- A denial letter is often an operational pause due to missing documentation, not always a permanent roadblock.

- Your first step is to decode the specific language in the letter to identify the exact gap in your paperwork.

- Keep all reactions in writing. Avoid calling to argue; instead, use structured emails to map your evidence to their requirements.

- Organize your rebuttal evidence cleanly (clear file names, logical order) before responding, treating this as a data-collection task rather than a legal battle.

The Initial Shock and the Operational Reality

Opening a letter that says your claim has been denied is an incredibly stressful moment. Most homeowners immediately panic, assuming the insurance company has permanently shut the door and that their only remaining option is to hire an expensive lawyer or give up entirely. If you are currently searching for insurance claim denied what to do, take a deep breath.

In my years working in claim operations, I have learned a fundamental truth about these letters: operationally speaking, a denial is very often just a poorly worded request for more information. Adjusters are essentially auditors working within strict software systems. If a specific box cannot be checked because a date is missing, a photo is unclear, or a contractor’s invoice lacks a crucial sentence, the system often triggers a denial. They cannot simply approve a file that lacks the mandatory proof.

To be clear: my goal here is to help you optimize your operational file. This guide is not legal advice, and it does not replace consulting a professional if you reach a true operational dead-end. However, before assuming the worst, we need to treat this as a missing-data problem. We need to find out exactly what data is missing and provide it cleanly.

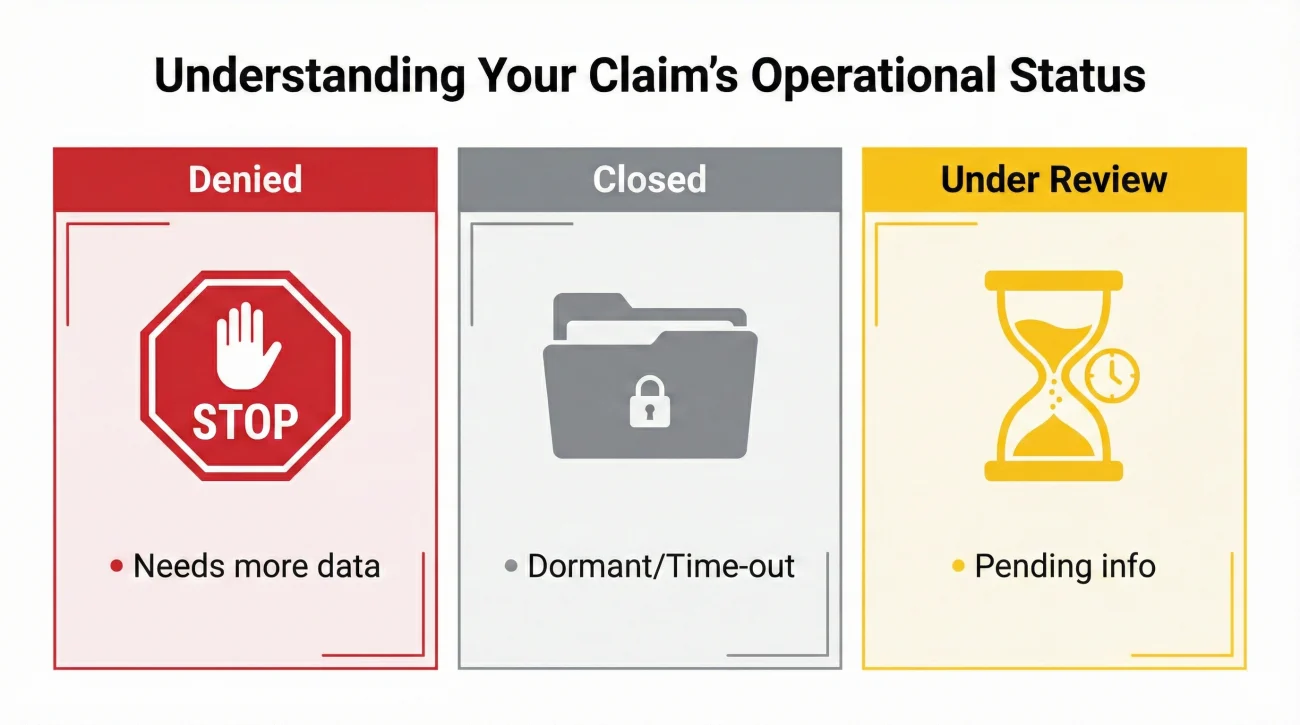

Status Check: Denial vs. Closure vs. Under Review

Before diving into the letter itself, it is crucial to understand the exact operational state of your file. Claim departments use specific terms that mean very different things.

- 🛑 Denied: The insurer has reviewed the current file and determined that, based on the evidence provided or policy language, they will not pay. (This is what we are addressing here, and it can often be reversed with new data).

- 📁 Closed: The file is dormant. This often happens automatically if you haven’t responded in 30 to 60 days. A closed claim can almost always be reopened simply by sending an email with an update.

- ⏳ Under Review / Pending Info: The file is still open, but the adjuster is waiting on an internal decision, a vendor report, or a document from you.

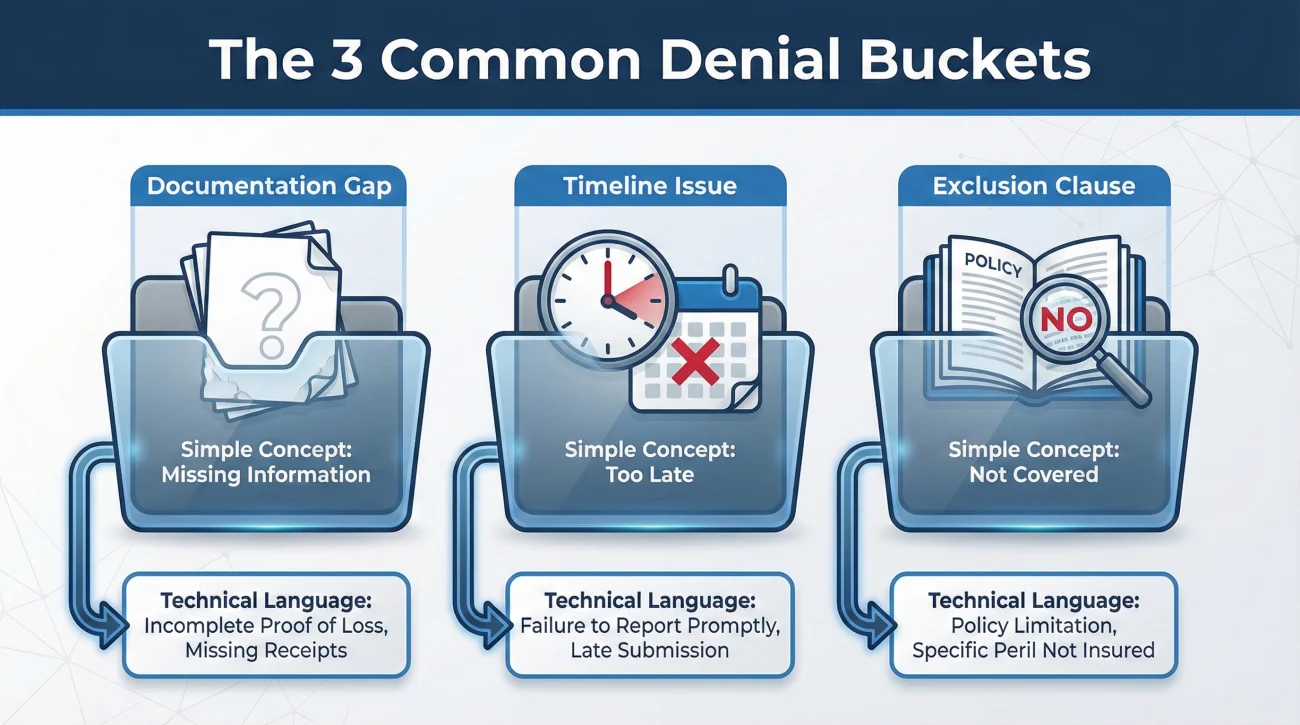

Decoding the Letter: The Language Traps

Insurance letters are written in heavy, technical language that can be difficult to interpret. However, if you strip away the boilerplate text, you will usually find that the denial falls into one of three operational buckets. I always tell homeowners to look for these specific “language traps” to know exactly what the adjuster is missing.

Bucket 1: The Documentation Gap

This is the most common reason for a denial. The insurer is stating that you have not provided enough evidence to prove the loss happened the way you said it did. Watch for phrases like “could not determine causation” or “insufficient evidence.” This does not mean they think you are lying; it simply means the file on their desk is too thin to justify a payout.

Key Point: A documentation gap is the easiest denial to fix. You just need to prompt the adjuster for an exact list of what document they are looking for and provide it.

Bucket 2: The Timeline Issue

Policies have strict operational timelines. If a claim is denied for this reason, you will see phrases like “failure to comply with conditions,” “late notice,” or “prejudice to our investigation.” If you missed a deadline, the system triggers a denial. In many cases, if you can provide email timestamps proving you did send the document on time, or document a valid operational reason for the delay, this can be corrected.

Bucket 3: The Exclusion Clause

This is when the letter cites a specific section of your policy stating that the type of damage is not covered. They might cite “wear and tear,” “long-term seepage,” or “earth movement.” Your operational task here is to review the evidence you submitted. Did your contractor use a loose word that accidentally triggered that exclusion?

Real-World Patterns: Three Common Denial Triggers

To illustrate how these buckets work in practice, let me share three operational patterns I see repeatedly when reviewing stalled or denied files.

Pattern 1: The Vague Plumber Invoice

A homeowner experiences a sudden pipe burst, gets it fixed, and submits the invoice. The denial letter comes back citing “wear and tear.” When we look operationally at the plumber’s invoice, it simply reads: “Fixed pipe under sink. $450.” It lacks descriptive detail. The adjuster had no proof it was a sudden break. The operational fix? The homeowner asked the plumber for an updated invoice stating “repaired sudden catastrophic rupture of supply line.” The denial was reversed without a legal fight.

Pattern 2: The “Scope Too Broad” Estimate

I constantly see claims stalled or partially denied because a contractor’s estimate is too broad. If an estimate just says “Rebuild roof – $15,000,” the adjuster cannot use it. They need line items to map against the policy coverage. Without itemized costs and clear causation language, the system kicks it back for “insufficient documentation.”

Pattern 3: Context-Free Photos

Homeowners often submit 50 extreme close-ups of a damaged shingle or a cracked tile. While detail is good, a lack of context is a massive operational gap. Without a wider shot showing the whole roof, or a timeline proving exactly when the damage happened (like a timestamped photo right after a storm), the adjuster cannot verify the event, leading to a “could not determine causation” denial.

Your Immediate Next Steps: The Operational Playbook

Acting impulsively or emotionally will only delay the process further. Here is the exact order of operations you should follow to map your evidence to their requirements and get the claim back on track.

Step 1: Save, Log, and Do Not Call

Your instinct will be to pick up the phone to argue. Phone calls leave no paper trail and often lead to frustrating, circular conversations. Save the denial letter as a PDF in your dedicated claim folder. Log the date you received it in your timeline tracker. It is highly risky to assume the adjuster remembers your previous phone conversations; if it isn’t in their system’s written log, it essentially does not exist during a denial review.

Step 2: Request the Specific Missing Items List

Your goal is to move the adjuster away from vague boilerplate language and get a concrete list of what is missing. You are not asking them to change their mind yet; you are only asking them to explain the gap.

Subject: Clarification Request – Claim #12345678 – Denial Letter Received

Hello [Adjuster Name],

I received the letter dated [Date] stating that my claim has been denied. To help me understand the status of my file, could you please provide a specific, written list of the documentation or evidence that is currently missing from my file?

If the decision was based on a lack of proof regarding the cause of the damage, please let me know exactly what type of report, phrasing, or photo would satisfy that requirement.

I look forward to your written response so I can gather the correct items.

Thank you,

[Your Name]

Step 3: Organize and Package the Rebuttal Evidence

Once you know what is missing, gather the documents that counter the denial reason. However, you must package them perfectly. Do not just forward a messy chain of emails from your contractor. Use this minimalist packaging checklist for your reply:

- ✅ Clear File Naming: Rename files so the adjuster knows exactly what they are clicking (e.g.,

Smith_Kitchen_Leak_Updated_Plumber_Invoice.pdf). - ✅ Chronological Order: If submitting timeline proof, attach the earliest emails or photos first.

- ✅ The Mapping Sentence: Include one clear sentence in your email mapping the new document to their denial reason. (e.g., “Attached is the revised invoice addressing the causation issue mentioned in your letter.”)

If you are unsure how to keep this new wave of documents structured, refer to our comprehensive guide on building a reliable claim follow-up system.

Common Mistakes When Reacting to a Denial

When people try to navigate a denial without an operational process, they often cement the denial permanently. Here are the most common errors and how to avoid them.

| The Mistake | Why It Fails Operationally | The Better Approach |

|---|---|---|

| Sending a massive, disorganized email dump. | Adjusters do not have time to sort through 50 unlabeled photos and a long emotional story. They will just file it away. | Send one clean email with clearly labeled PDF attachments and bullet points mapping the evidence to their concerns. |

| Threatening legal action immediately. | Threats usually cause the adjuster to stop communicating entirely and send your file to the legal department, freezing progress. | Keep the tone neutral and focus entirely on the missing data and the specific wording of the policy. |

| Guessing what the adjuster needs. | You might spend money on a new, expensive inspection that the insurer never asked for and still will not accept. | Require the adjuster to provide a written list of exactly what evidence would change the status of the file before you spend a dime. |

❌ Note: Always remember that your email is being read by an auditor looking for checkmarks, not a jury looking for an emotional appeal. Keep it strictly focused on facts and timelines.

What If The Adjuster Refuses to Elaborate?

In some cases, an adjuster may reply to your clarification request by simply repeating the original denial letter: “Please refer to the letter sent on Tuesday.” This is an operational roadblock.

When the primary contact refuses to provide an actionable list of missing items, you must escalate the communication internally. Internal escalation is about finding a manager who can clarify the operational requirements. It is completely different from threatening legal action—which, as noted, often freezes the file.

Subject: Second Request for Clarification / Supervisor Review – Claim #12345678

Hello [Adjuster Name],

Thank you for your reply. Unfortunately, the original letter does not provide a specific list of the missing documents I need to supply to complete this file.

Because I want to ensure my file is accurate and complete, could you please escalate this request to a supervisor or team lead who can provide a concrete list of the required documentation?

Please confirm when this file has been forwarded for review. I appreciate your help in getting this clarified.

Best regards,

[Your Name]

Final Thoughts on Managing the Process

A denied claim is a setback, but it is rarely the end of the road if you handle it systematically. The secret to reversing these decisions lies in your documentation hygiene and your communication discipline. By refusing to engage in emotional arguments and instead requiring the insurer to outline exactly what data is missing, you take back control of the timeline.

Remember to keep every single interaction in writing moving forward. Treat your claim file with the same rigor an auditor would, map your new evidence directly to their stated concerns, and you will dramatically improve your chances of getting a clear, fair resolution.

❓ FAQ

🛑 What is the first thing I should do when my claim is denied?

Read the letter carefully to find the specific operational reason for the denial, save a copy in your claim folder, and log the date you received it. Do not immediately call the adjuster to argue.

🔄 Can an insurance company reopen a denied claim?

Yes, in many cases. If a claim was denied due to missing information or a lack of clarity, providing new, cleanly packaged evidence that addresses their specific concerns can prompt them to reopen the file.

⏳ How long do I have to respond to a denied claim?

This depends entirely on your specific policy and local regulations. Check your denial letter and your policy documents immediately for any strict deadlines regarding appeals or submitting new evidence.

📋 Should I get a new contractor estimate if my claim was denied?

Only if the denial was specifically based on a “scope too broad” issue or insufficient detail in your original estimate. Ask the adjuster for a written list of what was missing before spending money on a new one.

✉️ How do I ask for the specific reason my claim was denied?

Send a polite email asking for a bulleted list of the exact documents or proof that was missing from your file, or ask them to point to the exact sentence in the policy they are relying on.

🔎 What does “lack of evidence” actually mean in a denial letter?

Operationally, it usually means your photos lacked context (no wide shots), your contractor’s invoice lacked a description of the cause of loss, or you did not provide enough proof to connect the damage to a specific timeline.

💻 Can I just email my response to a claim denial?

Yes, and you absolutely should. Replying via email ensures you have a permanent, date-stamped paper trail of your response and the new, clearly labeled evidence you are submitting.

🔇 What if the adjuster ignores my emails after a denial?

If they do not respond to written requests for clarification within a reasonable timeframe, you should send a polite follow-up email requesting that the file be escalated internally to a supervisor or team lead.

⚖️ When is it time to consult an attorney?

If you have provided all requested documentation cleanly, escalated internally, and the insurer still refuses to engage or relies on an unreasonable interpretation of the policy, you have reached an operational dead-end and may need professional legal guidance. This varies by jurisdiction.

🏛️ Should I file a complaint with the state insurance regulator?

A regulatory complaint is an option if you have documented proof of unfair operational practices (like ignoring timelines). However, your primary goal right now should be fixing the paperwork gap; regulatory complaints rarely fix a file that is simply missing data.

⚠️ Disclaimer: PropertyClaimChecklist.com provides practical guidance, process checklists, and example follow-ups to help you organize a property claim and move it forward. It is not policy language, claim documentation, legal content, or a substitute for your insurer's instructions. Always rely on your carrier's requirements and your actual policy terms for what must be submitted and how decisions are made.