simple timeline log—just a notepad file—where you note the date you requested the release.

[Action (Sent Invoice)] + [What you need in writing (Confirmation of receipt)] + [Confirmation request (Timeline for check)]

This level of organization does two things: it makes the actual submission take five minutes, and it gives you complete confidence when you have to follow up. You never have to guess when you sent something or what exactly was attached.

Final Thoughts on Securing Your Funds

Navigating the holdback process is largely an exercise in administrative patience. It is normal to feel frustrated that your money is being held, but understanding that this is a standard procedural step helps remove the emotion from the equation.

Remember that the person on the other side of the screen processing your release is looking for a file that is easy to review and approve. Give them clear invoices, unmistakable photos, and a polite, direct request. Do not leave room for ambiguity. If you handle the submission like a seasoned project manager, you significantly reduce the chances of your final payment being delayed in a stack of “needs review” files.

Stay organized, put your requests in writing, and always confirm receipt. You are simply closing the loop on the process.

❓ FAQ

🤔 What is a holdback in an insurance claim?

A holdback, usually listed as recoverable depreciation, is a portion of your settlement that the insurance company retains until you provide proof that the repairs have been completed.

⏳ How long does the insurance company hold back money?

They typically hold the funds until you submit a final invoice and completion photos. Once submitted, processing the release usually takes a few days to a few weeks, depending on their current volume.

⚖️ Is holdback the same as depreciation?

Yes, in most contexts. The holdback amount is the “recoverable depreciation.” It represents the difference between the full replacement cost and the actual cash value of your old, damaged property.

🔓 How do I get my holdback money released?

You unlock the funds by emailing your desk adjuster a final invoice from your contractor along with clear photos showing the completed repairs, accompanied by a direct request for the release.

🔨 What happens if I do the repairs myself, do I get the holdback?

In many cases, you can recover the holdback for the cost of materials if you provide receipts and photos. However, policies vary on whether they will pay the holdback for your personal labor time. Always ask for their requirements in writing.

🧾 Do I need to send receipts to get the holdback?

If you hired a contractor, their final itemized invoice usually serves as the receipt. If you bought materials yourself, you will need to provide those specific retail receipts along with completion photos.

🏢 Can a contractor bill the insurance company directly for the holdback?

Unless you have signed specific authorization documents (like an assignment of benefits, where applicable), the insurance company usually issues the check to you, and it is your responsibility to pay the contractor.

📉 What if my final invoice is less than the estimate, do I still get the full holdback?

Often, no. It depends on incurred cost rules, but insurance usually pays the actual incurred cost up to the limit of their estimate. If the work cost less, they will typically only release enough holdback to cover the actual invoice amount.

🛋️ Do they hold back money on personal property claims too?

Often, yes. For personal belongings, you usually receive the depreciated value first. You get the holdback released when you provide a receipt proving you actually purchased a replacement item.

👀 Will the insurance company inspect the house before releasing the holdback?

Sometimes. If it is a very large claim, they may send an adjuster to verify the work. For many routine claims, clear photos and a final invoice are often sufficient, though some carriers still require reinspections.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.